How Should We Pay for Our Infrastructure?

Brandeis University

The Issue:

A well-functioning society requires adequate infrastructure facilities such as roads, bridges, water systems, ports, airports, schools, and police stations. But the current stock of American infrastructure is now widely acknowledged to be deficient. The American Society of Civil Engineers has given the United States’ infrastructure a grade of D+, and the need for upgrading the country’s infrastructure seems to be an issue that both Democrats and Republicans agree upon. President Trump has repeatedly expressed the intention to craft a $1 trillion plan for infrastructure investment. This plan has resonated with the public: three-quarters of respondents to a Gallup poll favored greater spending on infrastructure.

While there is broad support for infrastructure investment, there is much less clarity and agreement around how to finance this infrastructure push.

The Facts:

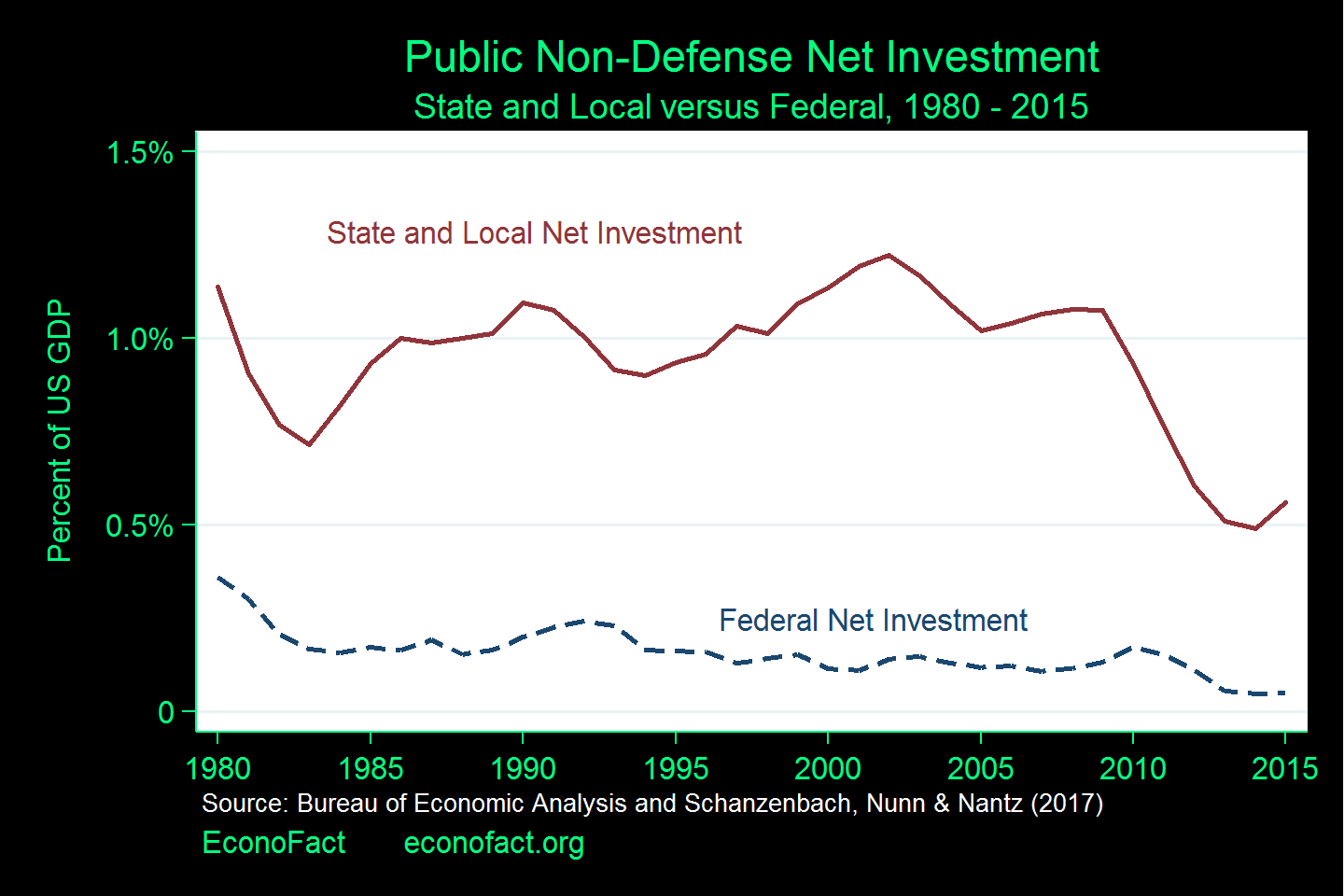

- Public investment in infrastructure has declined over time: public non-defense net investment fell by more than 50 percent from 2002 to 2015 (see chart.) State and local governments account for the largest share of infrastructure spending, but the federal government also plays an important role with direct investment, matching grants, and tax incentives (see this Hamilton Project report for details and breakdowns on federal, state and local infrastructure funding.)

