Who Owns Us? Foreign Investment and Trade Deficits

Fletcher School, Tufts University

The Issue:

Peter Navarro, head of the White House Council on Trade, argues that trade deficits not only reduce America’s economic self-reliance but could also pose a threat to national security. He warns in an op-ed in the Wall Street Journal that China and other trading partners use proceeds from export sales to buy U.S. companies and technology: "Suppose the purchaser is a rapidly militarizing strategic rival intent on world hegemony. It buys up America’s companies, technologies, farmland, food-supply chain—and ultimately controls much of the U.S. defense-industrial base. How might that alternative version of conquest by purchase end for our sons and daughters? Might we lose a broader cold war for America’s freedom and prosperity, not by shots fired but by cash registers ringing? Might we lose a broader hot war simple because we have sent our manufacturing and defense industrial base off shore?"

The Facts:

- Navarro is correct in that trade deficits are accompanied by sales of domestic assets to foreigners: this is how a country finances buying more goods and services from the rest of the world than it sells abroad. A country must pay for its net purchases from abroad in much the same way that an individual who spends more than she earns has to borrow (the equivalent of selling IOUs). But it is incorrect to say that a trade deficit causes a capital account surplus, that is, a net increase in foreign ownership of United States assets. Both the trade deficit and the capital account surplus reflect underlying economic conditions. Just as having a trade deficit does not cause the economy to grow more slowly (see this EconoFact memo), the capital account surplus reflects in part the fact that the U.S. is an attractive place for foreign investment and foreigners have, for decades, seen the dollar and U.S. Treasury bills as safe place to hold some of their assets. The net inflow of foreign capital allows the United States to invest more than it would if it were limited to the domestic pool of savings.

- The assets that foreigners buy include U.S. Treasury Bills, corporate bonds, stocks, real estate and green field investments (where foreign companies build new plants and production facilities). Foreign Direct Investment, which is the source of concern in Navarro’s opinion piece, is foreign purchases of domestic assets that offer some degree of managerial control. It can take the form of an acquisition of an existing company, the establishment of a new company, or the expansion of an existing majority-owned foreign company. Foreign direct investment in the United States in 2015 was $420 billion, with the vast majority representing acquisitions ($408 billion), while new investments were $11 billion, and expansions of exiting majority foreign-owned firms were $1.4 billion. Some of the acquisitions numbers probably include corporate tax inversions which are transactions U.S. multinationals undertake, effectively becoming subsidiaries to foreign companies, as a way to change tax jurisdictions and reduce corporate taxes.

- How much of U.S. productive capacity is owned by foreigners? Foreign direct investment represents the increase in foreign ownership in a particular year. The overall presence of majority-foreign owned businesses in the United States is the net accumulation of direct investment over time. The estimated overall accumulated foreign direct presence in the United States, based on a historical cost basis, was $3.1 trillion in 2015. This is about 12 percent of the combined value of the New York Stock Exchange and the Nasdaq, and clearly a smaller proportion of the value of all companies since many are not listed on either of these stock exchanges.

- International companies such as Siemens, Unilever, and Toyota that invest in operations in the United States employ American workers. The Commerce Department estimates that 6.1 million U.S. workers were employed by companies that were majority owned by foreign entities in 2013 (the latest year in which they could make this estimate) and more than one-third of these jobs were in manufacturing. The average compensation for these jobs ($80,000) was higher than the average compensation for all U.S. workers ($60,000).

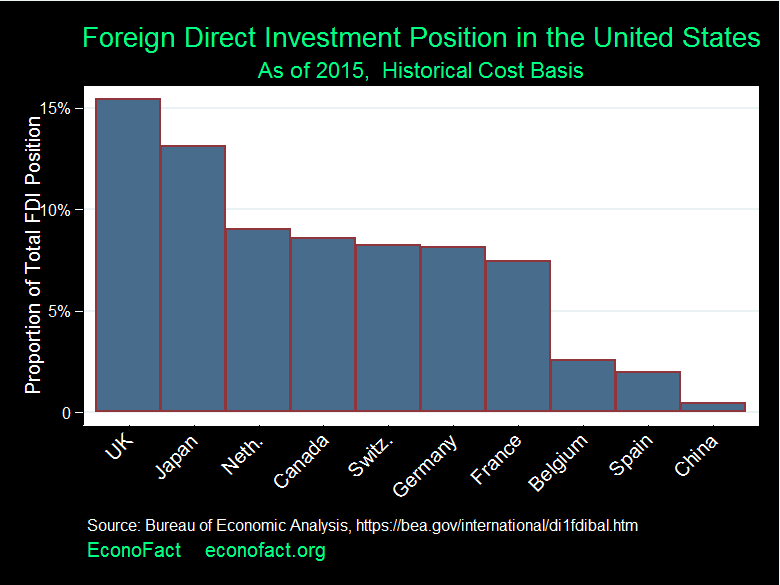

- Navarro expressed national security concerns about foreign ownership, of losing “a broader hot war.” A relevant fact here is the ownership of U.S. firms by different countries. About 69 percent of the $3.1 trillion cited in the previous point was owned by Europeans, with Great Britain having the largest ownership of any country within that group ($484 billion, or 15 percent of all direct ownership). Another 13 percent is owned by Japan. Chinese direct ownership in the United States represents $15 billion, or 0.5 percent of all foreign ownership (see chart.)

- There are safeguards in place to ensure that foreign ownership does not threaten the national security of the United States. The Committee of Foreign Investment in the United States (CFIUS) scrutinizes prospective foreign direct investment that may have national security implications. CFIUS consists of nine members, including the secretaries of commerce, defense, energy, homeland security, state, and treasury; the attorney general; the U.S. trade representative; and the director of the Office of Science and Technology Policy. It was created in 1988 by the Exon-Florio amendment. CFIUS review has expanded, even before the new administration took office, from its traditional focus on industries like aerospace and semiconductors to sectors like information technology and biomedical.

What this Means:

An “investment surplus” can be beneficial if it is funding the long-run productive capacity of a country. Access to foreign capital inflows allows the government, companies, and individuals to borrow at lower interest rates than would be the case if borrowing were limited to the domestic pool of savings. However, these same circumstances can also contribute to consumption spending that does not expand productive capacity. The extent to which foreign capital flows support investment versus consumption determines whether paying back in the future will be easy or painful. Concerns about “a rapidly militarizing strategic rival intent on world hegemony” buying up American assets ignores the fact that European countries and Japan are the primary foreign owners of US assets that offer some degree of managerial control and that Chinese ownership of U.S. productive capacity is a tiny fraction of all foreign ownership. Also, CFIUS guards against direct investment that might have consequences for national security or that may have other adverse consequences for the nation. Navarro’s comments ignore both basic economic relationships and the actual statistics of ownership by countries, as well as the presence of safeguards like CFIUS.