Banks, Credit Crunches, and the Economy

May 15, 2023

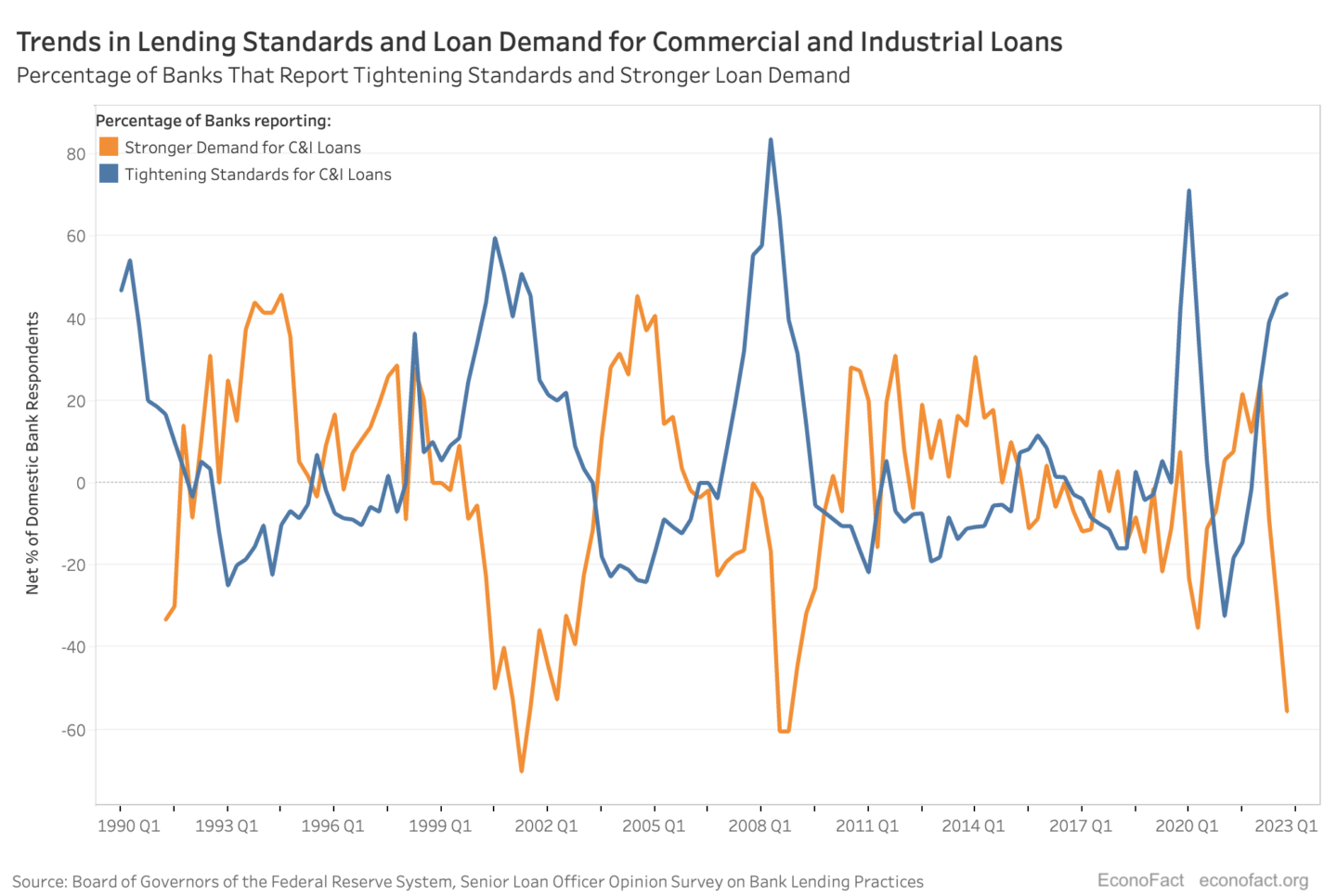

Credit crunches due to bank distress can undermine economic growth. There is evidence of tighter credit and lower demand for loans in the recent bank turmoil.

May 15, 2023

Credit crunches due to bank distress can undermine economic growth. There is evidence of tighter credit and lower demand for loans in the recent bank turmoil.

March 30, 2023

Commercial banking is inherently fragile. This fragility can be mitigated through appropriate bank management practices and good regulation and oversight.

