Medicaid and CHIP: Filling in the Gap of Children’s Health Insurance Coverage

Williams College

The Issue:

Together, Medicaid and the Children's Health Insurance Program (CHIP) have become an integral source of health insurance for children in the United States, providing coverage for more than one in three children in 2016. From its creation in 1965, Medicaid provided health care coverage for children from the poorest families. But a substantial share of children remained uninsured: those whose families earned above incomes needed to qualify for Medicaid but lacked employer-sponsored coverage and those for whom private insurance remained unaffordable. While subsequent Medicaid expansions addressed this issue to some extent, a substantial gap remained. The Children’s Health Insurance Program (CHIP), which began in 1997, filled in the gap for families at these income levels. While there is bipartisan support for CHIP, the funding for the program must be renewed by Congress periodically for states to continue its provision, raising uncertainty.

CHIP aimed to fill in the gap of coverage for children from low-income families who are above the income threshold to be eligible for Medicaid.

The Facts:

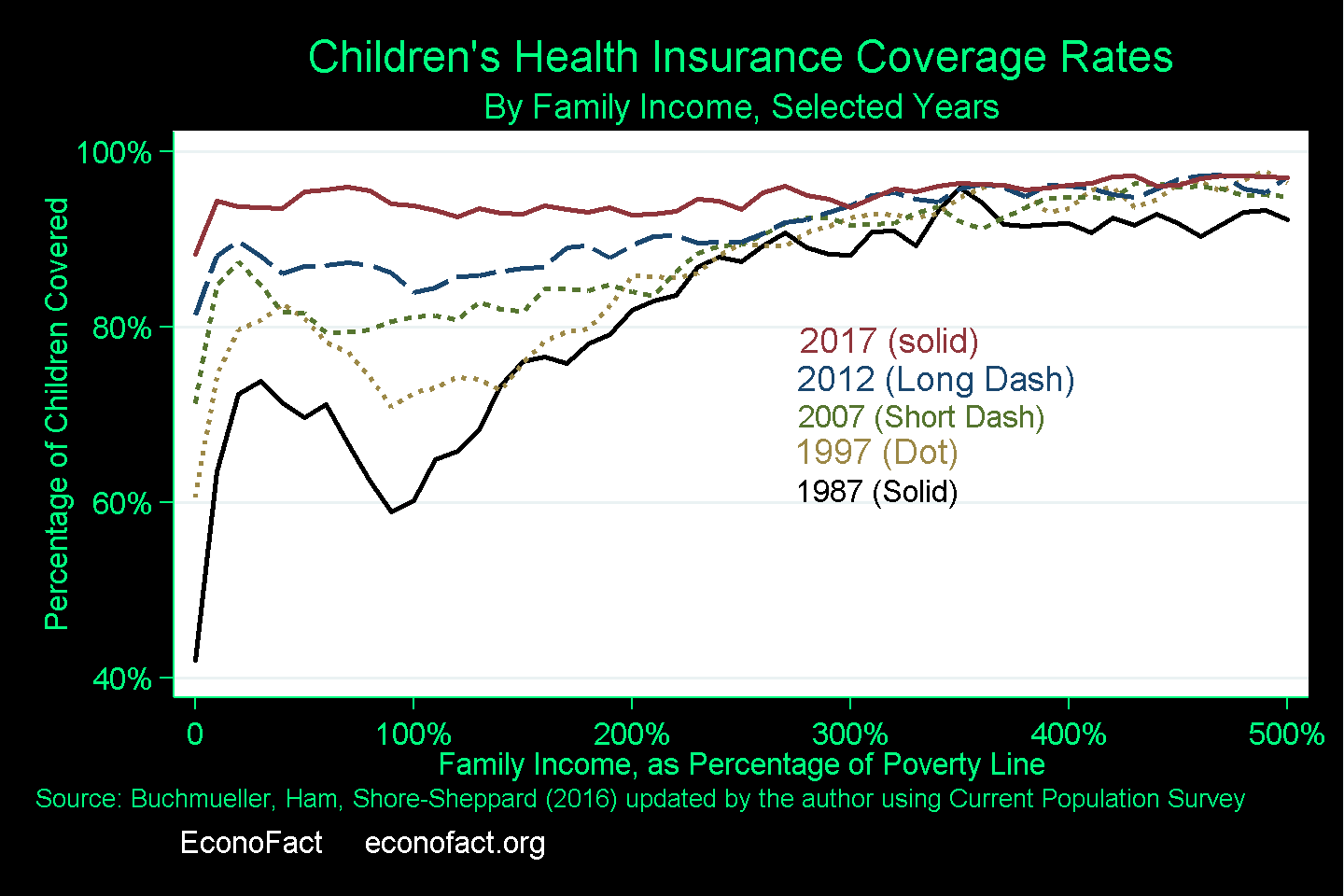

- There was a clear improvement in children's health insurance coverage rates between 1997, when CHIP was authorized, and 2012 (prior to the full implementation of the Affordable Care Act). Since Medicaid initially only covered children from the very poorest families, coverage rates across the income distribution had a “U” shape: the poorest children were eligible for Medicaid, and children in high-income families received coverage through a parent’s employer-sponsored coverage, while children in families with incomes between 50 and 200 percent of the poverty line had a considerably higher probability of being uninsured. Recognizing that private insurance was unavailable or unaffordable to many families in this group, the federal government expanded Medicaid eligibility, which began to fill in the “U” but, even so, a significant gap in coverage remained in 1997 when CHIP was authorized. As CHIP targeted children with family incomes somewhat higher than the poverty line, the clear improvement in coverage rates between 1997 and 2012 provides support for the argument that CHIP, along with expansions of Medicaid, increased the health insurance rates among children (see chart). By 2016, 37.5 percent of children in the United States had their health insurance coverage through Medicaid or CHIP (see Exhibit 2). While it is difficult to disentangle the individual contributions that each program made, additional research using quasi-experimental methods finds evidence that the rising health insurance coverage of children in families with incomes somewhat higher than the poverty line is likely due to both CHIP and the expansion of Medicaid. (Several studies examine the causal impact of these programs on increased coverage and whether their expansion crowded out private insurance: see here, here, here, here, here, and here. My co-authors and I survey this area of research in the Medicaid chapter of this book).

- The Children’s Health Insurance Program (CHIP) was an effort to fill in the gap of coverage for children from low-income families who are above the income threshold that would make them eligible for Medicaid. CHIP began as the State Children’s Health Insurance Program, which was authorized by the Balanced Budget Act of 1997 for 10-year period. States were given block-grant funding, with the amount based on the number of uninsured children in the state and the state’s relative health care costs, to allow them to expand public health insurance to additional children not covered by Medicaid. As is the case with Medicaid, state spending was matched by the federal government, at a rate somewhat higher than the Medicaid match rate but capped at the state’s allotment. CHIP allowed states to equalize eligibility across ages, and also to offer coverage to children at higher income levels — in most cases to children in families with incomes between two and three times the poverty line.

