Consumer Financial Protection: In Need of Protection

Harvard University

The Issue:

The Consumer Financial Protection Bureau (CFPB) was established by the Dodd-Frank Act in 2010 with a mandate to ensure that “markets for consumer financial products and services are fair, transparent, and competitive” and to “protect consumers from unfair, deceptive, or abusive acts and practices” of financial service providers. The CFPB writes rules, supervises banks and non-bank financial institutions, conducts research on consumer use of financial services, and maintains a public consumer complaint database. There is considerable hostility to the CFPB among Congressional Republicans. In the past month several bills have been introduced that would curtail the CFPB including legislation introduced by Representative John Ratcliffe and Senator Ted Cruz to abolish the CFPB. Representative Jeb Hensarling, chair of the House Financial Services Committee, has written that the CFPB “has eroded freedom, trampled due process, and killed jobs. It must go.” Opponents charge that the CFPB lacks accountability, that it publicizes unverified complaints against financial institutions, and that it promulgates rules without regard to costs, thereby reducing the availability of financial services.Research demonstrates pervasive financial illiteracy and a troubling incidence of mistakes: decisions by consumers that jeopardize their financial well-being.

The Facts:

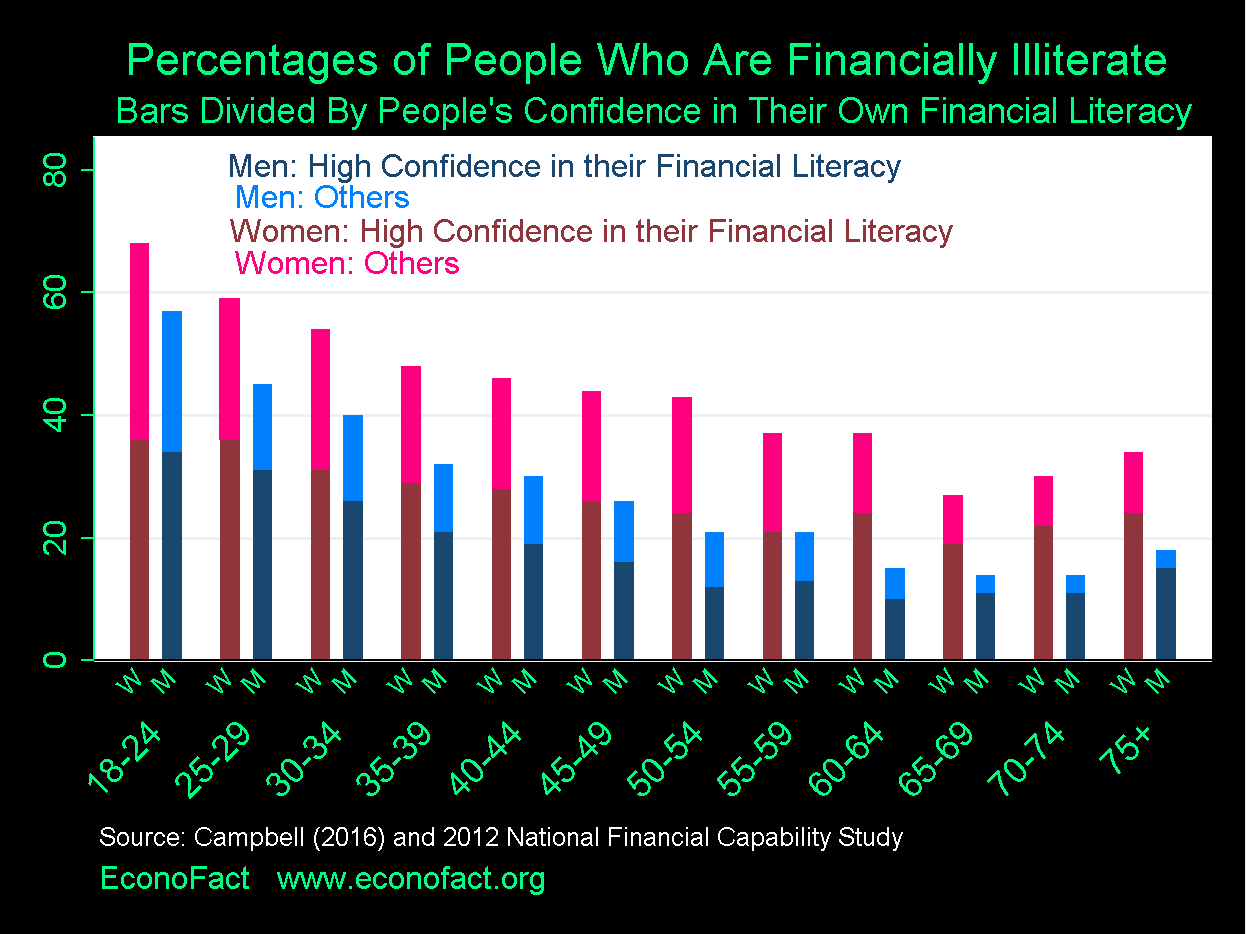

- The modern financial system is complex, and many people are ill equipped to make financial decisions in an unregulated environment. The 2012 National Financial Capability Study found that 28 percent of men and 44 percent of women are financially illiterate, in the sense that they can correctly answer two or less out of five basic finance questions, a lower score than can be achieved on average by guessing answers randomly (see chart). Financial illiteracy is particularly common among young adults and the elderly. However, a majority of financially illiterate adults state high confidence in their ability to manage their finances, suggesting that they may not seek help even if they need it. (See for instance my work on the case for consumer financial protection and how it applies to mortgages, payday lending and retirement savings, as well as how some households make serious investment mistakes).

- The CFPB conducts research that reveals the actual patterns of consumer financial product usage, for example the incidence of repeated borrowing at high interest rates from banks and payday lenders. Such research cannot be undertaken without the powers of the CFPB to obtain data from financial service providers. It informs the CFPB’s rulemaking and the legislative process in Congress and the states.

