Who is Responsible for the Strong Dollar? And What can be Done?

Fletcher School, Tufts University

The Issue:

In a series of recent statements, the new administration has alleged that several U.S. trading partners are making their currencies artificially cheap in order to sell more exports to the U.S. and import fewer American goods. For instance President Trump accused Japan and China of using monetary policy to pursue “devaluation,” during a meeting with leaders of the pharmaceutical industry on January 30. And, Peter Navarro, the head of the new National Trade Council, told the Financial Times that Germany – a country with which the U.S. has a large trade deficit-- uses a “grossly undervalued” euro to its advantage. These statements would seem to indicate that the Trump administration is focusing on making the value of the dollar cheaper with respect to other currencies as part of its stated strategy to increase U.S. exports and reduce the country's trade deficit. But how much power does the President, or any other leader, have over setting the exchange rate?Wishing won’t make it so. Efforts to talk down the dollar in the face of fundamental forces are unlikely to be successful.

The Facts:

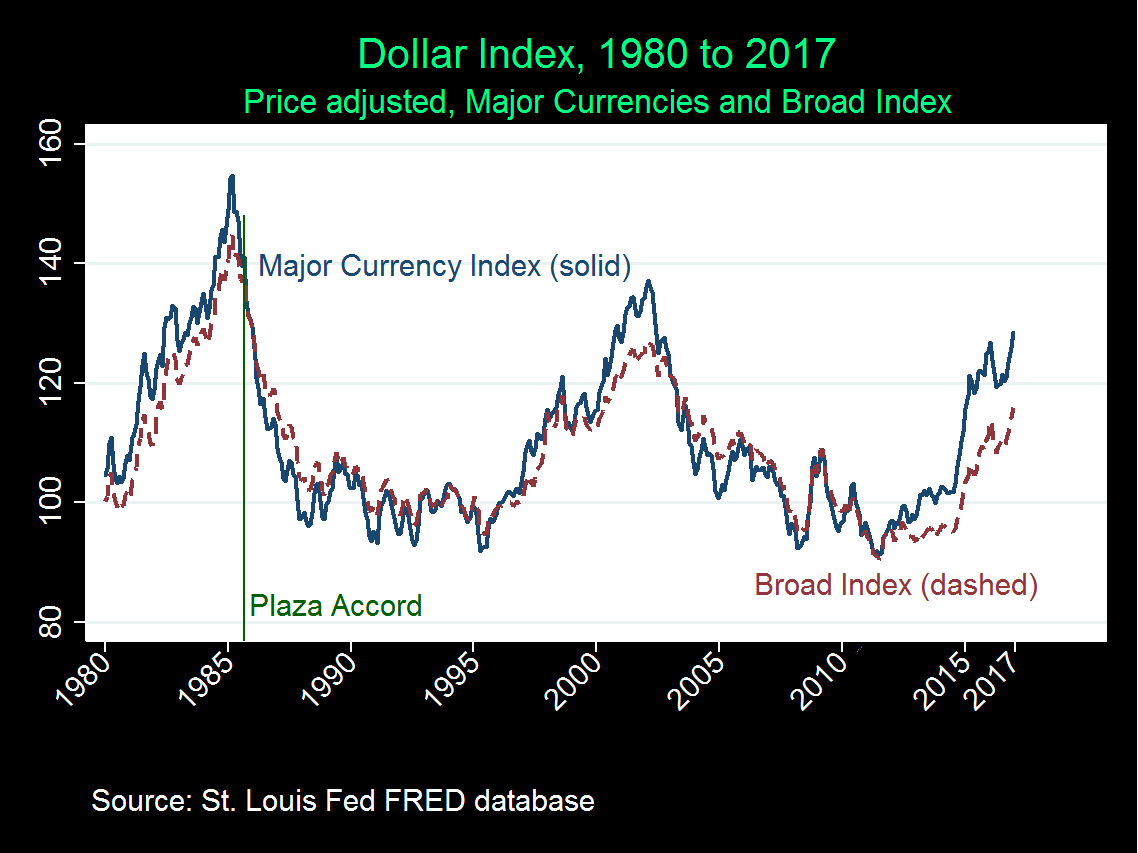

- There is no question that the dollar has strengthened over the past few years with respect to other currencies, including those of China, Japan, and Germany. The dollar has been rising since 2011 and is at its highest value since the summer of 2003 as measured by a broad currency index, and even higher according to a narrower index that just compares the dollar against major currencies (see chart). The relevant indicator for the strength of the dollar adjusts for prices across countries and takes an average based on the amount a country trades with the U.S. While the rise in the value of the dollar is certainly significant, we have seen higher levels of the dollar and more sustained appreciations in the mid-1980s and in the early 2000s.

