How will the Tax Cuts and Jobs Act Impact American Workers?

Reed College

The Issue:

Backers of the tax legislation signed into law by President Trump at the end of 2017, referred to as the Tax Cuts and Jobs Act (TCJA), have made bullish claims about the ultimate effects of the legislation for American workers, with bold predictions about large increases in economic growth, investment, and job creation. The Tax Cuts and Jobs Act clearly entails tax cuts, with an estimated revenue cost of $1.45 trillion over ten years. However, whether the legislation will spur additional job creation is far less clear, especially since the economy is beginning from a position near, or perhaps even beyond, full employment. Is the legislation likely to truly help American workers?The overall package of tax cuts tilts most benefits towards the wealthy. Eventually, these tax cuts must be paid for with tax increases or spending cuts.

The Facts:

- Very large tax cuts in the Tax Cuts and Jobs Act go to corporations, with most of the provisions being permanent. On the business side, there are about $650 billion in corporate tax cuts as well as about $265 billion of net tax cuts on pass-through businesses. (All estimates are over ten years; see the revenue effects of the TCJA detailed by the Joint Committee on Taxation). International provisions raise $324 billion due to taxing prior offshore earnings at a lower rate (8 or 15.5 percent) than would have applied under prior law; that provision raises $340 billion, but on net other international business provisions lose $16 billion in revenue. Most corporate provisions are permanent, although the pass-through provisions expire (“sunset”) after 8 years.

