Will Tax Reform Have an Impact on Charitable Giving?

Texas A & M University

The Issue:

Giving by individuals accounts for nearly three-quarters of charitable giving in the United States, over $280 billion in 2016. Changes to tax policy can have an effect on the incentives individuals and households face when making the decision of how much to give to charity. The U.S. tax code currently encourages charitable giving by individuals who itemize their expenses. Recent tax reform proposals differ widely on how to treat charitable giving.Even if the charitable tax deduction is not altered, changes to other aspects of the tax code such as the value of the standard deduction and the top tax rate can potentially influence charitable giving.

The Facts:

- The deduction for charitable giving is intended to subsidize nonprofit organizations and encourage activities that provide societal value. The reasoning is that these organizations may supplement or substitute for government activities while potentially being more responsive and directly accountable. The charitable giving deduction was established shortly after the income tax itself, by the War Revenue Act of 1917. Currently, it is capped at 50 percent of adjusted gross income, and is only available to households that itemize deductions. About 30 percent of households do so and tend to be higher-income, but they represent about 80 percent of giving by individuals. (See this review for a history of the charitable contribution deduction.)

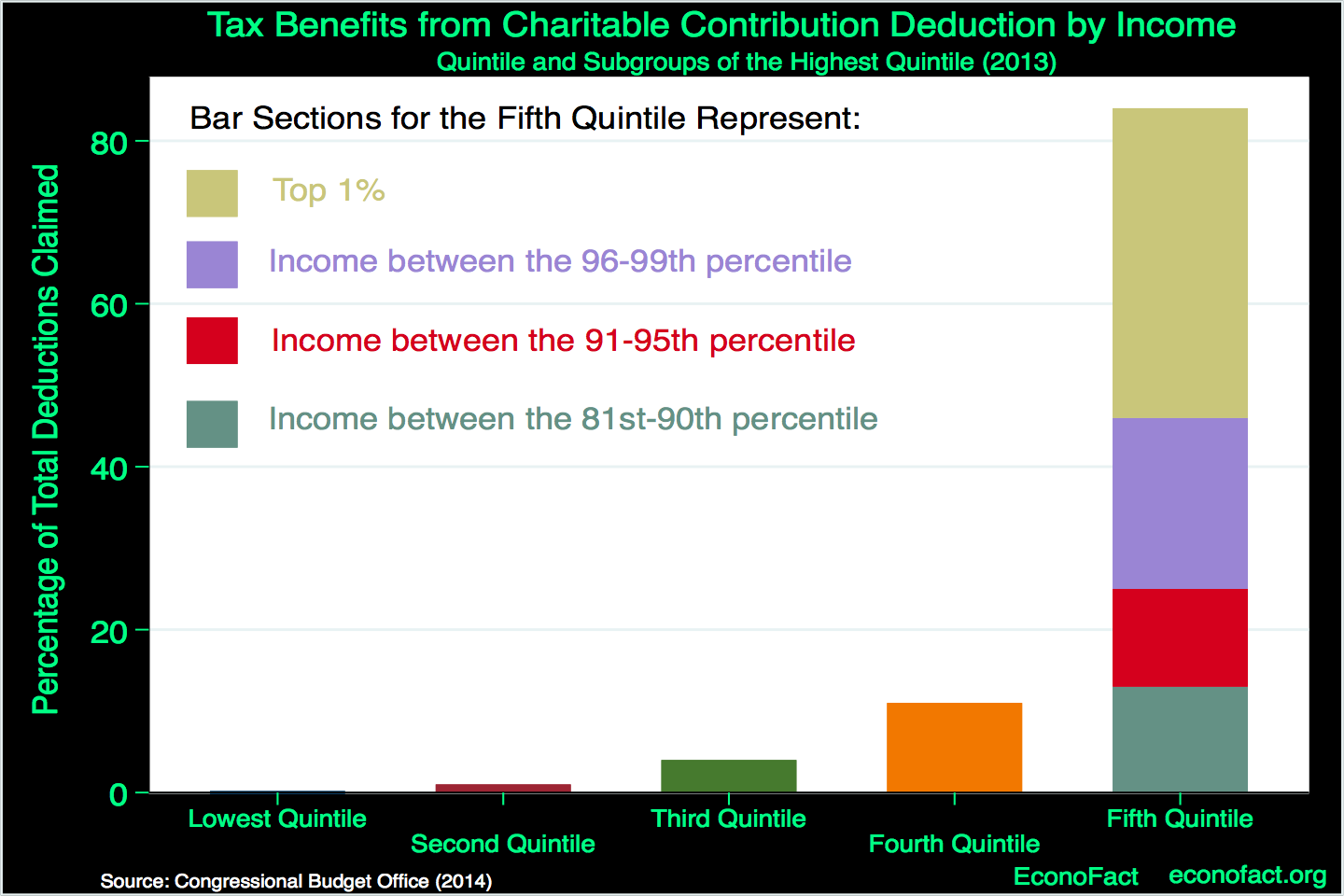

- Higher-income households derive greater tax benefits from the charitable tax deduction. A tax deduction reduces taxable income by the amount deducted; it thus reduces total tax liability by the tax rate times that amount. Given the progressive nature of the tax code, with increasing marginal rates, that means that a deduction is worth more to higher income households. The Congressional Budget Office estimates that over 80 percent of this benefit accrues to households in the top quintile of the income distribution, with over one-third accruing to the top 1 percent of households (see chart). These deductions and credits are called tax expenditures, since they are functionally equivalent to the government raising those funds and then expending them itself. The total tax expenditure of the charitable giving deduction to all qualifying organizations was $54 billion in 2016 .

- Recent tax reform proposals differ in their treatment of the charitable giving. Some have proposed expanding the availability of the deduction to all households, irrespective of whether they itemize. Others cap or even eliminate the deduction. Others still recommend a tax credit rather than a deduction, in which all tax filing units receive the same benefit from making a donation regardless of their tax bracket. A number of states also offer additional state tax incentives for charitable giving. The version of the Trump administration’s tax proposal circulating as of this date would leave the charitable deduction in place. However, the current plan includes a proposal to double the value of the standard deduction, reducing the number of households itemizing their returns (eliminating eligibility for the charitable giving tax deduction). In addition, the administration is proposing reductions to marginal tax rates, which would also reduce the value of tax incentives for charitable donations.

- Does the existence of the deduction for charitable giving benefit society? Valuing the societal benefit created by nonprofit organizations is difficult and often subjective, with some arguing that the largest beneficiaries of the deduction are not the most worthy causes. But the exclusion is more easily justified if the increase in charitable giving it causes is at least as much as the reduction in tax revenues that comes from allowing the deduction. Estimates from the economics literature vary, but suggest that charitable giving is quite responsive to tax incentives and that this is likely to be the case.

What this Means:

Tax policy is extremely complex and any changes involve numerous factors that will affect individuals’ giving patterns and government revenues; overall estimates differ dramatically depending on the specifics of the proposal. As a general rule, though, reductions in tax incentives will reduce donations. Completely eliminating the tax exclusion for charity would reduce charitable giving substantially. Tax revenues would increase, borne mostly by higher-income households, making the tax code more progressive. While high-income households give to all causes, they provide the majority of donations to organizations supporting health, education, and the arts. On the other hand, expanding the deduction to all households would likely increase giving somewhat, though it would primarily be a windfall to households that already make donations. Lower-income households face lower marginal tax rates and thus would not be as responsive to the deduction.