Social Security Benefits: When Do You Plan to Retire?

University of California, Berkeley

The Issue:

Social Security provides retirement benefits to over 40 million people each year. Current projections indicate that the program faces a long-term financing shortfall, and many Americans wonder whether the program will survive to pay them the benefits they have earned. President Trump pledged repeatedly during his campaign not to cut Social Security. But his nominee for White House budget director, Representative Mick Mulvaney, suggested during his confirmation hearing that he plans to advise the president to cut Social Security by increasing the retirement age.

Millions of retirees depend on Social Security. Raising the income level at which contributions are capped could maintain the program's long-run viability without cutting benefits.

The Facts:

- Social Security provides retirement benefits to over 40 million people each year, as well as to millions more spouses, dependents, and survivors of deceased workers, according to the Social Security Administration. Benefits average under $1,350 per month, and 30 percent of retirees receive less than $1,000 per month. These benefits are financed by payroll taxes paid by nearly all American workers. The program operates on a pay-as-you-go basis: Taxes paid by workers each year are not set aside for those workers’ future retirements, but are used in the same year to pay benefits to current retirees. Taxes and benefits do not balance perfectly each year, and the program has at various times operated in surplus or in deficit.

- Social Security benefits provide more than half of the household’s income for nearly half of married retirees and nearly three-quarters of unmarried retirees. Over one-fifth of married retirees and nearly half of unmarried retirees rely on the program for fully 90 percent of their income. This is because few Americans have substantial retirement savings outside of Social Security. In 2010, only 22 percent of full-time, private-sector employees had a defined-benefit retirement plan (i.e., a pension), and those plans that remain — both public and private — face significant financing challenges. Outside of traditional pensions, less than 60 percent of near-retirement-age households have any retirement savings, and among those who have savings the median balance is only $91,000. If used to purchase an annuity, this would support less than $5,000 per year in retirement income. This is in part because relatively few households have the financial wherewithal to save meaningful amounts for retirement, as they need nearly all of their earnings to support basic current needs.

- Elderly poverty is dramatically reduced by Social Security. Under the Census Bureau’s supplemental poverty measure, which counts income from transfer programs toward family resources but also attempts to account for medical costs, 14 percent of seniors live in poverty. Without Social Security benefits, this would rise to nearly 50 percent.

- Social Security faces a long-run funding shortfall. Projected revenues over the next 75 years fall short of projected benefits under current program rules by 2.66 percent of taxable payroll. This deficit reflects a number of factors, including lengthening lifespans, reduced birthrates and lower immigration. Rising wage inequality also leads to benefits rising more quickly than revenues because benefits are proportionally higher relative to income for lower-income retirees while social security contributions are capped and do not increase for annual incomes greater than $118,500.

- But the long-run funding shortfall does not threaten the basic structure of the program. A 16 percent cut in benefits, with no other changes, would close the entire 75-year funding gap. Alternatively, benefit cuts can be avoided via relatively small increases in revenues. For example, suppose that the existing tax rate were applied to all earnings, without excluding those above $118,500 per year as at present. This would expand the tax base by about 25 percent and raise enough revenue to entirely close the 75-year deficit, without benefit cuts for anyone and with only modest tax increases for any but the very highest earners.

- The benefits that Social Security provides are not easily obtainable through the private sector, even for those who manage to save. Social Security shields retirees from bad asset market outcomes and unscrupulous or incompetent investment advisors. Social Security benefits are not tied to the continued viability of any single employer, and while occasional adjustments are needed as demographic and economic realities diverge from earlier projections, these are small relative to the volatility faced by pension funds or private savings. Moreover, Social Security benefits are provided over an entire lifetime and cannot run out. To achieve that with private savings it is necessary to purchase annuities, which are very expensive.