- Public sector involvement in infrastructure construction, operation, and maintenance is common because infrastructure frequently has social benefits that go beyond the profits that a private company could capture. For example, a sewer system that mitigates the risk of directly contracting water-borne diseases like cholera or typhoid through ingesting tainted water also benefits those who live beyond the system's area of operation: even though they are not direct users of the sewer system, they have a lower risk of contracting these contagious diseases because of the sewer system’s existence. In a purely private economy, without shared investment, there will be undersupply of infrastructure services such as those provided by sewers and water systems that have this kind of shared public good component. In addition, there are reasons to believe that infrastructure investment contributes to economic growth by helping firms and workers become more productive — although the magnitude of this effect is subject of debate amongst economists (see here for David Aschauer's widely-cited paper that finds strong links between infrastructure investment and productivity growth and here for an assessment of more recent studies).

- Financing for infrastructure comes from a wide range of sources, some of which are direct – for example state or local spending to construct a bridge or a road. Financing can take different forms such as using debt, charging usage fees (such as tolls), matching grants, and partnerships with private firms (see here for a breakdown of infrastructure financing sources.)

- The federal tax exemption for the interest paid by municipal bonds is an extremely important indirect form of support for infrastructure investments. These municipal bonds finance almost a third of state infrastructure projects, and the fact that their interest is tax-exempt means that they can pay lower yields than otherwise equivalent taxable bonds. These lower yields are a subsidy whose value is split between the municipalities that issue the bonds and investors who buy them. This subsidy facilitates infrastructure investment and the benefits which that investment brings. The tax exemption has made municipal bonds a particularly attractive asset class for high-income households: since they pay higher tax rates, they get a greater benefit from tax-exempt bonds than households who pay lower tax rates. However, the benefits from the municipal tax exemption are more democratically distributed than might appear in a simple analysis when the gains to households that benefit from infrastructure facilities — such as those with several school-age children — are considered (see this study for instance). This subsidy comes at a cost in foregone tax revenues. The conventional estimate of this cost was $29 billion in fiscal 2014. However, the elimination of the tax exemption on municipal interest would likely lead to shifts in household portfolios and these shifts would mean that this conventional estimate of the cost of these subsidies is too high (see a discussion in this study).

- An alternative method of financing infrastructure is through public-private partnerships (often called P3s) in which the private sector partners with states and localities to jointly fund projects. While the initial public capital outlay for the project can often be smaller than it would have been had the investment been entirely financed with public funds, the private sector partner will expect to recoup its investment through user fees, tolls or other means. These P3 projects involve a contract between a state or a locality and a private entity to construct, operate, or maintain some component of infrastructure. The actual nature of the contract can take a variety of different forms, depending upon the project. For example, at the end of 2012, the Bayonne, New Jersey Municipal Utilities Authority entered into a 40-year concession with the private equity firm Kohlberg Kravis Roberts & Co (KKR) to invest in and manage that city’s water system. Other P3s have involved toll roads, airports, and other varieties of public investment. Recent research suggests that cities are more willing to privatize services for which it is easier to write and administer performance-based contracts.

- There has been recent support for P3s, including by President Trump. But P3s are not a panacea. Designing, negotiating, and managing contracts between public authorities and private service providers can be difficult, and the structures can be vulnerable to opportunistic behavior both on the private and on the public sides. For example, public support can at times represent a giveaway to the sponsors of projects that would be undertaken by the private sector, even in the absence of that public support. In addition, P3s can enable hidden borrowing by states and localities for reasons not linked to infrastructure. States and localities are, by-and-large, not supposed to borrow in order to finance operating deficits, but P3s can sometimes be structured in ways that amount to an end-run around these balanced budget restrictions. Chicago’s grant of a 99-year concession to operate and collect tolls on the already-built Chicago Skyway, and the use of the $1.8 billion upfront cost for budget relief, is an example of the use of a P3 to achieve budget relief – in ways that run counter to the spirit of balanced budget requirements - rather than to stimulate investment.

What this Means:

The American Society of Civil Engineers estimates that it would take $2 trillion to bring United States infrastructure up to a state of good repair. Infrastructure’s contribution to economic growth is the source of some debate, but, even given this, it has a role in the improvement of the quality of life through its benefits on health, as with the provision of water and sewer services and decreasing transportation accidents, as well as on convenience, such as through reducing commuting times. Any discussion of infrastructure must include a discussion of the means of financing it. The traditional method of allowing for tax-exempt bonds has distributional aspects, favoring higher-income households that benefit disproportionately in a progressive tax system. Public-Private Partnerships offer an alternative method, but there are challenges associated with this method as well. The prospect that P3s may become an even more important vehicle for infrastructure finance places a premium on unbiased analysis of the terms and implications of these deals.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.