The Capital Gains Tax and Inflation

Brandeis University

The Issue:

The United States Treasury Department is reportedly studying whether it can issue regulations that would allow taxpayers to account for inflation when calculating taxes on capital gains. Such a change has been considered in the past. Taxing savings, like taxing any economic activity, distorts the functioning of the economy. The fact that we currently tax the part of nominal investment returns that have merely served to compensate holders for the impact of inflation seems to many like a problem for which reform could be appropriate. But, adjusting capital gains taxes to account for inflation can introduce its own set of distortions and reduce government revenue in a time of increasing deficits.Adjusting capital gains taxes to account for inflation can introduce its own set of distortions and reduce government revenue in a time of increasing deficits.

The Facts:

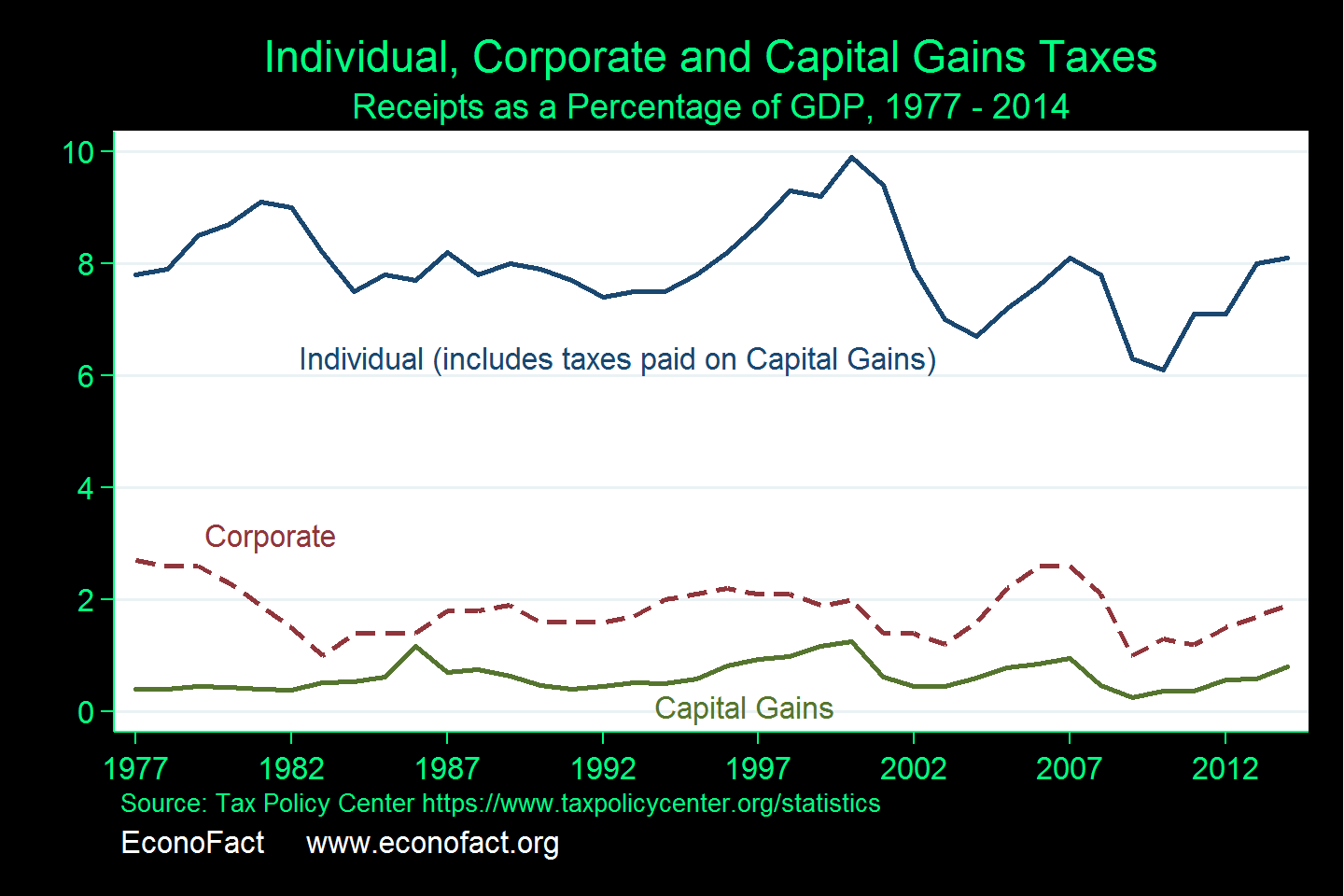

- Taxes on capital gains are an important – and at times highly variable – source of revenue for the federal government (see chart). A capital gain (or loss) occurs when an asset – real estate, a security, a cryptocurrency, or any other asset – that was purchased for one price is later sold for a different price. Under current tax law, taxes on capital gains are paid once, only in the year that an asset is sold, rather than on an ongoing basis with taxes calculated each year based on gains or losses over that period. The tax rate on capital gains depend on a number of factors, for example the length of time that an asset has been held, or whether the asset is held inside or outside a tax-advantaged savings account such as an IRA.