September 8, 2019

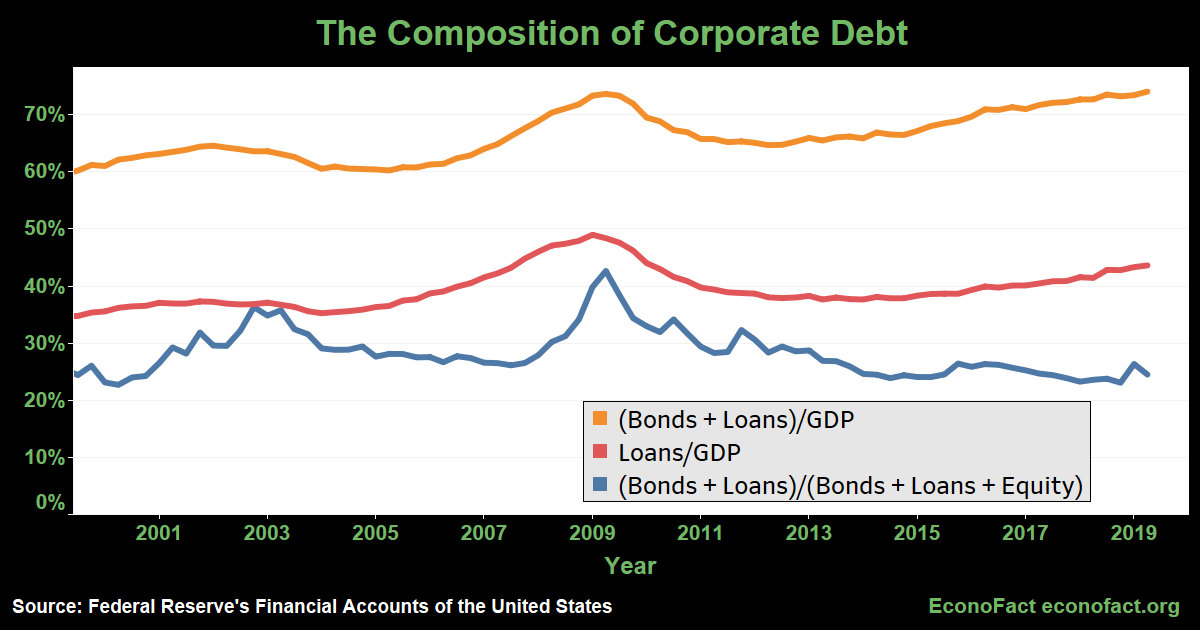

Corporate debt in the U.S. stands at or near all-time highs. It is important to pay attention not just to the amount of debt but also to its composition.

April 12, 2018

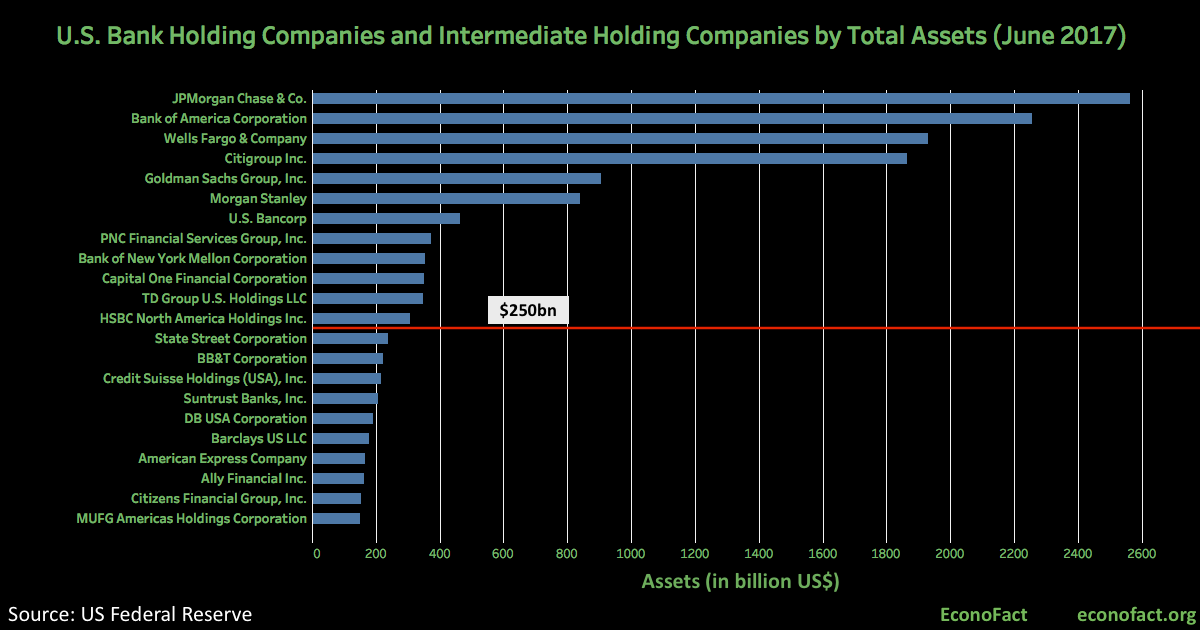

The Dodd-Frank financial reform imposed stricter oversight on the institutions that pose a risk of harmful spillovers to the broader economy. Financial regulation involves a tradeoff between enhancing safety and stability — and limiting the costs and burdens imposed on institutions and the economy as a whole.

September 8, 2017

While all sides agree there is scope for improvement, there are significant disagreements on the extent and direction of needed reforms.

March 1, 2017

Critics say the rule imposes a heavy burden on banks and does not address the root causes that led to the Great Recession.