Could Increasing Market Power Among Firms be Hurting Workers’ Wages?

University of Pennsylvania

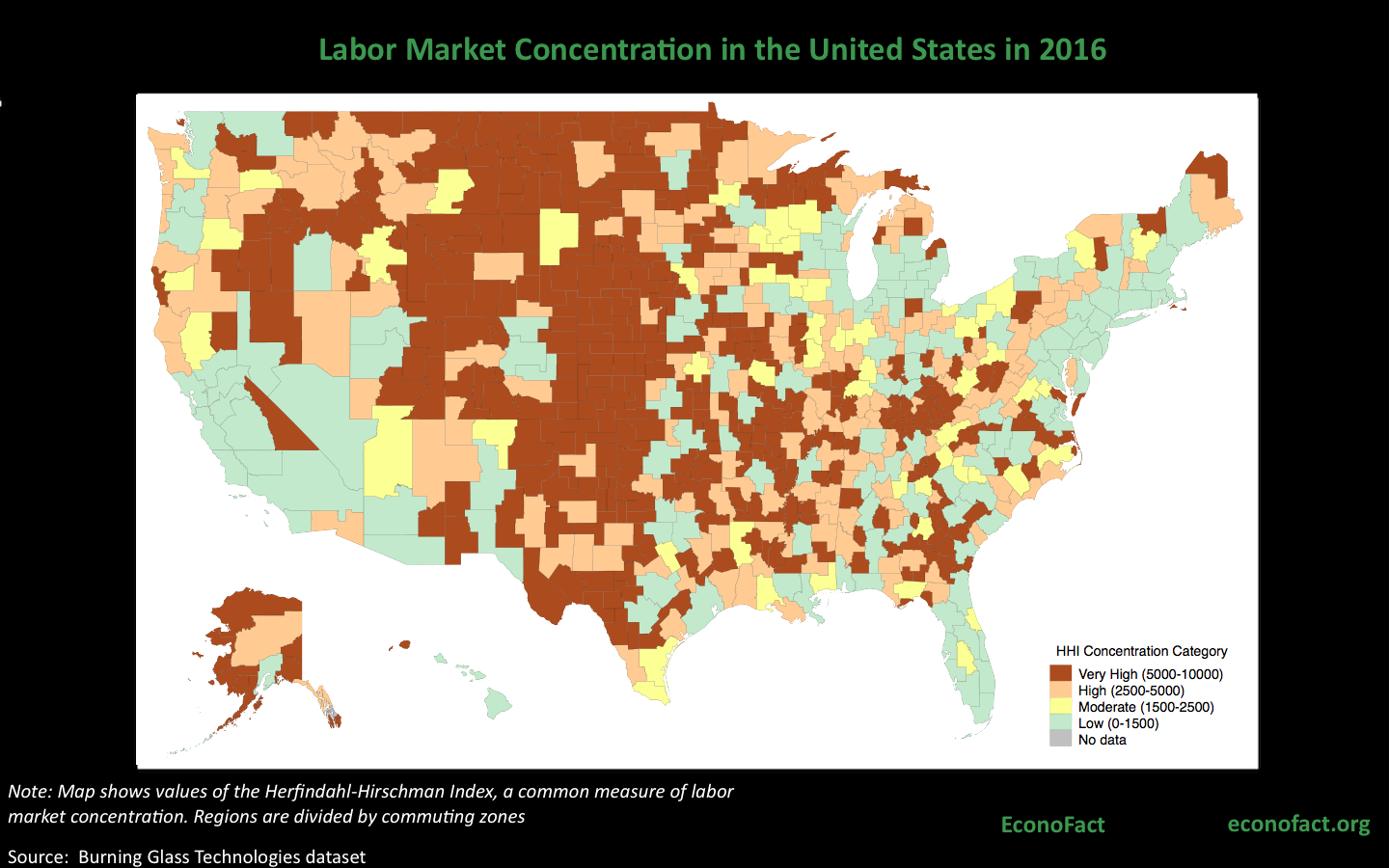

(Click here for a larger version of the map)

The Issue:

Wages for the typical American worker have been stagnant since the late 1970s, growing only 0.2 percent per year on average when adjusting for inflation. Increasing competition with low-wage workers abroad, automation, the decreasing power of unions, and slow productivity growth are often cited as possible explanations for this poor wage performance, particularly for less-educated workers. But another possible factor has been receiving increasing attention lately: a lack of competition for workers among firms, which is exacerbated by mergers and other circumstances that reduce competition for workers.

A small number of firms account for a large share of hiring in many U.S. labor markets. When a few firms dominate hiring, workers may be paid lower wages.

