The Financial and Economic Crisis in Turkey

University of Maryland

The Issue:

The Turkish lira has lost more than 40 percent of its value against the dollar since the beginning of the year, the country's debt has been downgraded by Moody’s and Standard & Poor’s, and experts are predicting a recession in 2019. President Recep Tayyip Erdogan has blamed the crisis on western countries, and the United States in particular, since the crisis began after President Trump doubled tariffs on Turkish metal exports to put pressure on the government to release a jailed American clergyman. But, like many other crises in emerging markets, even if the match that ignited this economic conflagration was the tariff increase, the combustible conditions were homemade and the result of an unsustainable credit boom and overborrowing.

Even if the match that ignited this economic conflagration was the tariff increase by the United States, the combustible conditions were homemade.

The Facts:

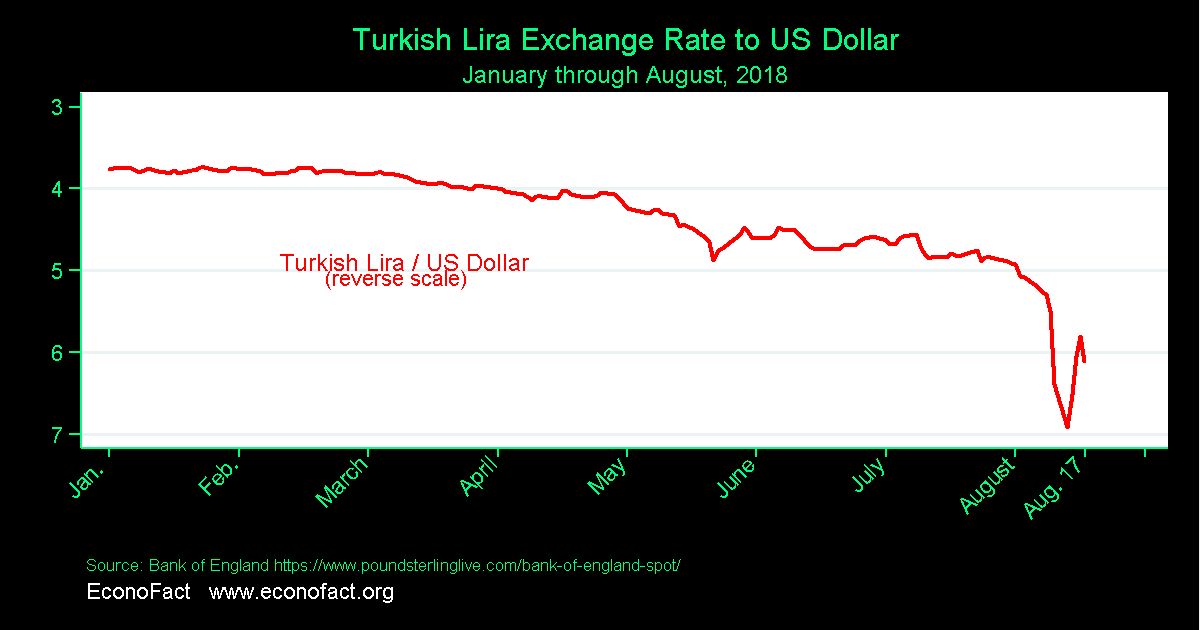

- Turkey had a large credit boom over the last decade financed with capital inflows from abroad. The private sector in particular — both corporations and banks — borrowed from foreign investors. About 60 percent of the corporate sector debt was in foreign currency in 2013 (see here). Having foreign currency-denominated borrowing is particularly risky for sectors such as construction whose earnings are in Turkish liras. (About 70 percent of the construction sector's debt is in foreign currency and for manufacturing it is 50 percent). If the Turkish lira loses value with respect to foreign currencies, the debt held by these companies becomes more difficult to repay and foreign investors become nervous about investing in the Turkish private sector. While the credit boom was taking place, the Turkish government kept monetary policy loose, allowing the economy to grow steadily but also failing to keep inflation in check. With annual inflation at 16 percent, the Turkish lira has been losing value with respect to foreign currencies and raising investor concerns. Indeed, the lira began 2018 at about 3.8 per dollar, by April it had depreciated to 4 lira to the dollar, and it began to plummet in value in August (see chart).

- Emerging market countries like Turkey can benefit from borrowing from abroad, and investors in richer countries benefit from lending to these countries. Economic growth depends upon a number of factors, including an expansion of factories, infrastructure and capital equipment. Emerging market countries typically cannot self-finance the amount of investment needed for rapid growth, and therefore borrow from abroad. Foreign investors are often happy to provide funding because of the high growth prospects of these emerging market countries. This is especially true during periods when, like in the wake of the 2008 Global Financial Crisis, richer countries like the United States had very low interest rates and their growth prospects seemed limited, so investing in less developed countries became more attractive.

