Are Global Imbalances a Source of Concern?

Robert M. La Follette School, University of Wisconsin-Madison

The Issue:

The Trump Administration argues that countries like Germany and China pursue policies that unfairly promote their exports, and consequently experience large trade surpluses at the expense of other countries that run trade deficits, such as the United States. Concern with these global imbalances predates this Administration, and was the subject of international economic policy discussion in the Obama Administration as well. Global imbalances have risen in the wake of the global recession that began in 2008. While their current size remains below those in the middle of the last decade, they remain a source of concern.

When the value of the global imbalance becomes large, or is based on circumstances that are not sustainable, it can entail risks to the global economy.

The Facts:

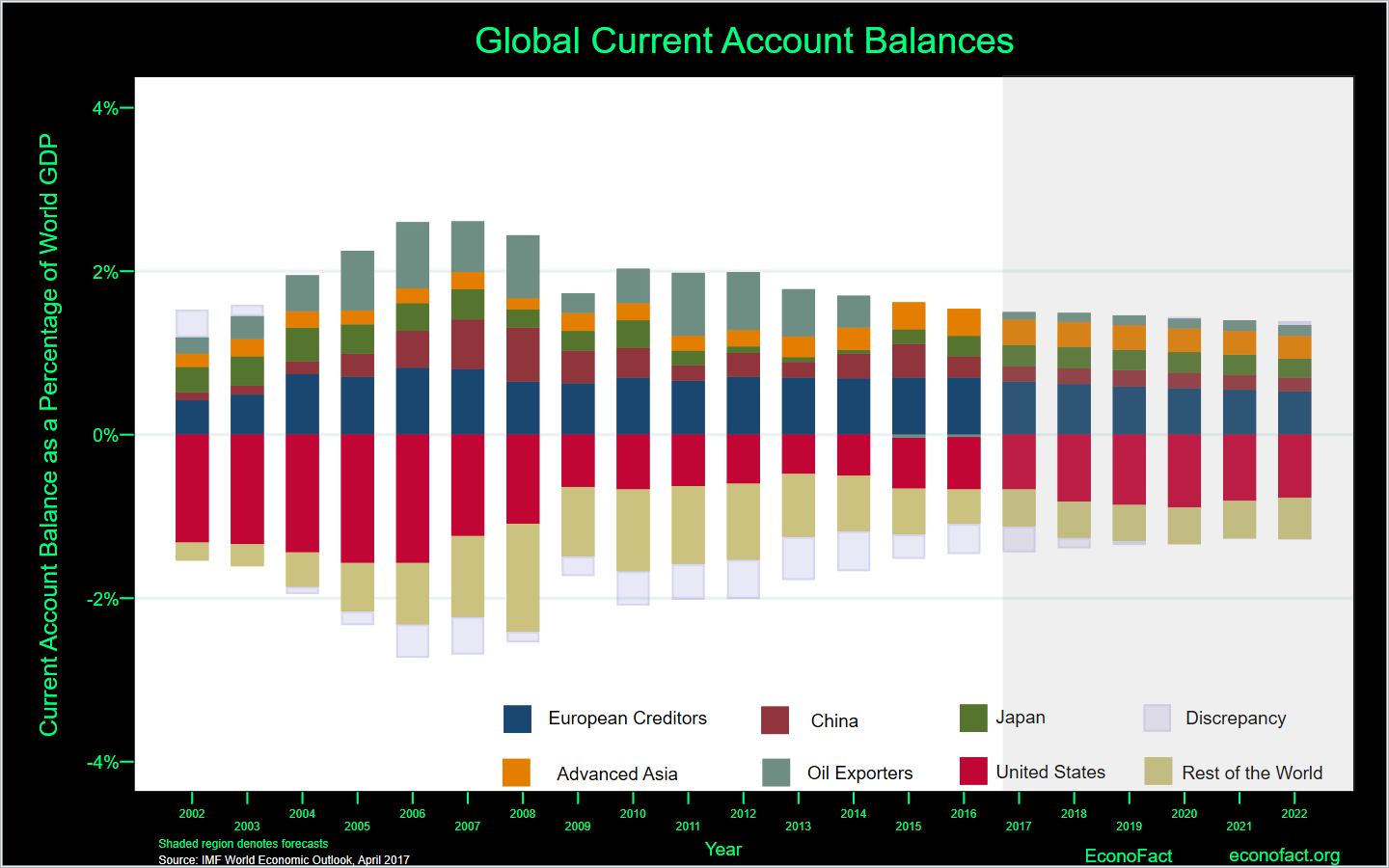

- In the international exchange between countries at any given point some countries are importing more than they are exporting and vice versa. This necessarily implies that, at the same time, some countries will be net borrowers from the international community while others will be net lenders. These external imbalances — both deficits and surpluses — can be appropriate and desirable. But when the value of the global imbalance becomes large, or is based on circumstances that are not sustainable, it can entail risks to the global economy. One way to see the dimensions of global imbalances is to look at the sum of current account deficits and surpluses across countries (see chart). A country's current account is the sum of the trade account (that is, whether it has a trade surplus exporting more than it imports or a trade deficit) plus any net income from abroad due to, say, dividend payments or grants from foreign governments.

