Does Taxing U.S. Corporations Make Sense in a Global Economy?

Reed College

The Issue:

The belief that it is essential to lower corporate tax rates is widely held by many, including members of the Trump administration and Congressional Republicans. Critics of the U.S. corporate tax system point to its high rates, the distortions it introduces, the possible double-taxation of corporate equity, and difficulties collecting the tax in an era of highly mobile multinational corporations. In response, both policy-makers and academics have suggested cutting the statutory rate from its current 35 percent to 15 percent or 20 percent. Others argue that reform should focus on shoring-up the corporate tax base: while they concede that some reduction in the statutory rate may be warranted, they argue it should be coupled with measures to stem profit shifting and other tax loopholes.The Facts:

- The current U.S. corporate tax system taxes corporate income at a statutory rate of 35 percent — which is among the highest in the world. In addition, unlike many other countries, the United States taxes the worldwide income of multinational companies (allowing a foreign tax credit for tax payments to foreign governments). Critics argue that this tax system puts United States corporations at a competitive disadvantage relative to companies based in foreign countries. Whether it does in fact have this effect is difficult to prove. The data indicate that United States multinational corporations are doing well. Corporate profits are higher as a share of GDP than they have been at any time in a half-century, in both before-tax and after-tax terms. United States multinational firms also dominate lists of the world’s top multinational companies; in the latest Forbes rankings of the world’s top 2000 companies, U.S. companies are one-third of the global total (measured by sales), 47 percent (measured by profits), and 44 percent (measured by market capitalization), even as the United States accounts for just 22 percent of world GDP. The U.S. share of top Forbes companies has actually increased over the previous couple of years, despite the ascendency of China and India. While our corporate tax system has problems, the competitiveness of internationally mobile companies is not at the top of the list.

- In practice, both the high rate and the worldwide reach of the U.S. tax system have more bark than bite for U.S. multinational companies. Most multinational companies pay effective tax rates that are far lower than the statutory tax rate and comparable to effective tax rates paid by multinational companies based in other countries, as researchers at the Congressional Research Service, the Government Accounting Office, the Treasury, and elsewhere have found. And the U.S. government raises almost no revenue from taxing the foreign income of multinational firms, since tax is not due until repatriation, and companies leave the money abroad, only repatriating in the case of a special holiday, or when they have access to offsetting foreign tax credits. While some argue that this reduces funds for domestic investment, it is important to keep in mind that these companies are the most credit-worthy on the planet, and can easily borrow to finance worthy investments. Further, much of the money that is booked “offshore” is actually invested in U.S. assets and available to U.S. capital markets. Still, shareholders are eager to get ahold of these earnings in the form of dividends and share repurchases, and therefore they have been a vocal voice for reform.

- Despite having a higher statutory corporate tax rate, the United States raises less revenue from corporate taxes relative to the size of its economy than peer countries. While the U.S. raises about 2 percent of GDP through the corporate tax; peer countries’ corporate tax revenues average 3 percent of GDP. These low revenues result from the fact that corporations are able to reduce the amount of income that is subject to the 35 percent statutory rate (what economists call the tax base). Several factors contribute to reducing the corporate tax base. For instance, tax laws that favor non-corporate business income lead to tax base leakage out of the corporate sector. Similarly, tax incentives that encourage profit shifting to overseas tax havens are estimated to cost the U.S. government over $100 billion in revenue per year.

- There are concerns that the corporate tax adversely distorts economic decisions. One distortion tilts companies towards debt-financed investments relative to equity-financed investments, since debt-financed investments are actually subsidized through the tax system whereas equity-financed investments may be taxed twice — once at the corporate level and a second time when investors receive capital gains or dividends. The corporate tax also encourages some types of investments relative to others because of relatively favorable tax treatment. The complexity of the corporate tax system means both high compliance costs and ample opportunities for tax avoidance for savvy taxpayers. And, as mentioned above, the corporate tax encourages firms to shift profits to tax havens, and then retain their income in tax-havens abroad, delaying repatriation of the funds to the United States.

- Yet a corporate tax is a key instrument for taxing capital income as well as excess profits. An economic case can be made for taxing both of these items. Corporate profits have been rising in the United States and are at historically high levels. At the same time, the share of labor in total income is falling in both the United States and other countries. Recent research supports taxing capital at rates that are similar to top labor income tax rates. It is also efficient to tax “excess profits,” such as those that arise due to market power, since this will have less of an effect of depressing economic activity than taxing a firm that is just breaking even. U.S. Treasury economists estimate the fraction of the corporate tax base that is excess profits (above the risk-free rate of return) is about 75 percent. Most agree that excess profits have been rising over time, in part due to intangible-intensive firms with market power. The optimal tax rate on such profits is higher than that on either the normal return to capital or labor income.

- The corporate tax is far more progressive than virtually any other tax instrument at the government’s disposal. Both capital income and super-normal profits are disproportionately held by the wealthiest individuals. There is little evidence that corporate taxes lower wages through a reduction in the capital stock, which would lower the productivity of labor. Tax progressivity is important, given trends in income inequality, the falling share of labor in national income, and middle-class wage stagnation.