- The CFPB has produced a relatively small number of major new rules through a deliberate process. In 2013 a rule took effect requiring fee disclosures in remittance transfers to foreign countries; in 2014 a rule defined the standards that lenders must use in assessing borrowers’ ability to repay mortgages, and the standards for qualified mortgages that, under the Dodd-Frank Act, provide greater protection against litigation to lenders who issue them; in 2015 a rule took effect integrating and simplifying the disclosure forms that mortgage borrowers receive; and in 2016 the CFPB issued a rule scheduled to take effect in 2017 regulating the terms of prepaid cards. The CFPB has sought comments on proposed rules concerning arbitration in consumer financial disputes and the terms of payday lending. None of the rules currently in effect are plausibly responsible for major changes in the availability of household credit.

- Following a mandate in the Dodd-Frank Act, the CFPB has established a database of complaints against financial institutions. The database now contains over 700,000 complaints, and the CFPB has made it available online. Opponents charge that individual complaints are unverified, but this concern exaggerates the importance of any one complaint and underestimates the important information that can be derived from observing a pattern of complaints in a large database. Moreover, online reviews are an increasingly important reality for all consumer-facing businesses.

- The CFPB must consider the cost of its rules relative to their benefits. The Dodd-Frank Act imposed requirements on the CFPB to conduct cost-benefit analysis of its regulations, and to review their impact in a retrospective analysis after five years. The General Accounting Office oversees this aspect of the CFPB’s work and has certified that it has fulfilled its obligations.

- The CFPB has no supervisory authority over small banks with assets of less than $10 billion, and it structures its rules to limit the impact on small institutions. This should alleviate concerns of excessive regulatory burden on smaller credit providers. The size threshold for CFPB oversight could be adjusted without changing any other aspects of the current legal framework.

What this Means:

Consumer financial protection is just as reasonable an endeavor as regulation of health care provision and access to pharmaceuticals. Research has demonstrated pervasive financial illiteracy and a troubling incidence of mistakes: decisions by consumers that jeopardize their financial well-being. Such mistakes encourage the provision of complex financial products that exploit consumer confusion and may contribute to systemic financial risk. These considerations demonstrate the importance of the CFPB, while the rules under which it operates limit the potential for regulatory overreach. The CFPB is a young agency that has acted responsibly under its Dodd-Frank mandate. The intensity of opposition to the CFPB is incommensurate with the scope of its actions to date and is not based on any evidence of harm to the economy. Under these circumstances it is important to preserve the CFPB’s independent ability to regulate financial services in the interests of consumers.

Topics:

Financial RegulationLike what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.