Many American Households Are Still Struggling to Build Wealth

Harvard University

The Issue:

Although trends in income bear heavily on economic security at the household level, they are not the whole story. One also needs to look at patterns of wealth holding to fully assess the economic risks facing households. The latest data on wealth show broad-based positive gains for American households over the last few years. But, they also highlight the growing concentration of wealth at the top, and the difficulties many families face when it comes to saving and building wealth.American households have recently made broad-based gains in wealth, but many have not made up for the losses suffered during the Great Recession.

The Facts:

- Families in nearly all income and socioeconomic groups saw increases in wealth (assets minus liabilities) between 2013 and 2016. The finding comes from the latest results of the Federal Reserve’s Survey of Consumer Finances (SCF), which were released in late September. The survey is done every three years and asks households about their income, assets, liabilities, and financial behavior. The SCF is widely recognized as the most high quality and comprehensive source of nationally representative data on household wealth in the United States.

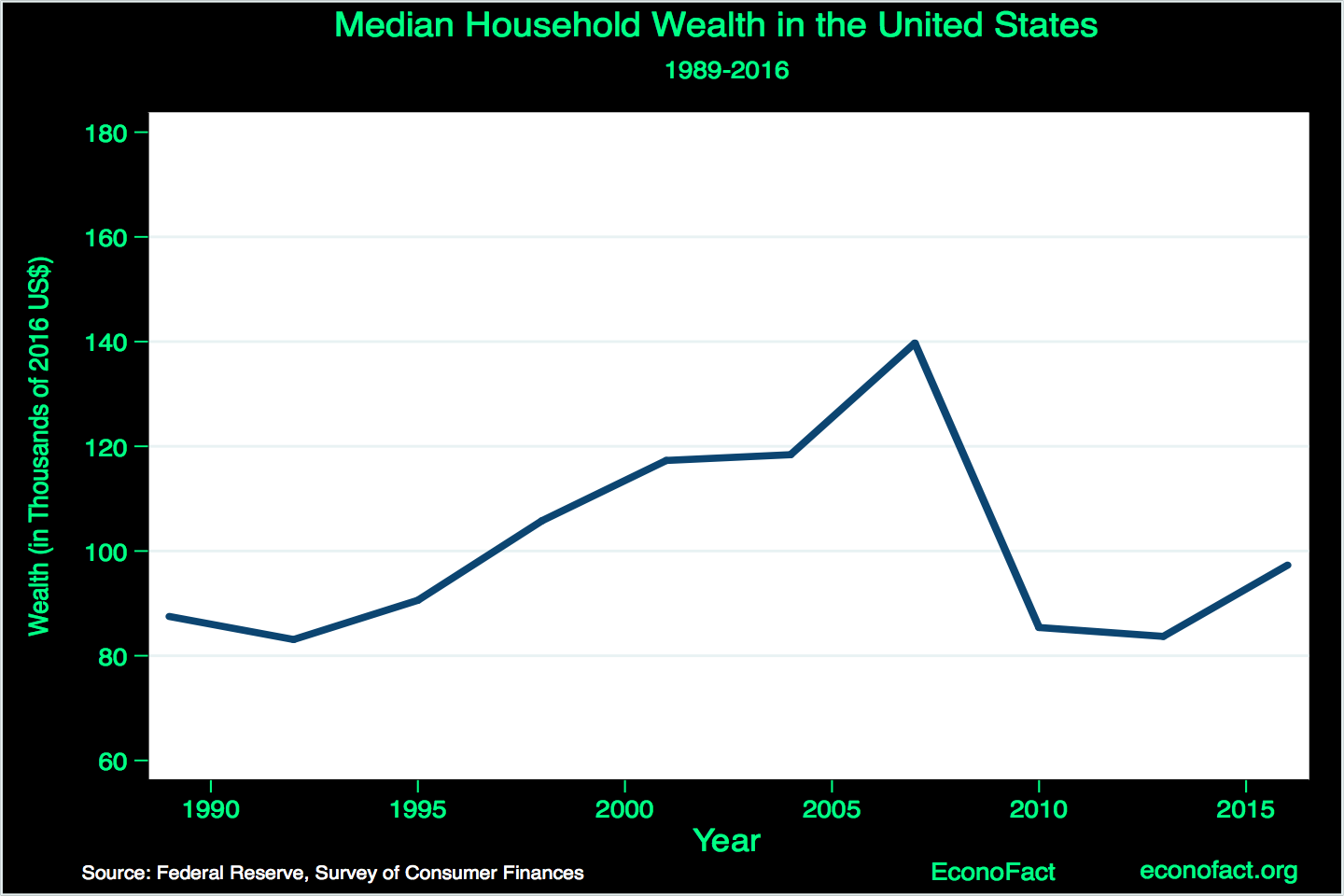

- Despite these gains, many households have not yet made up for the losses they suffered during the Great Recession and the weak early part of the recovery that followed. For example, median wealth (i.e. the wealth of the typical household) was $97,300 in 2016, up 16 percent from its inflation-adjusted value in 2013, but, on net, down 30 percent from its inflation-adjusted value in 2007. Indeed, median household wealth would have to increase by an additional 8 percent to recover to even its 1998 value in inflation-adjusted terms (see chart).

- The typical household has made some progress in building wealth since the late 1980s, with median wealth in 2016 about 11 percent higher than median wealth in 1989 after adjusting for inflation. But the ability to build wealth among households in the middle and lower part of the distribution has greatly fallen short of that of the richest households. One result is that the distribution of wealth has become much more unequal. The bottom 90 percent of the wealth distribution accounted for just 23 percent of total household wealth in the United States in 2016, down from a share of 33 percent in 1989. In contrast, the top 1 percent of the distribution accounted for 39 percent of total wealth in 2016, up from a share of about 30 percent in 1989.

