Oil Prices: Is it Déjà vu All Over Again?

Tufts University

The Issue:

Oil prices topped $70 a barrel in May 2018 for the first time since late 2014. Rising gas prices at the fuel pumps were not far behind. Also not far behind were the politicians from both sides of the aisle blaming the Organization of the Petroleum Exporting Countries (OPEC) and Saudi Arabia for driving prices up, bringing to mind the the tensions with OPEC of the early 1970s. Prices dropped somewhat after May 25th, when press articles reported that Saudi Arabia and Russia were nearing an agreement to boost production, but they remained significantly higher than a year ago. If you want to really understand what is driving oil prices up, there is much more behind the trend than Saudi Arabia or OPEC.

The economic crisis in Venezuela and the U.S. withdrawal from the Iran nuclear deal have contributed to rising oil prices.

The Facts:

- Oil prices in May were 50 percent higher than they were last year. The price of West Texas Intermediate (WTI) oil, a benchmark price for U.S. oil topped $72 a barrel on May 21. That’s a fifty percent increase since its recent low of $47 in April 2017. The story is similar for Brent, a benchmark price for oil sold in Europe.

- A deal between OPEC and non-OPEC countries, including Russia, to decrease oil production by around 2 million barrels per day had been in effect since January 2017. The deal sought to increase oil prices by reducing a supply glut (see here). Global oil production is a little over 80 million barrels per day, so the planned cuts, if enforced as planned, represented just a little over a 2 percent reduction in production.