The Facts:

- Concerns with diminished competition among firms have tended to center on the impact on consumers in terms of higher prices, lower quality of products, or decreased innovation. However, firms’ market power can also impact the suppliers of inputs like raw materials or labor. When a few firms dominate hiring in a labor market, workers may be paid lower wages. People's ability to negotiate for better wages depends, in part, on competition for workers among firms. When there is high labor market concentration (a situation where there are very few firms hiring workers or there is a dominant firm in the market), workers are put in a weak negotiation position and wages are lower than would otherwise be the case. One example of this is the company town, where a single company — such as a mine — dominates employment. In theory, workers could move to a place where they could earn higher wages. But moving is costly. Family ties, cultural affinity, or lack of knowledge about other locations can make a person accept a lower wage rather than move. Indeed, applications for a job decline rapidly with distance and more than 80 percent of job applications occur where the job applicant and prospective employer are within the same commuting zone (see here). The relationship between firm concentration and worker wages as well as its relationship to the share of production that goes to workers has been the subject of increasing interest by economists (see here and here for articles in the press).

- The average U.S. labor market is highly concentrated. This means that a relatively small number of firms account for a large share of hiring for each occupation within many commuting zones. The degree of labor market concentration can be gauged with a version of an index already used by regulators to measure competition in the sale of products. The Department of Justice and the Federal Trade Commission use values of the Herfindahl-Hirschman Index (HHI) to establish the conditions under which mergers and acquisitions among competitors are lawful (see here). The value of the index is higher when there are fewer firms selling a product or when one firm dominates the market (for example, for two firms the HHI is higher when one firm sells 90 percent of products and the other 10 percent than when each of the two firms sells 50 percent of products). Under the merger guidelines used by regulators, an HHI above 1,500 is “moderately concentrated,” and an HHI above 2,500 is “highly concentrated.” In our research, my co-authors and I have constructed an HHI index that measures how concentrated labor markets are in terms of hiring. We use data on vacancies listed online to calculate the share of each firm among posted vacancies, just as one would calculate the share of each firm in the sales of a product. We find that U.S. labor markets tend to be highly concentrated, with an average HHI of 3,953, which is equivalent to 2.5 firms hiring in the case of equal number of job vacancies for each firm. Overall, 54 percent of labor markets are highly concentrated, having an index above 2,500 HHI, which corresponds to four firms hiring with equal shares in hiring. These highly concentrated markets account for 17 percent of U.S. employment. Larger cities generally have lower labor market concentration while labor markets are more concentrated in rural areas (see map). Labor market concentration also varies across regions of the country, with higher concentration across a broad swath of the middle of the country, and by occupation; among the 30 largest occupations, the least concentrated occupation is "Registered nurses" while the most concentrated is "Marketing Managers." Analysis using data from other sources offers similar results.

- There is evidence that higher concentration among employers is associated with lower wages for workers. Our research shows that labor markets with higher levels of employer concentration tend to have lower wages. This, in itself, does not prove that greater market power by employers is leading to lower wages for workers. For example, the association could be driven by the fact that larger cities tend to have both a higher number of firms and higher wages, perhaps due to a higher cost of living. However, a stronger case can be made if we look at how changes in concentration within a given market over time affect wages over that same period. When considering changes in HHI for labor markets, our analysis of data from CareerBuilder.com indicates that an increase in labor market concentration is associated with a decrease in wages, even when taking into account factors like how tight the labor market is in a particular area and occupation. We estimate that, on average, a 10 percent increase in concentration is associated with a 0.3 to 1.3 percent decrease in wages. Furthermore, this effect is larger in smaller cities.

- Given the extent of existing employer concentration in U.S. labor markets, mergers and other circumstances that reduce competition for workers among firms are likely to have a negative impact on wages. One example of this is no-poaching agreements. These occur when employers agree with each other not to hire one another’s workers, which is a form of collusion (that is, anticompetitive behavior) among firms (see here). These types of agreements can occur even when firms do not sell products that compete. For example, consider the federal antitrust case that was conducted against eBay, Inc., and Intuit, Inc. Intuit’s principal products are TurboTax, a popular income tax preparation program, and Quickbooks, a popular business program for bookkeeping and accounting while eBay is a popular online auction site, which is not in the business of producing or selling software. Authorities made the case that these two firms found it profitable to agree with one another not to poach each other’s “specialized computer engineers and scientists.” The fact that the two firms found it worthwhile to enter into this agreement is a strong indicator that the firms were competitors in this particular portion of the labor market and also that, between the two of them, they had enough market power to make the agreement profitable by limiting wages. Indeed, if the workers could easily go work for a third company, this no-poaching agreement between only these two firms would not be very useful in limiting workers’ opportunities to chase higher wages. There are other recent examples in which the Department of Justice has focused on the impact of competition among firms on the market for workers (see here and here).

What this Means:

New research provides compelling (albeit early stage) evidence that higher labor market concentration is associated with significantly lower posted wages for new jobs. This has implications for merger and antitrust policy, and for the significance of no-poaching agreements in reducing labor market competition. To date, no court has ever condemned a merger because of its anticompetitive effects in labor markets. This may be because it has not been clear how widespread labor market power truly is, and how much it affects wages. But mergers that increase labor market concentration should invite very close scrutiny. Analytic tools like an HHI for the labor market can be used by regulators to make a prima facie case against a merger that significantly increases labor market concentration and runs the risk of anticompetitively suppressing wages or salaries. Merger policy does not need to change fundamentally in order to review mergers that threaten to increase labor market concentration and allow for anticompetitive wage suppression.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.