- Nonwhite and Hispanic families saw larger proportional increases in wealth between 2013 and 2016 than white families. The wealth of the typical nonwhite family was up 29 percent relative to 2013 in inflation-adjusted terms and the wealth of the typical Hispanic family rose 46 percent; meanwhile, the typical white family saw an increase of 17 percent. However, the larger proportional gains for the nonwhite and Hispanic families partly reflect the fact that the absolute wealth of these groups is very low, at $17,600 for the typical nonwhite family in 2016 and $20,700 for the typical Hispanic family — compared with $171,000 for the typical white family. Such low levels of wealth imply that many of these families have a limited buffer against job loss or unexpected spending needs and are on track to have a very limited ability to supplement their Social Security income and any other pension income in retirement.

- One of the reasons many households struggle to build wealth is that they have difficulty saving. Only 55 percent of households in the 2016 SCF reported saving over the preceding year (up from 53 percent in 2013). For households in the lower half of the income distribution, only 43 percent reported saving.

- Research suggests that one of the most effective ways to get many households to save is by providing a commitment device that makes saving easier and more automatic. One such mechanism would be workplace retirement savings plans like 401(k) plans, particularly when designed such that new workers are “defaulted” into the plan (with the choice of opting out). However, data from the Department of Labor suggest that only 47 percent of private employers offered access to 401(k) and similar “defined contribution” plans as of early 2017. The 2016 SCF shows that the share of families with a head between ages 45 and 64 (key retirement saving years) that had a retirement saving account was only about 60 percent in 2016. This share has not increased at all since the 1990s.

What this Means:

Although the 2016 Survey of Consumer Finances revealed broad-based good news about how the financial situation of U.S. households evolved between 2013 and 2016, there is also cause for concern. After adjusting for inflation, the wealth of the typical household remains materially behind where it was in the first decade of the 2000s and a large share of households seem to be having difficulty saving. Policies that encourage more firms to offer well-designed workplace retirement saving plans such as tax breaks for setting up such plans could help make it easier for households to build wealth. It is also important to preserve institutions that help households protect any savings that they have such as the Department of Labor’s Fiduciary Duty Rule and the Consumer Financial Protection Bureau.