College Financial Aid: What You Don’t Know Can Cost You

Wellesley College

The Issue:

Sky-high listed college costs at many elite private colleges and universities are clearly unaffordable for the vast majority of the population and dissuade many people from even applying to these schools. Yet the widespread availability of extensive financial aid at many of these institutions brings an elite college education within reach for well-qualified students. However, many of those who stand to benefit are unaware of the option. There is an effort to address this problem; federal legislation mandates that every college and university post a “net price calculator” on their web sites, designed to provide students/families with estimates of their expected cost based on their own finances. But these on-line tools are often difficult to use.Lack of information regarding financial aid reduces the likelihood that well-qualified students from low and moderate income families attend colleges that their families could, in fact, afford.

The Facts:

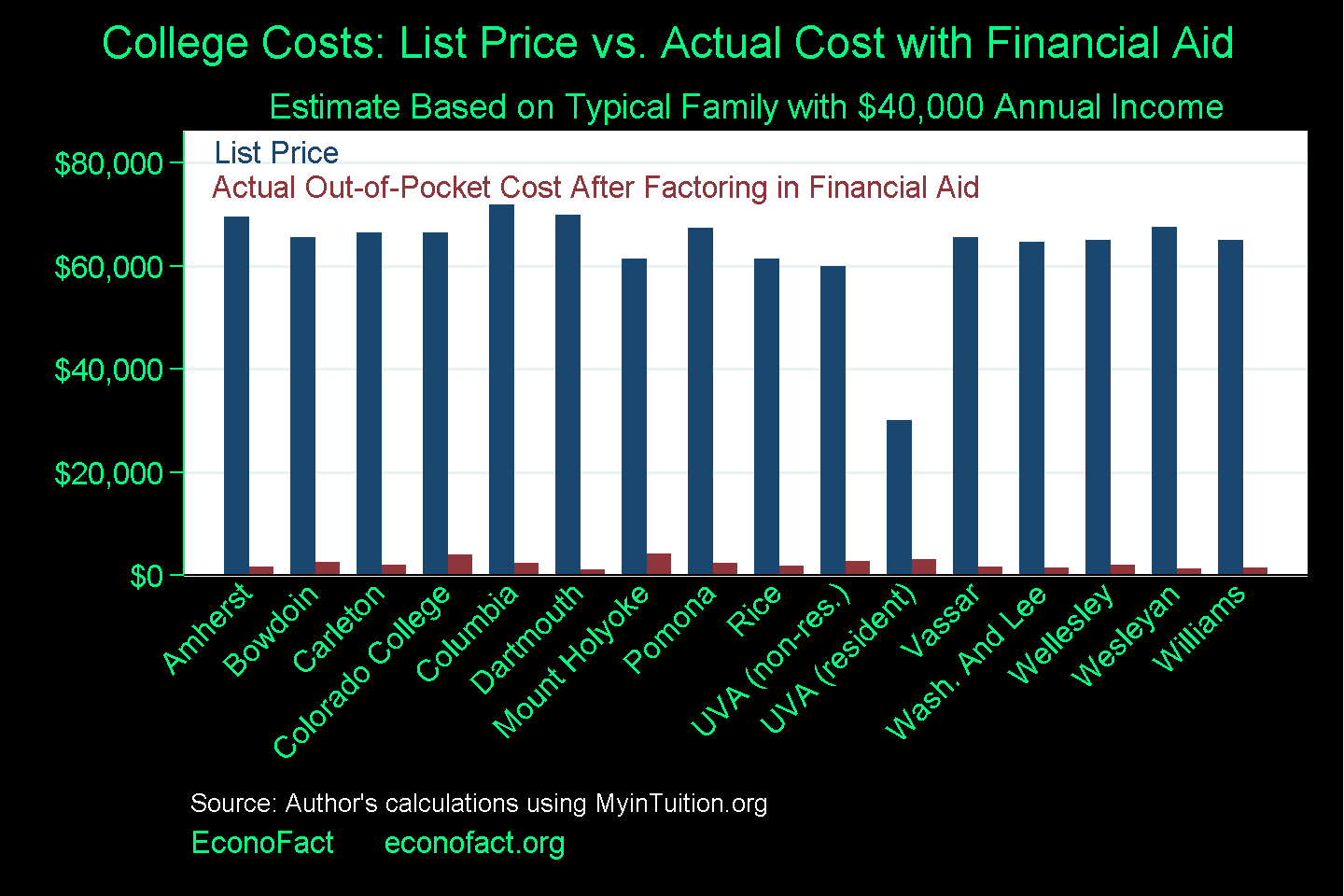

- Stated college costs including room and board approach $70,000 or more at the nation’s leading private higher educational institutions. The median annual income of families with college-age children is $68,000 and their median net worth is $55,000; half of that is home equity. For families with those financial resources, and certainly for those with fewer, those prices are clearly unaffordable.

