Global Repercussions of the Strong Dollar

University of Michigan

The Issue:

The Issue:

The dollar has strengthened sharply with respect to the currencies of many industrialized nations and emerging markets to reach a 20-year high. This appreciation of the dollar is viewed as a major global challenge for most countries, especially emerging market economies. In the past, many countries would have embraced a strong dollar; indeed, emerging market countries like China often intervened in foreign exchange markets in the hopes of weakening the value of their currencies to gain trade advantage. But today both advanced and emerging countries alike are struggling against further depreciation of their currencies for a range of reasons.

A strong dollar feeds into inflation pressures abroad and makes it more difficult to service dollar-denominated debt.

The Facts:

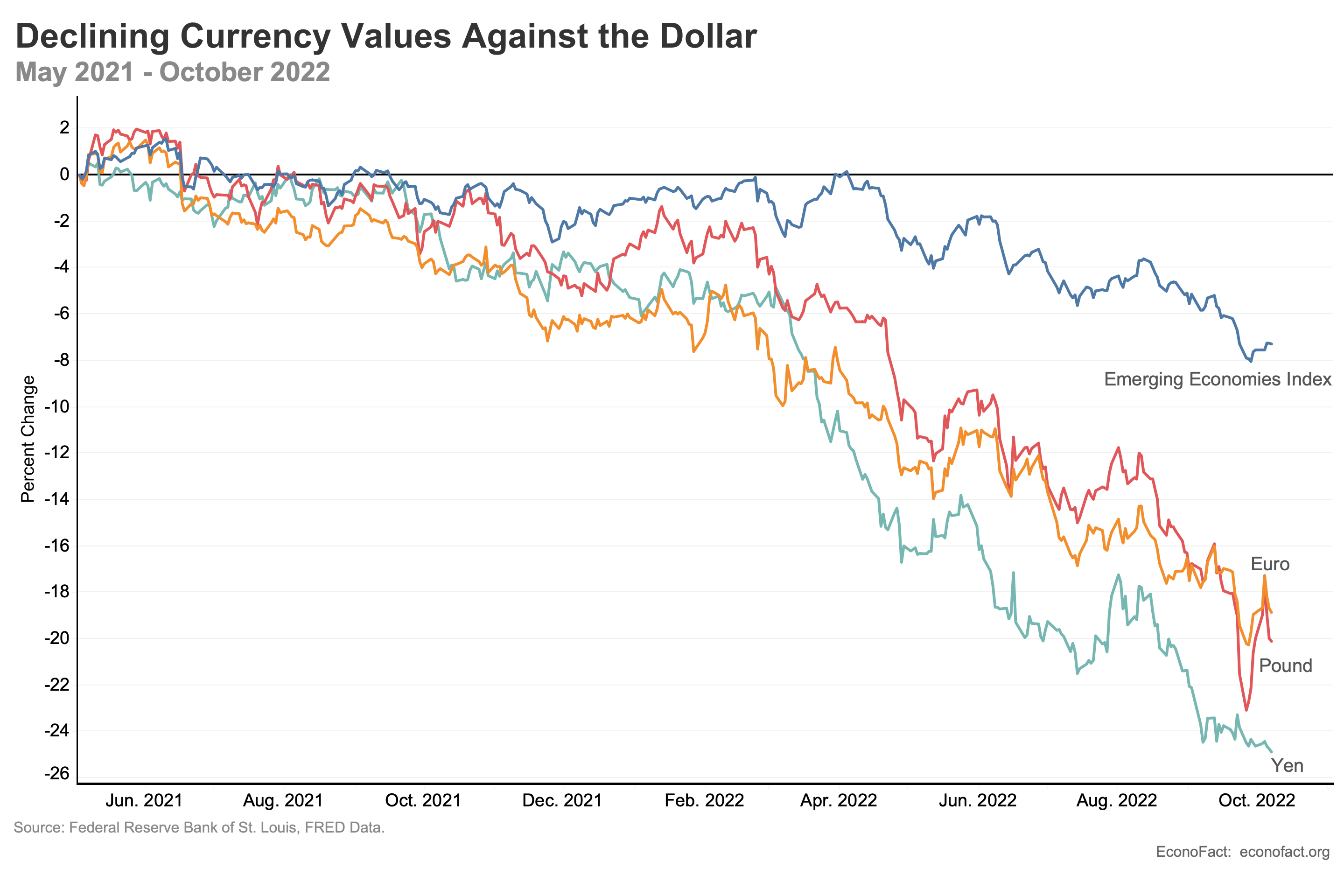

- The dollar has strengthened considerably. Since May of 2021, the value of the euro with respect to the dollar has weakened by 19 percent, the British pound by 20 percent, and the Japanese yen by 25 percent. There has been a similar, albeit smaller, strengthening of the dollar against the currencies of emerging markets (see chart).

- The strength of the dollar can be traced to the relative attractiveness of United States assets. The dollar strengthens when investment funds flow into the United States because the purchase of American assets requires acquiring dollars. The Federal Reserve has been raising interest rates more aggressively than other advanced economy central banks, including the European Central Bank, the Bank of England, and the Bank of Japan, making bonds denominated in dollars relatively attractive as compared to bonds denominated in these other currencies. Prospects for growth in the United States, while lowered by the inflation-fighting interest rate increases by the Fed, are still brighter than those in many other countries – for example, disruptions in gas and oil supplies due to the war in Ukraine affect European countries more severely than the United States. The dollar is also considered a “safe haven” currency and, with the war in Ukraine, there has been a flight to dollars, driving up the U.S. exchange rate.

