The Decline in the Dollar

Fletcher School, Tufts University and George Washington University

The Issue:

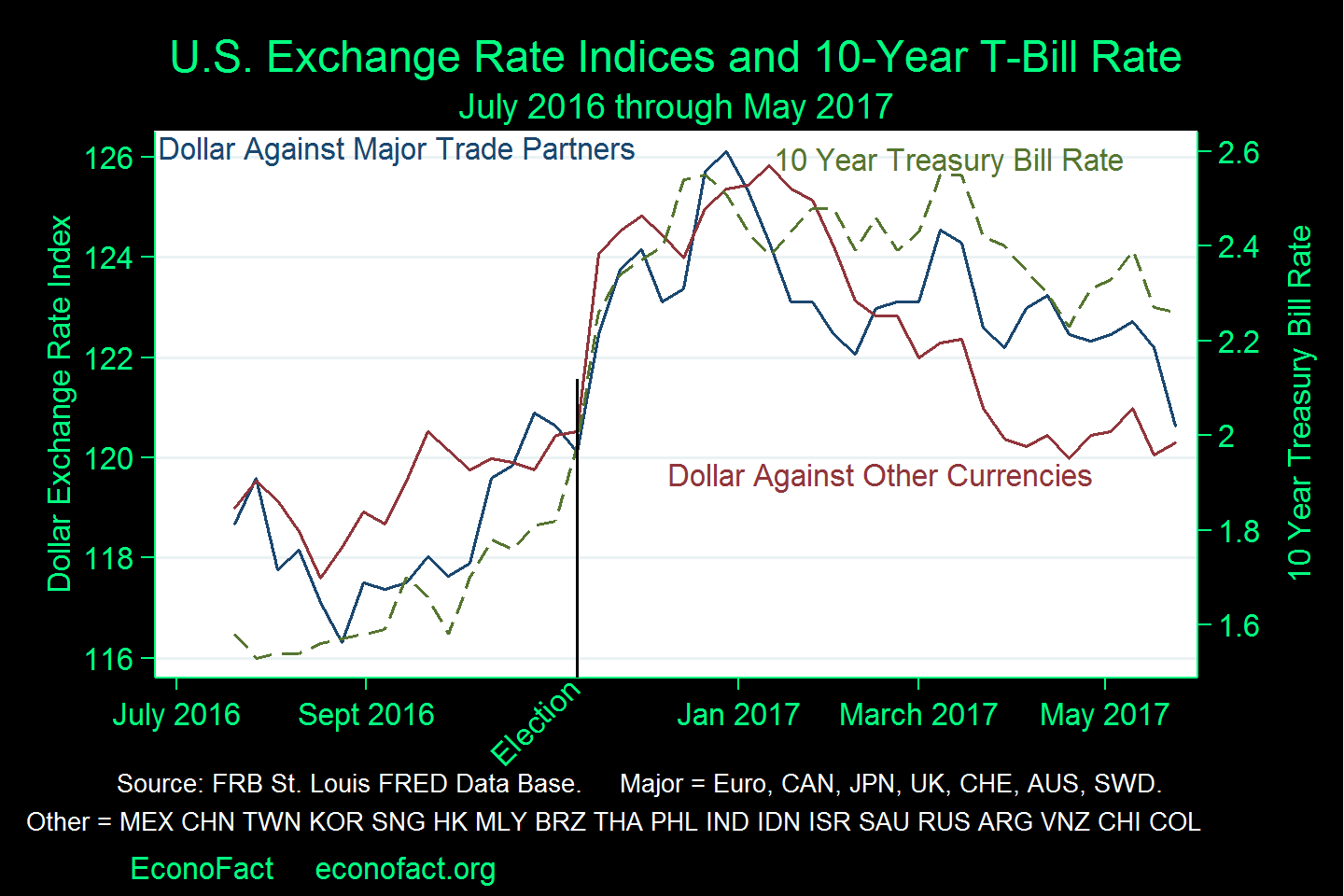

The dollar got stronger (appreciated) against the currencies of its major trading partners in the immediate wake of the election of President Trump. This reflected the market’s view of the expected effects of policies advocated by Candidate Trump, such as tax cuts, infrastructure spending, and higher taxes on foreign goods. But the increasing likelihood that these policies may not be enacted has led to a decline in the value of the dollar as well as movements in other financial indicators, such as a decline in the interest rate on 10-year Treasury Bills.