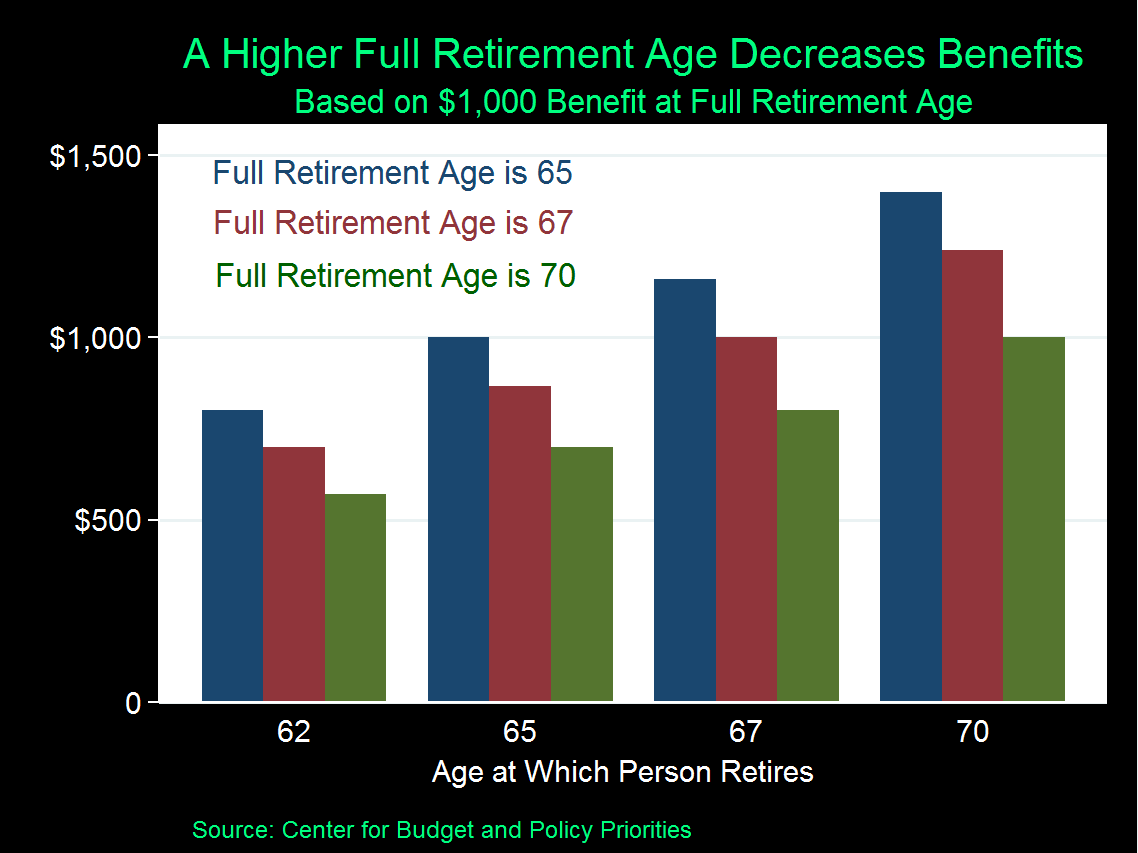

- Raising the retirement age for receipt of full Social Security benefits (known as the “full retirement age”) is exactly the same as cutting benefits. Retirees receive higher benefits if they postpone retirement. But a retiree who stops working at a given age receives lower benefits if the full retirement age is raised. For example, suppose the full retirement age is 65, and that a retiree would receive $1,000 per month if he retired at that age. If the retirement age is raised to 67, that person would receive only $867 if he retired at 65, and would have to wait until 67 to receive the original $1,000 per month. The benefit if he retires at 65 would fall further, to $700 per month, if the full retirement age were raised to 70 (See chart). Regardless of the planned retirement age, benefits are lowered if the full retirement age is increased. It is important to note that relatively few workers wait until even the current full retirement age to begin drawing benefits. In 2013, according to a Congressional Research Service report, 45 percent of new claims were from 62-year-olds, and nearly 60 percent were under 65, and all of these people retired before their respective full retirement ages.

What this Means:

Large majorities oppose cuts to Social Security. In a recent poll conducted for the National Academy of Social Insurance, 82 percent agree it is critical to preserve Social Security for future generations even if this means increasing Social Security taxes paid by working Americans. And, 75 percent believe we should consider raising future Social Security benefits in order to provide a more secure retirement for working Americans. This is understandable when one considers that there are declining rates of coverage by other retirement plans such as private defined benefit pensions, and the typical retiree has limited savings in defined contribution accounts. The long-run viability of Social Security could be maintained by cutting benefits through raising the retirement age. But there are many other options as well, including increasing revenues by raising the income level at which Social Security contributions are capped. Any type of benefit cut would further erode the already limited retirement security that working Americans have. Policy changes that strengthen the retirement system have tremendous promise to improve people’s feelings of security – not just retirees but also people in the prime of their lives. Social Security is the best functioning component of this system, and should be the basis for efforts to expand retirement security. Its financing shortfall can be addressed without changes to the structure of the program, and we can and should look to expand rather than reduce benefits to replace disappearing pensions and individual savings.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.