Is China a Currency Manipulator?

Fletcher School, Tufts University

The Issue:

Donald Trump has said that, upon taking office, he will declare China a currency manipulator. Many Americans, understandably angered by factory closings and job loss seemingly due to Chinese competition, appear to support this. An artificially cheap yuan enables Chinese exporters to unfairly undercut American manufacturers. And, indeed, a superficial look might bolster the charge: the yuan fell by more than 6.5% over 2016 and is at an eight year low against the dollar.

But currency manipulation is not like pornography – you don’t know it when you (think you) see it.

The Facts:

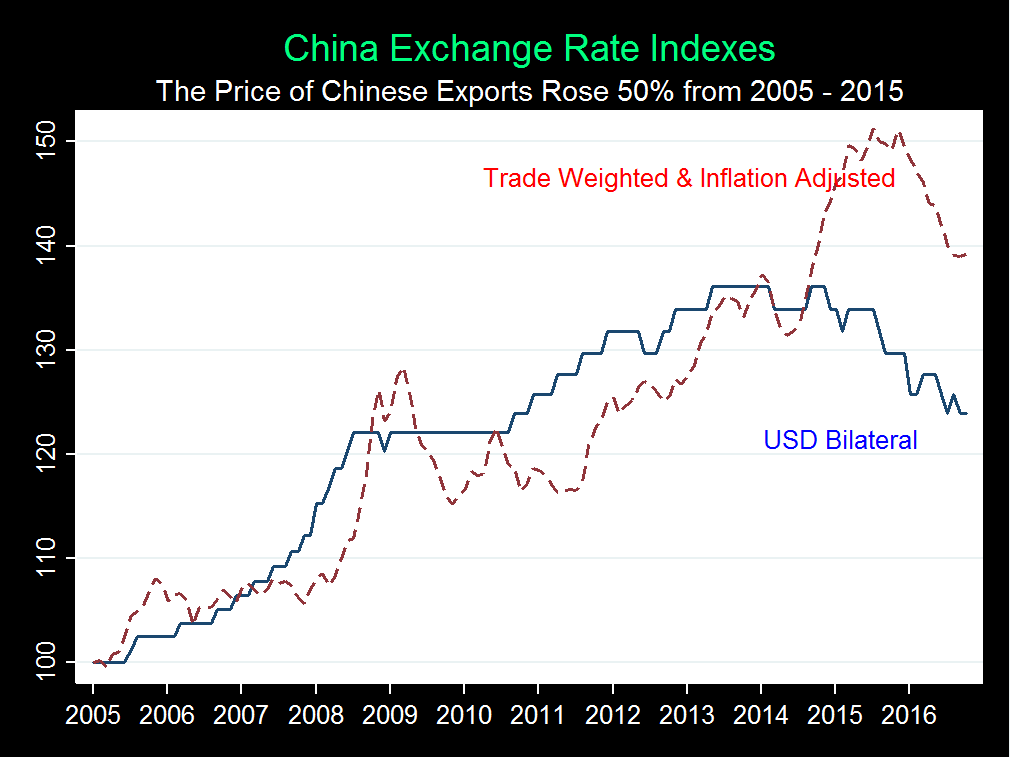

- A study of longer-term trends shows that the relative price of Chinese goods has in fact risen significantly over the past decade. The solid line in the accompanying chart shows that the yuan has strengthened 25 percent against the dollar in the last 10 years, even given its recent decline. And that is not the only factor that has been pushing up the price of Chinese exports. The cost of manufacturing inside China has been steadily rising, in part because Chinese workers have been demanding and getting higher wages. Meanwhile, the yuan has been strengthening even more against currencies other than the dollar, largely because the US economy has done much better in emerging from the recent global recession than most of the rest of world. The dashed line in the graph reflects these added factors, adjusting for Chinese prices and taking into account China’s trade links with countries other than the US. As it shows, the overall real relative price of worldwide Chinese exports has risen by about 40 percent in the past decade, even given this year’s decline. The price of Chinese exports, in other words, has risen considerably.

- The figure shows that the yuan has weakened over the past year. This does not represent an effort to manipulate the currency to promote Chinese exports. Rather, Chinese authorities have actually been trying to stem a free fall of the currency in the wake of economic disruptions in the country, including concerns about the solvency of the banking sector. This might be considered “manipulation,” but the effect is the exact opposite from what many of us—and apparently Mr. Trump—believe.

What this Means:

Looking forward, administration officials should be wary of too freely tossing around the term “currency manipulator,” and not just because the evidence for the most celebrated example does not stand up. Tax cuts and rising interest rates in the United States are likely to strengthen the dollar, while ongoing financial challenges in China, including in its banking system, could weaken the yuan. But, were these currency movements to occur, they would not reflect concerted efforts to promote Chinese exports, rather, like most changes in exchange rates, they would reflect underlying macroeconomic conditions.