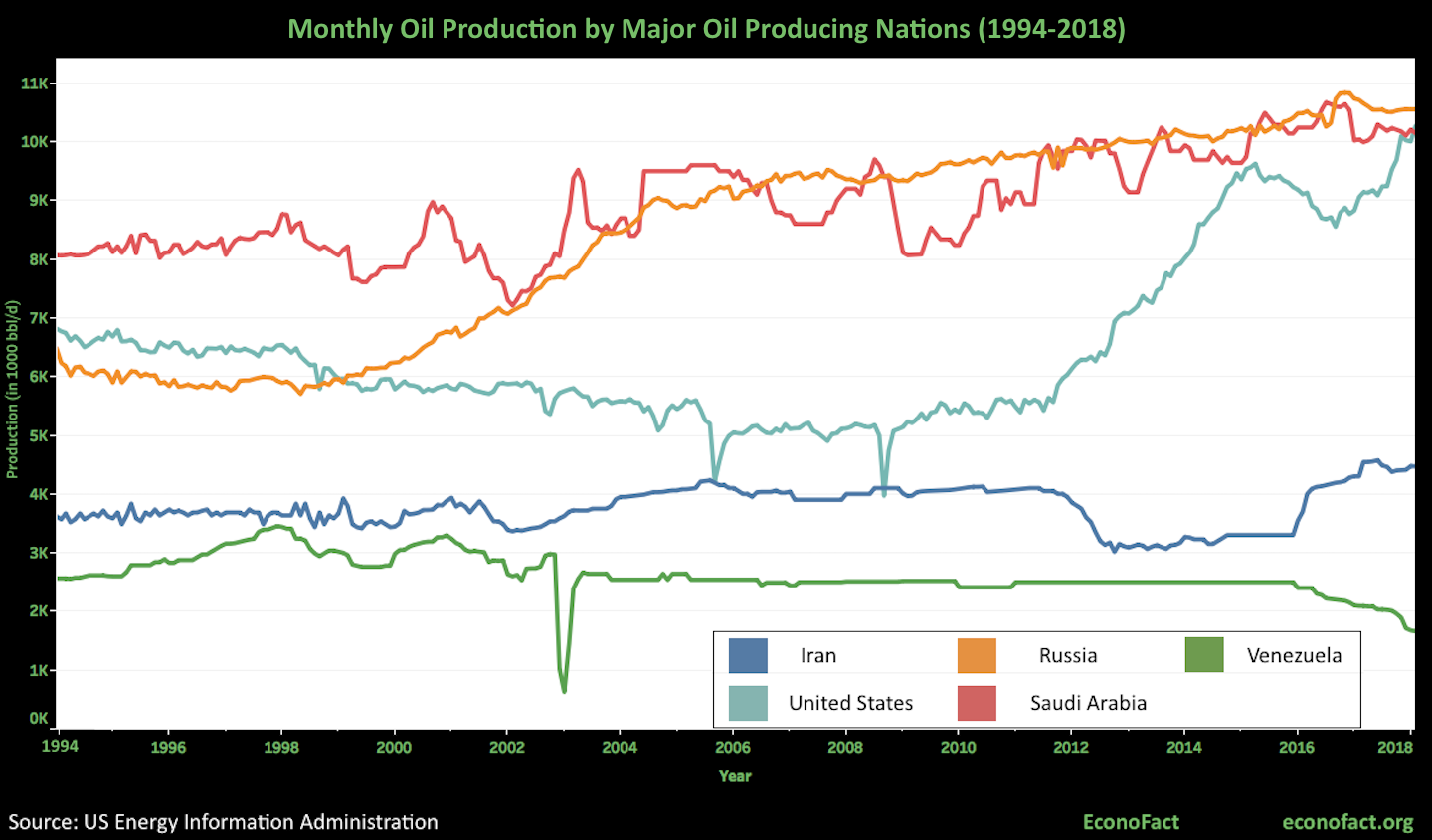

- The oil production landscape has changed dramatically over the past decade and the United States has become a big player among oil producers. Production in the United States has grown strikingly to the point of rivaling the levels of the other two world leaders in production: Saudi Arabia and Russia. U.S. production exceeded Saudi production in February 2018, the legacy of the fracking and shale oil revolution in the United States, a legacy that has contributed to inexpensive gasoline at the pump for the last eight or so years.

- But Saudi Arabia continues to be a big producer and when OPEC is joined with Russia as a group they are even bigger. OPEC and Russia as a group produced 46 million barrels of oil per day (bbl/d) in February 2018. Have they managed to curtail production as their deal for 2017 intended? According to a Bloomberg analysis, Saudi Arabia has cut production by roughly one-half million barrels per day, in line with their production reduction target. Russia, in contrast, has failed to hit its reduction target of 300 thousand barrels per day. Many other OPEC countries failed to cut production as promised. Meanwhile U.S. production has more than offset Saudi cuts so that oil production from Saudi Arabia and the U.S. combined has increased by seven percent since January 2017.

- Why were oil prices rising so dramatically then? In large measure, the answers lie with the economic crisis in Venezuela and the Trump administration's decision to withdraw from the Iran nuclear deal. Nicolás Maduro, the increasingly dictatorial leader of Venezuela, has led the country to economic ruin. Venezuela’s national oil company, PDVSA, was historically led by highly respected technocrats and oil engineers. PDVSA contributed greatly to the country’s wealth and prosperity over the years. Hugo Chavez, Maduro’s predecessor, interfered in the oil company’s operations and managed to drive away much of the senior leadership. Maduro has accelerated the slide. The country’s fiscal situation is so dire that PDVSA can’t make needed investments to maintain its aging infrastructure. The result? A precipitous decline in oil production starting in mid-2015 that saw its production fall by one-third. Just in the last twelve months, Venezuela’s production fell by over 400 thousand barrels per day, the largest decline among all oil producing countries. In addition to Venezuela's production demise, the Trump administration's decision to withdraw from the Iran nuclear deal and reimpose sanctions jolted global oil markets. Since the nuclear deal was signed, Iranian production has increased by nearly one million barrels per day. Analysts surveyed by Platts think the reimposition of sanctions will cut Iranian production by less than 500 thousand barrels per day, but there is much uncertainty with analyst estimates ranging between 100 thousand and 800 thousand barrels per day. Meanwhile, the economy is strengthening and fueling higher demand for oil. Given inelastic demand and the time it takes to bring new oil on-line in response to higher prices, it’s no surprise prices have risen.

- Will prices go higher? It’s never smart to try to predict future oil prices. U.S. jawboning has clearly led the Russians and OPEC to boost production to stop prices from rising further (see here). But here’s something to consider: Shale oil production in the United States can be ratcheted up fairly quickly. One analysis of U.S. oil production finds that a ten percent increase in price leads to a seven percent increase in drilling activity. Drilling activity is up in the United States and shale oil should begin to offset production declines elsewhere in the world. One reason for OPEC and Russian restraint is the recognition that high prices will trigger major increases in U.S. shale production, something OPEC and Russia would like to avoid. Major increases in U.S. production are possible but beware the bottlenecks. Pipeline constraints are bottling up oil in the West Texas Permian basin, as evidenced by the sharp price differential of $15 a barrel between oil sold in Midland Texas and oil sold in Houston. Midland drillers are struggling to get their oil to refineries in the Houston area and until they can, oil prices in the Permian basin will be depressed. Given the price differential, they will eventually figure out a way to get their oil to market. But it could take a few months.

What this Means:

What should we be doing in the face of rising oil prices? Jawboning OPEC to increase production will only get us so far. Even though the United States has become a major oil producer, it continues to be a major consumer as well. Over seventy percent of oil in the United States is used in the transportation sector. If we really want to insulate ourselves from higher oil prices, we need to wean ourselves off oil. The best way to do that is to increase our fuel economy and speed the penetration of electric vehicles in the transportation fleet (less than one percent of oil is used to produce electricity). Unfortunately, the Trump administration’s rollback of CAFE fuel economy standards along with calls for cuts to energy R&D are taking us in precisely the wrong direction.