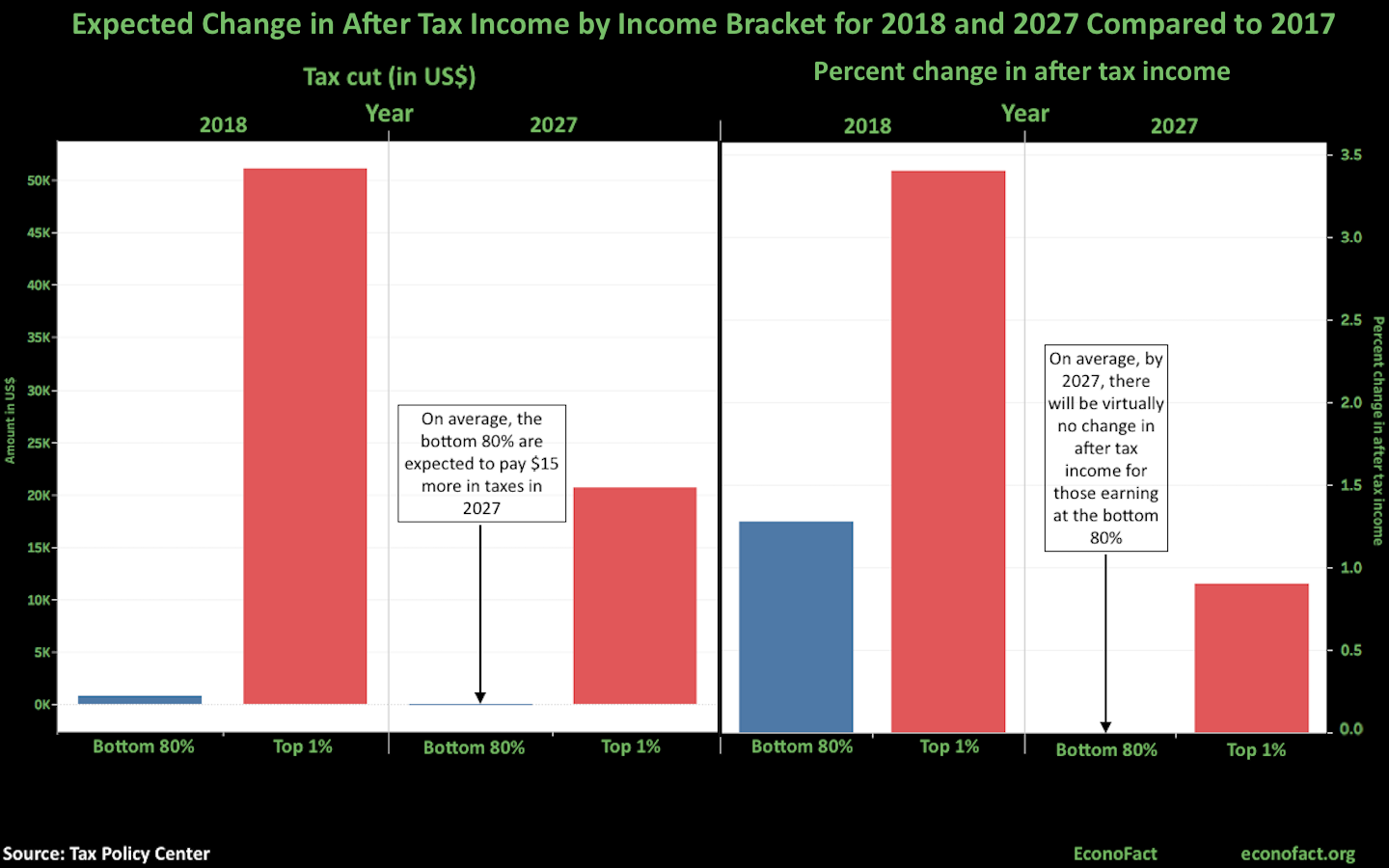

- The tax cuts granted to individuals are set to expire in 8 years and tend to provide greater benefits to people at higher income levels. Some of the tax cuts are clearly directed toward those at the top of the economy, including a cut in the top marginal rate of two percentage points, a reduction in the bite of the Alternative Minimum Tax, and a doubling of the estate tax exemption, which only benefits the top one-fifth of one percent of estates. Many other provisions depend on the individual circumstances of the taxpayer; the standard deduction is doubled, but personal exemptions are eliminated, and some itemized deductions are limited. The child tax credit is expanded, but in a way that excludes the “Dreamers” since a social security number is required to claim it. Tax rates are generally lowered, but the inflation measure is changed, which slowly increases tax burdens over time. On net, the nonpartisan Tax Policy Center estimates that, in 2018, the bottom 80 percent of U.S. taxpayers will receive a tax cut of $795, about 1.3 percent of their after tax income, but by 2027 the legislation will result in an average tax increase of $15 for the same taxpayers. In contrast, taxpayers in the top 1 percent of the income distribution are estimated to receive a tax cut in excess of $50,000 (more than 3 percent of their after-tax income) in 2018. By 2027, the top 1 percent still receives a tax cut in excess of $20,000 (see chart). Joint Committee on Taxation estimates also find tax cuts tilted toward the top.

- Some of the benefits of the tax cut for corporations may be passed on to workers, but the larger share is expected to go to shareholders. For instance, the estimates above from the nonpartisan Tax Policy Center assign some fraction of corporate tax cut benefits to workers, but they assign a majority of the benefits from these tax cuts to shareholders or investors who are more likely to be at the top of the income distribution. Widely respected mainstream models conclude that the corporate tax mostly falls on capital or shareholders, with workers only bearing a small minority — typically about 20 percent — of the tax (see for instance estimates from the Joint Committee on Taxation, the Congressional Budget Office (pages 17-18), and (until recently) the U.S. Treasury). If the burden of the corporate tax falls disproportionately on owners of capital, then it follows that a reduction in the corporate tax would be expected to benefit capital owners disproportionately.

- How might business tax cuts ultimately redound to workers' benefit? Two mechanisms might generate that result. First, companies with above-normal profits may share them with their workers. There is some limited evidence supporting this mechanism, though it often relies on evidence from countries with very different wage-setting cultures. And, early evidence on workers’ benefiting from the sharing of higher profits due to the TCJA is not promising. Companies have used the vast majority of tax cut savings on paying dividends and buying back shares. Indeed, share buybacks reached record highs in early 2018; at this rate, 2018 will mark the first year that buybacks exceed $1 trillion. In comparison, wage increases and bonuses have been paltry; wage growth in the first quarter of 2018 was identical to wage growth in the first quarter of 2017.

- A second way workers may benefit is if companies respond to the incentives created by the TCJA to raise investment, which could lead to greater worker productivity and increased wages. This mechanism will take more time to assess. Expensing provisions, which sunset, should encourage company investment, and the lower corporate rate should make equity-financed investments more attractive. But this is somewhat offset by a higher cost of debt-financed investments due to TCJA. If, on net, investment rises, that should eventually boost worker productivity and wages, but this will take time. So far, trends in the investment share of GDP are not particularly impressive. Overall, there are many reasons to be skeptical that this mechanism will lead to large increases in worker wages; this issue is explored extensively in a prior Econofact piece.

- Economic growth is unlikely to be as robust as supporters of the TCJA claim. While proponents of the TCJA argue that it will dramatically increase economic growth, investment, and eventually, worker wages, mainstream estimates of the growth effects of the legislation suggest that deficits will remain large and that economic growth effects will be small. One difficulty in parsing the effects of the TCJA is disentangling its effects from the more robust wage growth and investment that have occurred in the prior few years, including before the present administration took office.

- The impact of the tax law on health insurance is also likely to have an important effect on American workers. Embedded in the tax law was a repeal of the individual mandate to buy health insurance under the Affordable Care Act. This is expected to increase the number of uninsured Americans by 13 million over time. This saves the government $300 billion, since there will be fewer subsidies for health insurance due to the increased number of uninsured people. But the increased number of uninsured also increases health insurance premiums for others by over $1,000 for a benchmark premium, likely more than offsetting the positive effects of the tax cut on workers’ take-home pay.

- The tax cuts increase the federal deficit, and the way in which we tackle growing government deficits in the future will also impact workers. These tax cuts are deficit financed, and they occur in a context of rising government debt burdens. The Congressional Budget Office predicts debt to GDP ratios will approach 100 percent within the next decade. Eventually, these tax cuts must be paid for with either future tax increases or spending cuts (or some combination thereof). If future taxes are increased, it is unlikely that business tax cuts will be fully reversed, so middle-class workers will bear a disproportionate burden of future tax increases. If government spending is cut, this will hurt the poor and the middle class, who face a disproportionate burden associated with cuts to entitlement and means-tested programs. When the tax cuts are eventually paid for, the vast majority of American households will be worse off.

What this Means:

After 35 years of increasing income inequality, the Tax Cuts and Jobs Act makes our tax system less progressive. The overall package of tax cuts tilts most benefits towards the wealthy. Average workers could benefit from the TCJA business tax cuts if they result in large increases in investment that translate into gains in worker productivity and wage growth. While the jury is out on how effective the TCJA will be in this regard, early signs do not indicate important changes in companies’ sharing their profits with workers or substantial changes in investment or wage growth trends. A full reckoning of the effects of the TCJA on average workers must also account for the larger policy environment. Middle class workers are hurt by cuts in health insurance funding since this increases health insurance premiums and causes fewer Americans to be insured. In addition, deficit financed tax-cuts that drive up government debt limit the ability of fiscal policy to respond to the next recession, making it more challenging to shorten its duration or cushion its impact on Americans. The current expansion is already much longer than average, and recessions always do arrive. Beyond that, deficit-financed tax cuts must ultimately be paid for, and higher taxes and/or reductions in government spending are both likely to be harmful to middle class workers.