- While there are clear advantages to emerging market borrowing, countries often experience a boom – bust cycle after extensive borrowing from abroad. There is a long history of boom-bust cycles and subsequent crises in emerging market countries. Across the years, investors and borrowers alike have thought “this time is different” and conditions were distinct from the last set of crises. For example, many people believed that emerging market countries learned their lessons from the financial crises of 1980s and 1990s that were ignited by high levels of sovereign debt, inflexible exchange rates, and large fiscal deficits. Indeed, emerging market macroeconomic policy has generally been better since the turn of the century. But the current crisis in Turkey shows that countries can have a crisis even with flexible exchange rates and low government debt if the private sector borrows heavily in foreign currencies and loose monetary policy causes inflation to rise and the domestic currency to fall in value.

- Currency mismatches arise when emerging market governments or companies borrow in dollars rather than in the domestic currency, and these mismatches often play an important role in crises. Emerging market governments and companies in emerging markets often find it easier to borrow through contracts denominated in U.S. dollars rather than their domestic currency because lenders are insulated from being repaid in foreign currency that might lose value. Lenders might also prefer short-term debt. Emerging market borrowers are rewarded with lower interest rates in these circumstances. But they are more vulnerable to exchange rate depreciations when their receipts are in domestic currency while their loan repayments are in dollars. They also face a crisis if they cannot roll over their debt. During the Latin American crises of the 1980s, and the Asian crises of the 1990s, this type of liability dollarization played a significant role (see here).

- A key macroeconomic vulnerability in Turkey is private-sector short-term borrowing in U.S. dollars. Some companies try to protect themselves from falls in the value of the lira through currency hedging (essentially, buying an insurance contract to protect against this outcome). But, in general, only big companies can afford to do this because hedging is very costly. The vulnerability of Turkish companies makes lenders less willing to roll over their debt. Also, the rise in interest rates in the United States and Europe with improving growth in these economies, as well as the prospect for even higher interest rates as the Federal Reserve and the European Central Bank shift their attention to cooling potentially overheating economies, have made emerging market debt relatively less attractive than it had been when interest rates were rock bottom in richer countries.

- A standard first response to this type of crisis is that the central bank raises interest rates, but this has not happened in Turkey. Central banks can attempt to stem the outflow of money and keep the currency from plummeting by raising interest rates and making domestic debt more attractive. This also has the advantage of demonstrating the independence of the central bank, which gives investors confidence that the currency will not continue to fall. But higher interest rates also raise the cost of borrowing to firms and slow the economy. Monetary policy is currently quite expansionary in Turkey, as shown by an inflation rate of 16 percent. Foreign investors may have reason to believe that the Central Bank of Turkey will not raise rates, or only do so by a token amount: After the election in late June, 2018, President Erdogan, who has called interest rates “…the mother and father of all evil", gave himself sole authority to appoint the head of the Central Bank.

- There is a political dimension to this crisis as well. President Erdogan came to power in 2003 as the prime minister with the AKP government. Since that time, Turkey has enjoyed resilient growth that averaged 5 percent annually, a performance that earned praise from financial markets and economists alike (see here). However, during this period of populist policies and the rule of a leader who centralized power around himself, there were no major structural, institutional or legal reforms that would have addressed underlying weaknesses in the economy but may have slowed growth in the short run and imperiled the popularity of the government. Loose monetary policy can support economic growth (and the popularity of the government), at least for a while, but it can also ultimately lead to an asset price bubble, especially in the absence of any domestic structural reform. In the case of Turkey, an additional factor was the erosion of the strength of institutions during Erdogan’s rule that could have provided more economic stability by limiting economic mismanagement and financial and economic fragility (see here).

- The United States Administration did not cause this crisis, but it did not help, either. The normal response of the United States during an emerging market crisis is to try to calm markets. President Trump, by slapping tariffs on Turkish metals, did exactly the opposite. The chart shows that the lira was already tumbling before President Trump announced a doubling of tariffs, and the fall continued in wake of his comments. Along with the direct detrimental effects of the rise in tariffs, President Trump’s move also helped President Erdogan blame America for the crisis, arguing that the U.S. was waging an economic war against Turkey. Placing the blame on a foreign government makes it less likely that the Turkish government will look to address domestic factors leading to the crisis.

What this Means:

The Turkish crisis is a home-made textbook example of an emerging market crisis. It did not come about because of the United States, but it has been made worse by the political fight between Presidents Erdogan and Trump. Political pressure in Turkey might mean that the central bank finds it difficult to take measures to stem the collapse of the lira, a precondition to the resolution of the crisis. But, at this point, raising interest rates might not be enough if confidence in the Turkish economy cannot be regained. The crisis could spread to other potentially vulnerable emerging markets, those that are borrowing heavily from abroad, especially if the borrowing is in foreign currency and inflation is high (which is an indicator that the domestic currency will likely weaken). There is the possibility that the Turkish economic crisis has an impact on Europe as well, since many European banks have lent to Turkish banks and companies. The pivotal role that Turkey has played in the refugee crisis introduces another set of concerns, since Europe cannot afford to have an unstable Turkey in its backyard. The United States, while more insulated from the economic fallout of a Turkish crisis, will face political pressures if the crisis brings Turkey closer to Russia and introduces a new source of economic and political tension in a volatile region.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.