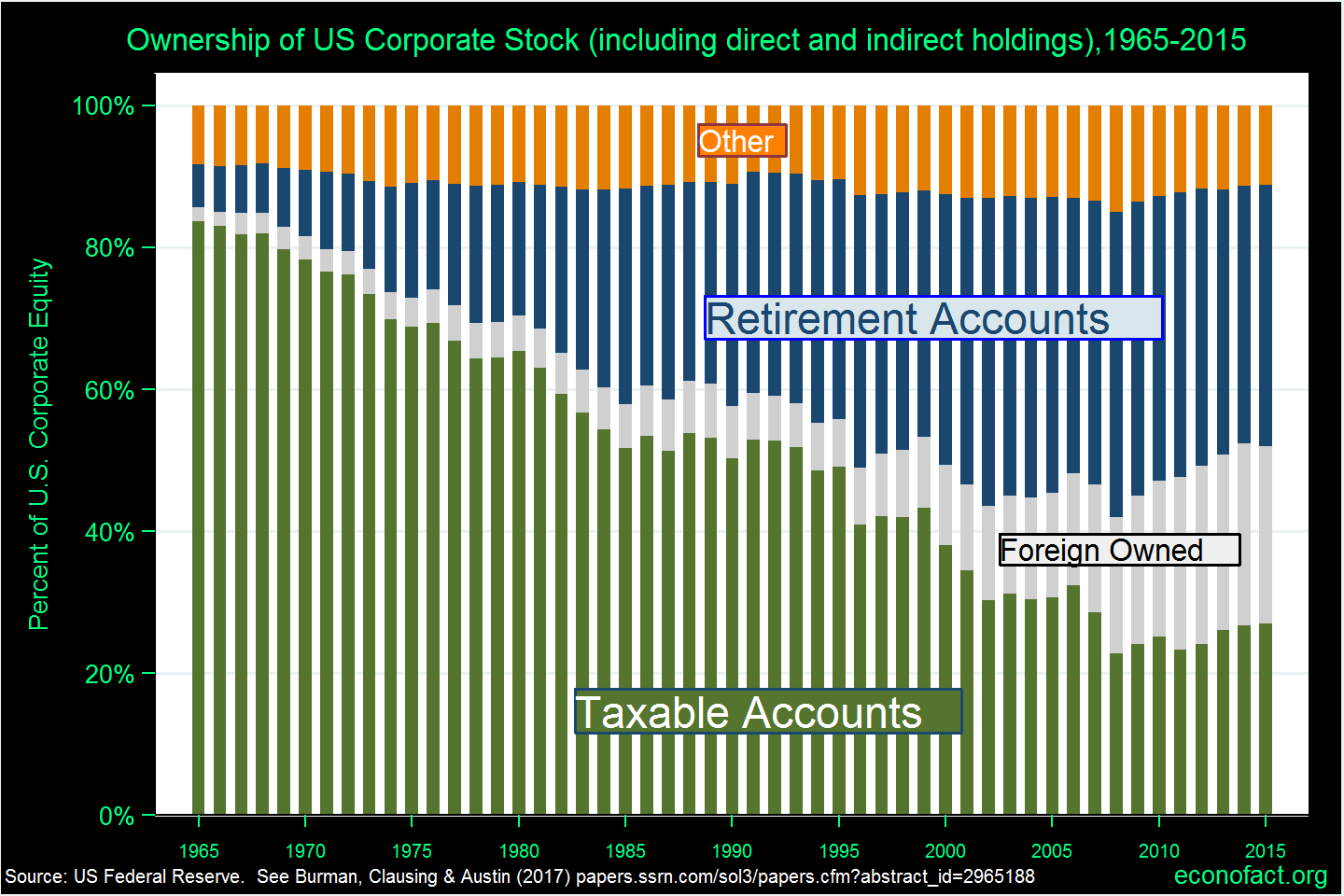

- Would it be better to tax capital at the individual level instead of the corporate level? Some, including Utah Senator Mike Lee, suggest lowering the corporate tax rate (or eliminating it altogether) and coupling this with increased taxation of capital income through the individual income tax system. In practice, this is difficult. Recent research suggests that the vast majority of U.S. equity income goes untaxed at the individual level, and the taxable share of U.S. equity income has fallen dramatically in recent decades (see chart). There are several reasons for this, including tax preferences for retirement savings, demographic changes that have swelled these retirement accounts, the increased internationalization of asset holdings, and other tax preferences such as college-savings accounts. In addition, moving the burden to the individual level creates a large disincentive to sell stock, which postpones tax payment indefinitely. Policies for handling this problem, such as a “mark-to-market” tax system that would tax returns as they are accrued on paper, or an interest charge on long-held assets, face technical difficulties and political obstacles.

What this Means:

Despite its many critics and flaws, the corporate tax is a vital part of our tax system. It is a necessary part of capital taxation and it helps fulfill the efficiency, equity, and revenue goals of our tax system. The corporate tax would certainly benefit from a major reform. For instance, corporate tax reform should better align the label and reality of our tax system — such that the statutory rate is much closer to the rate that corporations are actually paying. Statutory tax rates can fall, as long as we also expand the corporate tax base. This would protect revenues and retain the progressivity of the tax system. Measures such as a per-country minimum tax (taxing, without deferral, the foreign income earned in tax havens and other very low tax countries) coupled with measures to address corporate inversions would address profit shifting and the problem of large offshore earnings stockpiles that companies are loath to repatriate since they hope for more favorable tax treatment. Reforms should also lower distortions by evening the tax treatment of different types of business income, such as corporate and pass-through business income, and debt- and equity-financed investments. But, there is no reason to lower corporate tax revenues relative to the current baseline. Such tax cuts would swell the deficit and seem especially unwarranted at a time when businesses have record after-tax profits; there is no evidence that even more after-tax profits will unleash a sustained economic renaissance, despite claims to the contrary. Large cuts to corporate tax revenues would make our tax system far less progressive, a troubling response to the increasing income inequality and middle-class wage stagnation of the previous decades.