The dollar is still relatively strong after its huge prior appreciation, but the added rise associated with the election seems to have faded – at least for now.

The Facts:

- The value of the dollar has been on a general upward trajectory for several years. The dollar experienced a particularly steep rise against the currencies of its trading partners in 2014 and 2015, rising 23 percent from mid July 2014 to late January 2016. As commodity prices (especially oil prices) were falling in this period, major oil exporters like Mexico, Canada, and Russia all depreciated sharply against the dollar. But the dollar's strength was broad based: Relatively robust growth in the United States, as compared to the performance of other economies, as well as to the stance of American monetary and fiscal policies as compared to those of other countries was largely responsible for the rise during this period (see this EconoFact post). Following the sharp rise, the dollar’s value against these indices did not change much between February 2016 and the November election.

- In the wake of the presidential election, the dollar strongly appreciated, with the indices of the dollar against both major currencies and the currencies of other trading partners rising by 4 percent between the election and the end of 2016. The interest rate on the 10-year Treasury bill also rose during this period by almost 70 basis points, from 1.82 percent to 2.51 percent (see chart).

- Changes in exchange rate indices and the 10-year Treasury bill rate in the eight weeks after the election reflect expectations of policy changes that were advocated by Candidate Trump. Exchange rates and interest rates are forward-looking variables, that is, their values reflect not just current conditions but expectations of the future as well. Policies advocated by Candidate Trump during the election, such as cutting taxes and increasing spending on infrastructure, would raise interest rates in the United States and, in so doing, would bid up the value of the dollar as foreign investors seek to hold higher-yielding United States assets. Furthermore, Candidate Trump’s calling for trade sanctions against major trading partners would cause the dollar to strengthen as well since currencies typically move to partially offset tariffs. For this reason, the proposed border adjustment tax would also have contributed to a strengthening dollar. The Mexican peso alone depreciated more than 15 percent after the election based on concerns of increased restrictions on Mexican goods.

- The dollar fell over the first six months of 2017 by 4.4 percent against the index of major currencies and by 4 percent against the index of other currencies. These shifts likely reflect changing market perceptions of the likelihood of the administration succeeding in getting tax cuts or an infrastructure spending bill through Congress or of a border tax adjustment being included in a tax reform. The Mexican peso too has actually recovered all of its lost value since November 8th. It is noteworthy that these decreases in currency values occurred while there was continued discussion of the Federal Reserve raising interest rates, as unemployment and the inflation rate stayed low. That is, the core fundamentals have changed little. The 10-year Treasury bill rate also declined, but not by as big a proportion as the decrease in exchange rates. The smaller change in the 10-year interest rate as compared to the exchange rate indices may reflect the effect of an expected increase in the Federal Reserve’s policy rate (the Federal Funds rate) being countered by the decreasing likelihood of the enactment of tax and spending policies that would raise the government’s budget deficit. Changes in views on trade policy or a border adjustment tax would weigh specifically on the exchange rate, as might changes in expectations of foreign growth or policy.

What this Means:

Currency values respond to news, literally new views on the future, so a lower likelihood of the enactment of policies that would stifle trade or raise the government budget deficit would change perceptions and alter currency values. This is what we seem to be witnessing now, with a decreasing likelihood of major economic policy changes. The dollar is still relatively strong after its huge prior appreciation, but the added appreciation associated with the election seems to have faded – at least for now.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.