- Yet extensive financial aid is available at many of these institutions that substantially reduce their cost, bringing them more in line with a family’s finances. At a typical elite institution, students whose parents earn less than the median are often expected to pay perhaps $2,000 out of pocket (often with an expectation that the student can earn that in a summer job), take a work-study job during the school year to pay around another $2,500, and, at some of these institutions, take out loans of no more than $5,500 per year (these loans may be less, or even zero, at a select few of these institutions). For example, the estimated average out-of-pocket cost, including room and board, for a typical family that earns $40,000 per year is about $2,200 at a group of colleges and universities with an average list price at the private colleges of $66,300 (see chart). For lower income families, these burdens are not trivial, but may be manageable. Given the substantial return to a college education and the premium associated with attending an elite institution, this represents a great investment.

- Students and their families, especially those from low-income households, are generally poorly informed about the availability of financial aid. Survey evidence indicates that the majority of students of college-going age only know the stated sticker price that colleges charge. This misinformation reduces the likelihood that well-qualified students attend those institutions. One study found that almost half of high-achieving, low income students attend non-selective institutions.

- Research suggests that providing more information to prospective students regarding what it would actually cost to attend will have a substantive impact on their higher-education decision-making. In one experiment, students who were offered estimates of the cost of attending nearby colleges after incorporating financial aid and assistance completing the FAFSA form were 29 percent more likely to subsequently complete two years of college. In another experiment, providing application assistance, guidance on the actual cost of college, and application fee waivers for high-achieving, low-income high school seniors led them to apply to schools that better match their abilities, with higher four-year graduation rates, instructional spending, and median SAT scores. A survey of participants conducted after that experiment indicates that better information regarding financial aid was an important factor in improving student outcomes.

- In principle, federal legislation has already mandated the introduction of tools that address this information problem. As of 2011, every college and university has had to post a “net price calculator” on their web sites, designed to provide students/families with estimates of their expected cost based on their own finances. The “net price” includes direct payments from the student and his/her family plus expected loans and the proceeds from a work-study job. These net price calculators are now in place, but they are often difficult to use, frequently requiring users to provide information from tax forms that they may be reluctant to dig out and may not understand.

- One alternative way to simplify access to college cost information is an approach that is being tried by Wellesley and a handful of other colleges that have taken steps on their own to introduce easy to use cost calculators. The online tool, which I created and which has been financed by Wellesley College, MyinTuition, simplifies the process. It requires users to enter just the most common types of financial resources (income, home equity, cash in the bank, and savings in investment accounts). Demand for the tool has been incredibly strong. In the six weeks since its recent expansion to 15 schools, 20,000 users have obtained over 35,000 estimates. It takes an average of 3 minutes to complete and 91 percent of those who start the tool finish it. Although purely descriptive, applications at Wellesley, Williams, and the University of Virginia, all of which have been using MyinTuition at least since the fall of 2015, jumped 13 to 23 percent last year. In each case, around 90 percent of that increase came from students requesting financial aid.

What this Means:

One critical component of any attempt to increase access to college for low and moderate income students is better information regarding costs. Policies that reduce the price are only beneficial if students know what those prices are. Students from low-income households benefit from mentors who could advise them about college choice and college financing. Greater transparency about the true costs (and benefits) of different colleges will aid students, their parents, and the mentors who assist them, to make better-informed choices. Federal proposals to improve already mandated net price calculators are one approach to address this problem. Private market solutions, like further expansion of MyinTuition, may address the problem as well. Efforts to level the playing field for college affordability will only work if the true price of attending these colleges, inclusive of the available financial aid to low and moderate income households, is widely known.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.