- The strong dollar feeds into inflation pressures abroad. When a country’s currency weakens against the dollar, the price of imports from the United States rises, putting pressure on prices. On average, the pass-through of a 10 percent dollar appreciation into inflation abroad is 1 percent. This pressure extends beyond the direct import of goods from the United States: the prices of commodities like oil, wheat and metals are quoted in dollars, so a stronger dollar means a higher price for these things. Further, because food and energy expenditures make up a larger share in emerging economy consumption, increases in the dollar prices of these commodities significantly increases their cost of living.

- A weaker currency can help promote a country’s exports and the sales of its import-competing companies – but there are other effects as well that mitigate these trade advantages. The same company that exports products may also depend on imported inputs for production. The advantage from a cheaper price of a company’s product, through currency depreciation, may be mitigated, or even reversed, through higher costs of production due to the increased home-currency price of inputs that are priced in dollars – both imported inputs from the United States and, even more importantly, commodity inputs that are priced in dollars. For example, a weaker yen raises the cost of production of Sony’s PlayStation consoles, and the clothes sold by Asia’s biggest clothing brand, Uniqlo. The effect of a weaker currency is more complicated than the simple depreciation-export linkage.

- A strong dollar makes it more difficult to service their debt for those who have borrowed in dollars but whose receipts are in another currency. This is a particular problem for governments and companies in emerging economies because most of their borrowing is in dollars. In the years following the Global Financial Crisis in 2008 emerging economies experienced strong capital inflows, global liquidity was high and interest rates were low in advanced economies, making emerging economies attractive places for investors. Emerging economy external borrowing grew and more than 80% of this debt was denominated in foreign currency, mostly in U.S. dollars. The pandemic brought a sharp reversal in capital flows, many emerging economies experienced sovereign rating downgrades, and countries with high levels of external debt relative to foreign exchange reserves suffered large-scale capital outflows and dramatic currency depreciations.

- A stronger dollar has been associated with a range of problems for emerging market economies, including declines in output, consumption, investment and government spending. A recent analysis by Maurice Obstfeld and Haonan Zhou finds that a 10 percent dollar appreciation leads to a real GDP decline of about 1.5 percent relative to trend in emerging market economies. They find that the adverse impacts of a strong dollar are largest for countries that peg their exchange rates, that have not adopted inflation-targeting monetary frameworks, and that have high levels of dollar debt. The negative impacts of a strong dollar for emerging economies are heightened in the current context because many of these countries increased their public- and business-sector debt levels due to the pandemic. The strong dollar raises the real value of dollar debts, higher interest rates raise debt servicing burdens, and slower growth reduces business profits and government tax receipts.

- Central banks respond to inflation, as well as currency weakness, by raising interest rates – but this has the effect of slowing the economy, and perhaps leading to a downturn. The Federal Reserve undertook a more aggressive stance towards inflation earlier than the European Central Bank, the Bank of England, or the Bank of Japan. The relative strength of the U.S. economy has allowed the Fed to continue raising interest rates to fight inflation, but there is a danger that these actions, together with similar policies taken by other central banks, could jointly create an unnecessarily sharp global recession. Central bank mandates require that policy actions be based on domestic conditions, making it difficult to fully internalize the spillover effects of each other’s actions, potentially leading to an overly aggressive global monetary tightening cycle.

- What can countries do to counter a strengthening dollar? Several countries, including Japan, have recently intervened in foreign exchange markets to strengthen their currencies by selling dollar assets. Foreign reserves held by emerging economies fell by more than 6 percent in the first half of 2022 as a result of intervention efforts to defend their currencies against a rising dollar. These unilateral efforts have temporarily slowed depreciations, but have not reversed the dollar’s upward climb. Countries may also work in coordination to intervene in order to stabilize currency markets. There is historical precedent for coordinated efforts to stop an ascendant dollar: In 1985, the U.S., Japan, West Germany, France and the U.K. agreed to a joint intervention in currency markets in what became known as the Plaza Accord. The countries proceeded to sell dollars in exchange for other currencies in the foreign exchange market and the dollar’s value declined (see here). But, unlike today, there was widespread consensus that the dollar’s value in 1985 exceeded that consistent with underlying fundamentals, so it is less clear that a “new Plaza Accord” would be as effective in the present environment.

What this Means:

Large swings in exchange rates can lead to coordination efforts, as well as currency wars, where countries go-it-alone against each other in efforts to manipulate the value of their currency at the expense of other countries. Outside the U.S. there is building enthusiasm to launch another Plaza Accord-style coordinated intervention effort to bring down the value of the dollar. What makes the current context different from the dollar appreciation in the 1980s, is that there is little evidence of a dollar bubble today. The dollar is strong not because of over-exuberant market behavior, but because the U.S. economy is expected to be stronger than most other economies over the foreseeable future, together with higher dollar interest rates, and the safe haven status of the dollar. Dollar strength may nonetheless become a concern for the U.S. if the global economy continues to falter and financial conditions worsen, leading to lower U.S. export sales and emerging economy debt defaults. If the global repercussions of the strong dollar become too costly, it will be in the U.S.’s best interest to join the effort to bring it down.