- Because states have some degree of discretion in how they implement both Medicaid and CHIP, there is variation in how the programs work together from one state to another. Children are eligible for Medicaid if their family’s income is below the state-determined income limit. States have some discretion on how low family income must be for a child to be eligible for Medicaid (typical levels are between 133 percent and 200 percent of the federal poverty line, though some states set their limits higher) but once a state has set the limit any child with family income below the limit is eligible for services paid by the state with a federal government match of spending. Beginning in the 1980s, the federal government expanded Medicaid eligibility, first by permitting and then by requiring states to cover additional low-income children whose families were not eligible for cash assistance. These expansions typically covered infants and very young children earlier and at higher income limits, but by the time of the initial passage of CHIP in 1997 all but the oldest teenagers (15-18) were covered if their family income was below the federal poverty line (and sometimes higher, depending on the state). The structure of CHIP was intended to fill in this gap, with the result that particularly in some states children may age from Medicaid to CHIP even if their family income does not change. In addition, as a family’s income changes its children may move from Medicaid eligibility to CHIP eligibility or vice-versa. Families may not be entirely aware of the exact source of funding for their children's coverage.

- Unlike Medicaid, which is an entitlement, funding for CHIP needs to be renewed by Congress periodically. CHIP was reauthorized after its first decade, but not without some controversy. When CHIP came up for renewal in 2007, Congress passed two bills reauthorizing it. But President Bush vetoed both, voicing concern about potential negative impacts on privately sponsored health insurance coverage. The studies that examined impacts of CHIP and Medicaid expansions on coverage have also measured crowd-out, typically finding estimates of private coverage decline in response to public coverage eligibility that are small. In late 2007 the Medicare, Medicaid and SCHIP Extension Act of 2007 was enacted, largely maintaining existing funding levels for the program on a short-term basis. Full reauthorization of the program occurred in 2009 with the Children's Health Insurance Program Reauthorization Act (CHIPRA).

- The availability of Medicaid and CHIP coverage for children has led to improvements in access to health care and to improvements in health over both the short-run and the long-run. Research using quasi-experimental methods has found that children who become eligible for public insurance through expansions in Medicaid or CHIP are more likely to see a doctor at least once a year, are more likely to be in better health as teenagers and as adults if they were eligible for public insurance as young children (see, for example here, and here), and have lower mortality as teens and adults (see, for example here, and here).

- CHIP continues to play an important role for health care coverage for children from poorer families, even after the full implementation of the Affordable Care Act (ACA, or Obamacare) in 2014. As other researchers have pointed out, Marketplace coverage is in many cases not an adequate substitute for CHIP coverage for children. While coverage through the ACA Marketplaces is subsidized for low-income families, the subsidy is only available if the family does not have access to affordable employer-sponsored insurance. Since the affordability standard is based on the cost of employee-only coverage relative to the family’s income, families offered affordable employee-only coverage are not eligible for a subsidy for family coverage through the Marketplaces, even if family coverage through the employer has much higher cost. Moreover, in many cases, the benefits available through a Marketplace plan are less complete than the benefits offered through CHIP, particularly in areas such as dental, vision, and hearing care.

What this Means:

CHIP is a key provider of health insurance for low-income children and has been an important contributor to the achievement of near-universal health insurance coverage for children in the United States. There has been a clear improvement in child well-being as result of Medicaid and CHIP. However, the renewable block-grant nature of CHIP funding leads to periods of uncertainty for families and states when the program comes due for renewal, threatening the health insurance coverage of large numbers of children. The threat of coverage losses for children arising from failure to address the program’s funding suggests that if recent policy proposals to make Medicaid a block-grant program were to be implemented, this could introduce additional periods of uncertainty and instability for children’s health care coverage.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.