- Proposals to account for inflation when calculating capital gains taxes reflect an effort to tax the increase in the real purchasing power of an asset rather than the increase in its value that only reflects overall rising prices. For example, consider an asset that was purchased for $1,000 in 2000 and sold for $1,500 in 2018. Average annual inflation over this period was 2.25 percent, so something that cost $1,000 in 2000, and whose price followed inflation, would cost $1,500 in 2018. This means that the inflation-adjusted return on this asset was zero. Even though the owner sold the asset for more than what they paid for it, they did not experience a real increase in wealth. But the capital gains tax would be based on the $500 increase in the price of the asset. The tax-inclusive real (i.e. inflation adjusted) return on this asset would then be negative; if the capital gains tax was 25 percent, the tax would be $125 and the real return on the asset would be -8.7 percent. If, however, the capital gain was adjusted for inflation, the tax would be zero.

- The idea of adjusting capital gains for inflation has a long history. Concerns about taxing nominal capital gains became particularly acute during the high-inflation 1970s when the average inflation rate was over 7 percent. Indexation proposals were floated during the tax reforms of 1978 and 1986, but were not included in the final version of either final reform. The Trump administration is reportedly exploring the idea of changing the taxation of capital gains via a new Treasury regulation, as opposed to working through Congress. This has also been considered in the past. The idea of indexing capital gains taxes by executive order was explored during the George H. W. Bush administration, but it was abandoned after both the General Counsel of the Treasury Department and the Office of Legal Counsel of the Justice department rejected this idea as illegal (see here).

- A potential benefit from indexing capital gains would be enhanced incentives for savings and investment. The fact that inflation is not taken into account when capital gains are taxed increases the effective tax rate on savings. A lower effective tax rate (accomplished by adjusted capital gains for inflation) would increase the real return to saving and investing, and may contribute to higher levels of capital formation, and thus higher wages, and employment. But these incentives would depend upon the change being credibly believed to be persistent, something that might be in doubt in a time of rising deficits. Furthermore, the immediate impact of the change would be a significant windfall for households who saved in the past – a windfall that would not affect their future behavior, given that their past saving has already happened. If one thinks of tax policy as a balance between raising funds and reducing distortions to saving and other behavior, the first order impact of the change would be a deeply regressive increase in deficits and a windfall for households whose relevant behavior has already occurred and for which concerns about distortions are therefore irrelevant.

- There are several considerations that work against adjusting capital gains taxes for inflation. Any type of inflation indexation would lower tax revenue at a time of rapidly increasing budget deficits. Len Burman of the Tax Policy Center has estimated that the impact on budget deficits of indexing capital gains taxes for inflation would be in the neighborhood of $10 - $20 billion per year – perhaps small relative to a $1 trillion overall deficit, but going the wrong direction. And indexing capital gains would push against the goal of progressivity in the tax code – because capital gains taxes are paid overwhelmingly by high-income households, this tax change would overwhelmingly benefit those families.

- Other tax payments are also affected by inflation – for example, “bracket creep” means that rising incomes due to inflation move people into a range with a higher tax rate. There is no compelling reason to index capital gains but not other forms of income. Moreover, adjusting the capital gains part of the tax code for the impact of inflation without addressing real/nominal discrepancies elsewhere will open up new tax shelters for people and businesses with the resources to access them. One example: an investor who borrows to buy assets will be able to write off the nominal value of interest paid to purchase the assets while being taxed only on the after-tax return to those assets, a tax “loophole” that is almost certain to encourage exploitation.

What this Means:

Tax policy reflects a tradeoff between raising revenue and distorting the functioning of the economy; the goal is to raise the required revenue in a way such that the damage done by economic distortions created by taxes is as low as possible. The goal of minimizing tax distortions on savings is a legitimate one, and the tax code already includes a number of ways in which capital gains enjoy preferential treatment. The ability to defer capital gains until an asset is sold is an important benefit, and tax rates on capital gains for assets held more than a year are generally lower than tax rates on other sources of income. In addition, assets that are passed to heirs through an estate enjoy a benefit known as the “basis step up”, meaning that the basis for calculating capital gains taxes is “stepped up” to the current value when the assets are bequeathed. Indexing capital gains taxes for inflation by regulatory fiat – if it were actually determined to be legal – would have significant costs and questionable additional benefits.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.