- There is some confusion about what the U.S. policy towards the value of the dollar should be. The US Treasury has publicly favored a strong dollar through successive administrations since the mid-1990s. Treasury Secretary designate Steven Mnuchin endorsed this view in his confirmation hearings. In this view, a strong dollar is in the interest of the United States because an expectation that the dollar will strengthen, or at least remain stable, supports the sale of U.S. government debt, enabling the government to finance its budget by selling assets internationally. A strong dollar also keeps the prices of imports low, and dampens inflationary pressures.

- On the other hand, a strong dollar means that U.S. exports are more expensive abroad, which hurts companies that produce for international markets and hinders job creation in those sectors (see here for pros and cons of the relative value of the dollar). The recent statements by Trump and Navarro would seem to endorse a weaker dollar.

- But is the strengthening of the dollar a result of other countries' deliberate actions? Exchange rates largely reflect underlying economic conditions. The recent strength of the dollar is a reflection of relatively robust U.S. growth, as compared to the performance of other economies, as well as the stance of its monetary and fiscal policies compared to those of other countries. Government policies that drive up interest rates, like tax cuts, spending increases, or monetary tightening, make dollar assets more attractive, increasing the demand for dollars and strengthening the dollar against other currencies.

- Politicians’ statements (or those by central bankers, or treasury secretaries) may have some short run effect on currency values, but typically not the long-run effect that is necessary for the change in the currency value to have an effect on exports or imports. But politicians’ (and central bankers’) statements do introduce short-run volatility into currency markets. The value of the dollar fell 0.7 percent in response to Navarro's comments to the Financial Times while, correspondingly, the euro rose to an eight-week high.

- There is one well-known example of a successful effort to talk down the dollar, the September 1985 Plaza Accord. The dollar had appreciated by over 50 percent in the first half of the 1980s. This led to international imbalances, with the United States having a deep trade deficit and U.S. manufacturing being hurt by the strong dollar. G-7 finance ministers declared that the dollar should weaken at a meeting at the Plaza Hotel in New York. The dollar continued its depreciation in the wake of that meeting, after a short period of stability in the summer of that year.

- There are reasons to think that results like those after the Plaza Accord would not hold today. First, there is less consensus that the dollar should weaken. This is reflected in the contrasting statements between Trump and Mnuchin. There is also a difference in opinion on the value of currencies between Trump and leaders of other countries since growth is uneven across the world and a weak dollar would hurt export-led growth in struggling economies. Second, the current dollar appreciation is less sustained and much less steep than was the case in the first half of the 1980s.

- Moreover, while the Trump administration is giving signals that it would like to see a weaker dollar internationally, U.S. domestic policies seem, at least in the near future, directed to an even stronger dollar. As unemployment has fallen since the Great Recession, this has made it more plausible that the Federal Reserve would start raising interest rates. And, President Trump's proposals to cut taxes and implement infrastructure spending would also have the effect of increasing domestic demand and strengthening the dollar.

What this Means:

Wishing won’t make it so. Efforts to talk down the dollar in the face of fundamental forces are unlikely to be successful. The recent strength of the dollar reflects the relative strength of the U.S. economy as compared to many of its trading partners, as well as an anticipation that the Federal Reserve may soon begin rounds of raising interest rates (it’s worth noting, also, that a strong dollar will somewhat mitigate the need for the Fed to raise rates). Some of the new administration’s proposed policies, like tax cuts and support for infrastructure spending which are likely to increase domestic demand and lead to higher interest rates, have also put upward pressure on the dollar. Furthermore, at a time when the United States economy is relatively strong, an effort to talk down the dollar will raise international economic tensions by hurting the export performance of countries whose economies are not doing as well as ours.

Topics:

Exchange RatesLike what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.