Is Financial Regulation Doing the Right Amount to Prevent Cascading Crises?

Brandeis University

{kind=link}

The Issue:

One of the perceived causes of the severity of the 2008 financial crisis was that some institutions that failed, or came close to failing, were systemically important. Because of their size, their interconnectedness with other financial firms, or the nature of their business activities, the failure of such institutions had the potential to cause a cascade of other problems, as happened after Lehman Brothers went bankrupt in September 2008. Part of the response to the crisis, embodied in the 2010 Dodd-Frank financial reform bill, was to make efforts to guard against this type of risk by identifying systemically important financial institutions (SIFIs) and subjecting them to more regulation than institutions that are not considered systemically important. But the Dodd-Frank financial reforms have come under attack, with opponents of these reforms arguing that they impede bank activity and therefore hurt economic performance.The Dodd-Frank financial reform imposed stricter oversight on the institutions it determined posed a risk of harmful spillovers to the broader economy.

The Facts:

- Systemic risk arises when stress at one financial institution directly causes difficulties at other institutions. For example, the failure of Lehman Brothers in September 2008 led to great stress throughout the financial system because of the uncertainty concerning which institutions would be adversely affected by Lehman’s inability to make good on its commitments. The Lehman episode reflected the opacity and the complexity of financial linkages at that time, and the systemic risk that contributed to the financial crisis. Of course, the interactions among financial institutions that can give rise to systemic risks are also vital to the functioning of the economic system, and can even foster stability, as pointed out in 2013 by then-Federal Reserve Vice Chair Janet Yellen.

- In theory, a financial institution is systemically important if its failure could cause a cascade of other problems or even failures in the financial system. But, in practical terms, determining the criteria by which institutions are deemed to be systemically important is matter of debate. Under Dodd-Frank, banks with assets of $50 billion or more were designated as SIFIs, which subjects them to stricter oversight from the Federal Reserve (see here). Although it is correlated with systemic risk, size can be an imperfect measure of the systemic risk that a financial institution poses. The systemic risk created by an institution will also be a function of its complexity and the specific activities it undertakes – for example the extent of mismatches in currency and maturity between an institution’s assets and its liabilities. In the case of Lehman Brothers, the institution’s complexity, its range of activities, and its opacity meant that its failure caused systemic problems that a less opaque and complex organization might not have created. Research on measures of systemic risk that improve on merely measuring size is an important ongoing area of work (see here and here for examples).

- The danger posed by systemic risk comes because financial institutions do not fully account for the effects of their decisions on others and, consequently, lack incentives to adequately guard against the possible wider adverse consequences of their actions. ”Moral hazard” is the term used for a situation where an institution engages in risky behavior because it will not fully bear the cost of a bad outcome. Moral hazard is particularly likely to be a problem if an institution expects that it might be bailed out by regulators, either because of a pre-arranged plan or because of the threat to the system as a whole, as captured by the idea of too big to fail. One goal of the Dodd-Frank reforms of 2010 was to mitigate the systemic risk consequences of moral hazard.

- Among other provisions, Dodd-Frank required SIFIs to maintain more capital than other financial institutions. Capital is the net worth or equity of a financial institution. It serves as a buffer at times of stress since, unlike with borrowed funding, there is not a set requirement that the institution repay the funds on demand or at a specific time. But bank profitability tends to decrease as a bank maintains a larger equity cushion, and for this reason, financial institutions may have incentives to be “undercapitalized” relative to what would be optimal from a systemic perspective. This undercapitalization can occur because the market may not discipline an institution for taking on this extra risk. For example, depositors do not have an incentive to monitor a bank’s activity if government deposit insurance protects their funds. Also, a financial institution that is considered too big to fail, and therefore reasonably considers receiving a bailout if it faces collapse, may have an incentive to engage in a moral hazard play, taking a “heads I win, tails you lose” strategy that combines undercapitalization with excessive risk-taking. The increase in capital requirements mandated by Dodd-Frank make it more likely that losses at a financial institution will be entirely borne by the shareholders of that institution rather than taxpayers in the form of a bailout. The extra capital required of SIFIs better aligns incentives of the institutions’ managers and owners with the goal of system-wide financial stability. A variety of measures indicate that banks’ capitalizations have risen in the United States in the post-Dodd-Frank period (see here).

- Dodd-Frank also extended the oversight authority of the Financial Stability Oversight Board to include non-bank financial institutions deemed systemically important, for example to certain large insurance companies. These types of non-bank institutions had been lightly regulated before the crisis. Absent these regulations, there is an incentive for financial activity to migrate from regulated banks to non-bank financial institutions, which are sometimes called the "shadow banking" sector. Under Dodd-Frank, the Financial Stability Oversight Board (FSOC) has the authority to monitor systemic risk and regulate systemically important institutions regardless of their jurisdiction. Non-banks, such as insurance companies, which are designated as systemically important are subject to the greater oversight and tighter regulation that SIFIs face. This Dodd-Frank reform played an important role in limiting incentives for this type of regulatory migration.