- A country's current account reflects economy-wide activity. A current account surplus represents a situation where a country’s income exceeds its spending, while a current account deficit represents spending in excess of income. Equivalently, a country has a current account surplus when its public and private saving exceeds its investment spending, and a deficit when its spending on investment projects is greater than what it can self-finance through its savings. Just as an individual could spend more than she earns by borrowing, so too can a country run a current account deficit by borrowing from abroad. That individual would face a day of reckoning if she persistently borrows to finance her spending and, in so doing, accumulates debt. Likewise, a country with persistent current account deficits may also find itself in a situation where it needs to cut back its spending and face difficult circumstances.

- Many economists have argued that global imbalances that became too large were a contributing factor in the Great Recession and the Global Financial Crisis that accompanied it. Global imbalances grew markedly in the years prior to the Great Recession, reaching almost 3 percent of world GDP in 2006-7 (see chart.) Countries with large current account surpluses in the first decade of this century, like China and Germany, lent to countries like the United States, Spain, and Greece, that had persistent current account deficits, fueling projects like housing (in the United States), government spending (in Greece) and construction (in Spain) that were unsustainable. For instance, in 2005, Ben Bernanke who would subsequently serve as Federal Reserve Chairman stated: “[T]he experience of the United States in recent years is not so nearly unique among industrial countries as one might think initially. [A] number of key industrial countries other than the United States have seen their current accounts move substantially toward deficit since 1996, including France, Italy, Spain, Australia, and the United Kingdom. … [and] have generally experienced substantial housing appreciation and increases in household wealth …" This process ultimately contributed to the financial crisis when some homeowners in the United States, some construction firms in Spain, and the Greek government found themselves too deep in debt. Given this experience, there was general agreement that, in principle, countries should pursue policies that would shrink global imbalances.

- Global imbalances decreased in the immediate wake of the Great Recession but have since rebounded, albeit not to the same extent. The cast of characters in the surplus category has changed somewhat: Oil exporters are no longer running big surpluses given the drop in oil prices. However, European creditors – like Germany – are still running big surpluses and advanced Asia plus Japan and China as a whole has consistently run a surplus, even as the Chinese surplus has shrunk. The United States remains the key deficit country and, although the United States' deficit shrank during the global recession, it has again grown in recent years and is projected to increase further. (See this report for greater detail on global imbalances).

- The current account balance is primarily a macroeconomic phenomenon and, accordingly, policies that adjust macroeconomic conditions are the most effective tools for tackling undesirable global imbalances. A government may have little leverage over some determinants of the current account. For instance, a country with a young population will have less savings, and therefore a larger current account deficit, than a country in which a larger proportion of its population is in their prime earning years, all else equal. But there are policy options over which countries do have control. An important component of national saving is government saving, that is, whether the government has a budget surplus or deficit. Recent estimates indicate that on average, a one percentage point increase in the government budget deficit raises the current account deficit by up to a half of a percentage point. Hence, a projected increase in U.S. government deficits implies a widening of the United States current account deficit.

- The distribution of current account balances is important in the current political context. Persistent current account surpluses from countries such as Germany, China, and Korea in the face of a persistent and increasing current account deficit in the United States contribute to increasing political tensions over trade policies. To the extent that deficit countries could raise production and employment by shifting spending away from exports from surplus countries, policymakers might be tempted to use trade policies to narrow the gap. But, imposing tariffs and other trade restrictions, without addressing other factors such as the balance of government spending, is not likely to have a significant effect on the U.S.'s current account.

What this Means:

Since current account surpluses and deficits are primarily macroeconomic phenomena, driven by saving and investment decisions, attempts to reduce the United States' trade deficit by way of protectionist trade measures, such as anti-dumping tariffs and countervailing duties, and withdrawals from free trade agreements, are unlikely to be effective. Instead, they will redistribute the trade balances between our different trading partners. On the other hand, fiscal policy measures – such as the large tax cuts on the order of $2.2 trillion over ten years currently envisaged by the Trump Administration and the Republican led Congress – are very likely to drastically increase budget deficits and hence current account deficits.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.