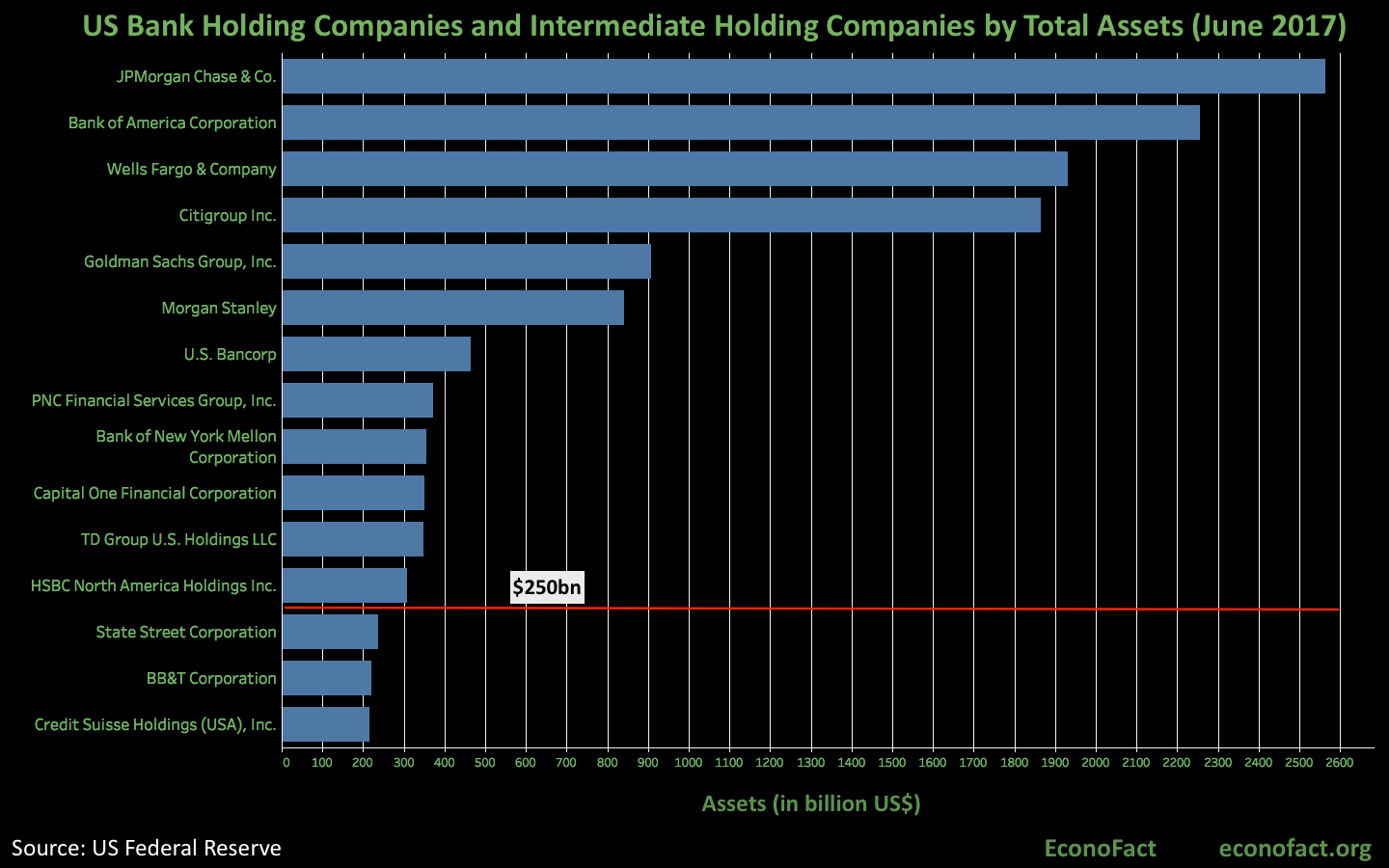

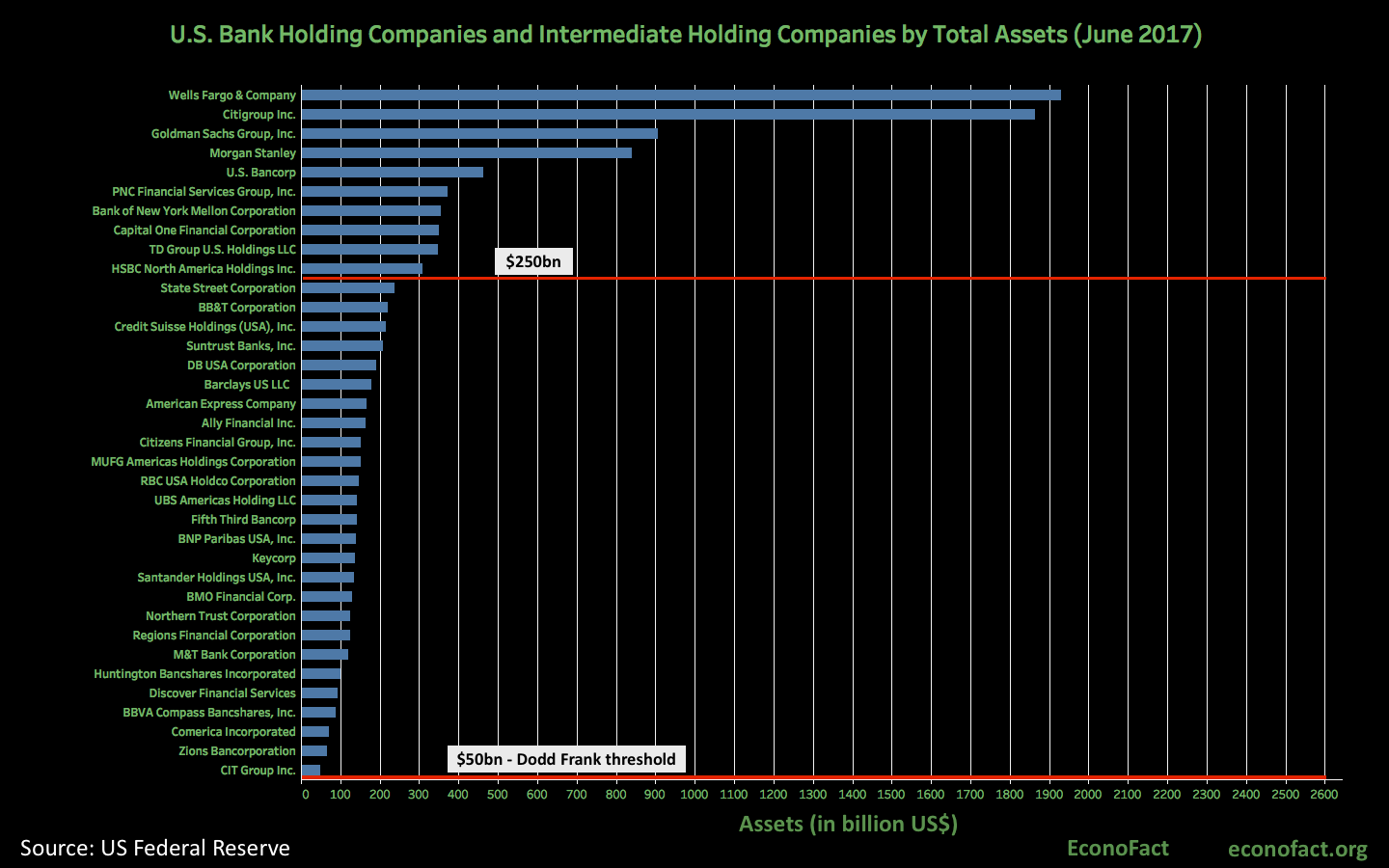

- As the last crisis has receded in memory, banks and other financial institutions have argued that the Dodd-Frank regulations are excessively restrictive and policymakers have begun to take steps in the direction of rolling them back. In June 2017, the United States Treasury responded to a directive from President Trump by releasing a series of recommendations targeted at weakening some of the important provisions of the Dodd Frank reform. In that month the House of Representatives also passed H.R.10, called the CHOICE Act, which would weaken a number of the Dodd-Frank reforms, including some designed to address systemic risk. In March 2018, a bipartisan majority in the Senate passed a much narrower reform of the Dodd-Frank Act, Senate Bill S.2155, that would reduce the number of institutions that are subject to SIFI regulations by raising the primary threshold from $50 billion to $250 billion in assets (Former Representative Barney Frank, who was among the original sponsors of Dodd-Frank, has indicated that the $50 billion threshold may have been too low, and perhaps a $125 billion threshold might have been more appropriate). This regulatory change would not affect mega-banks such as JP Morgan ($2,563 billion in assets), Bank of America ($2,256), Wells Fargo ($1,931) and Citigroup ($1,864), but would remove a number of important smaller institutions from that designation, including regionally important banks like as BB&T ($221 billion in assets), American Express ($167) and Fifth Third Bancorp ($141) (see chart). One potential consequence of this change, if implemented, would be a round of merger and acquisition activity in the financial services sector as institutions responded to the lifting of the previously-binding constraint by merging to form larger institutions that are, nonetheless, still under the $250 billion threshold. Differences between the Senate and House bills, however, mean that outlook regarding the ability to craft a compromise bill that would be able to pass through both houses of Congress is cloudy.

What this Means:

Some of the most important changes introduced by Dodd-Frank involved taking actions to try to limit the potential damage that one failing institution could have on broader areas of the financial system. Taking a system-wide approach to evaluating the risks posed by individual institutions, Dodd-Frank imposed stricter requirements on the institutions it deemed had the higher risk of harmful spillovers to the broader economy. However, these reforms come at a cost. Financial regulation involves a tradeoff between enhancing safety and stability — and limiting the costs and burdens imposed on regulated institutions and the economy as a whole. Determining where to draw the line is an area of legitimate discussion and debate. The biggest costs though, are those that come with a financial crisis of like the one the United States went through in 2008 and 2009.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.