Banks, Credit Crunches, and the Economy

Fletcher School, Tufts University

The Issue:

Financial disruptions in 2008 contributed to the deep economic downturn that came to be known as the Great Recession. Could current bank failures similarly lead to a recession? The $532 billion of assets of the three banks that failed in March and April 2023 exceed the inflation-adjusted value of $526 billion of assets of the 25 banks that failed in 2008. Furthermore, there are concerns that the crisis may not be contained and other mid-sized banks could also fail. However, the current situation differs in many ways from the underlying economic circumstances at the outset of the Great Recession. Still, that experience, as well as others, show how financial distress can lead to macroeconomic weakness which then contributes to further financial distress, resulting in a downward spiral during which credit becomes tight, investment is curtailed, and growth stalls.

Bank distress can have adverse consequences for borrowers and the broader economy.

The Facts:

- One source of recent bank vulnerabilities is the rapid increase in interest rates. The Federal Reserve has attempted to bring down inflation by raising interest rates at the fastest clip since the 1980s, from near zero in March of 2022 to a range between 5% and 5.25% in May 2023. The sudden shift to higher interest rates creates fragility in the banking sector. Banks take in deposits that can be withdrawn in the short term and use them to make loans and invest in securities at interest rates that are fixed for some time. As interest rates rise, the value of banks’ existing portfolio decreases as new investments at higher rates are more attractive. By one estimate, the U.S. banking system’s market value of assets is $2.2 trillion lower than suggested by their book value of assets accounting for loan portfolios held to maturity. These book losses are realized if banks have to sell those assets to cover withdrawals from depositors. At the same time banks face challenges in maintaining deposit levels, depositors are less willing to place their money in low-return checking and savings accounts as higher-interest opportunities become increasingly available.

- Banks that have failed so far have had specific weaknesses that made them particularly vulnerable. Silicon Valley Bank (SVB) was particularly exposed to risk from rising interest rates as it had heavily invested in longer-term government bonds which lost market value as interest rates rose and its management failed to hedge against this risk. SVB was also especially vulnerable to a run by depositors because over 90 percent of the value of its deposits exceeded the $250,000 amount guaranteed by the Federal through the Federal Deposit Insurance Corporation (FDIC). Depositors holding accounts in excess of this guaranteed amount, both individuals and companies (whose accounts were used for making payroll, among other reasons) are only partially protected in case of bank failure so they have an incentive to withdraw funds at the first sign of trouble. Moreover, depositors were connected to each other through business and social groups, so news traveled quickly seeding the conditions for a classic bank run at Twitter speed. Signature Bank also had about 90% of its assets uninsured and its portfolio was heavily concentrated in crypto deposits. Both banks grew very rapidly with inadequate risk and liquidity management practices in place and, while regulators had raised concerns about these risks, they had not taken more forceful actions to address them, according to a GAO report. The latest to fail, First Republic Bank, catered to wealthy depositors and for this reason also had a high share of uninsured deposits that made it more vulnerable to a bank run as its bond assets lost value amidst rising interest rates (see here).

- Commercial banks reduce lending when their deposits fall or when they otherwise cannot meet regulatory requirements. Deposits represent an important source of banks’ ability to lend. As a bank’s deposits decrease, it has less resources available for lending since other sources of funds are not as easily obtained. A bank may also cut lending in an effort to satisfy regulations such as meeting or exceeding the Capital Adequacy Ratio. Regulators require banks to have enough capital on reserve to handle a certain amount of loan losses. The Capital Adequacy Ratio decreases when loans fail and the bank sees its loan loss reserves decline. The bank can then increase its Capital Adequacy Ratio by using funds that would otherwise be devoted to commercial loans or by shifting from loans to other assets that are less risky (such as government securities). There is evidence that this effect contributed to the cutback in bank lending in New England in the 1990 – 1991 recession when there was a collapse in that region’s real estate market. A bank may choose to reduce lending if there are concerns about solvency even if it is not yet hitting up against the formal capital adequacy ratio requirement.

- A decrease in bank lending may reflect a fall in the supply of loans by banks, for reasons discussed above, or a decrease in demand for loans that has little to do with the ability of banks to lend – and this distinction is important for understanding whether there is a credit crunch. A credit crunch occurs when borrowers who would otherwise receive loans are precluded from doing so because of a restriction on the supply of loans by banks. But a reduction in bank lending could also reflect a decrease in borrowers’ demand for loans. Researchers have used a variety of methods to identify when there is a credit crunch rather than just a lower demand for loans. For example, a credit crunch could be identified through looking for differential borrowing, employment, and performance patterns by bank-dependent companies as compared to those that have access to financing through bond or equity markets. Bank dependent companies are typically smaller than those that have access to other types of financing. Researchers have also used information from bank examiners to identify banks that are facing regulatory restrictions and must therefore cut lending. A third strategy uses data from Japan where large companies are dependent on financing from a main bank. These banks faced downgrades at different times, and it has been shown that a company’s foreign investment decreases as their respective main bank is downgraded even as companies linked to healthier banks take advantage of these investment opportunities abroad.

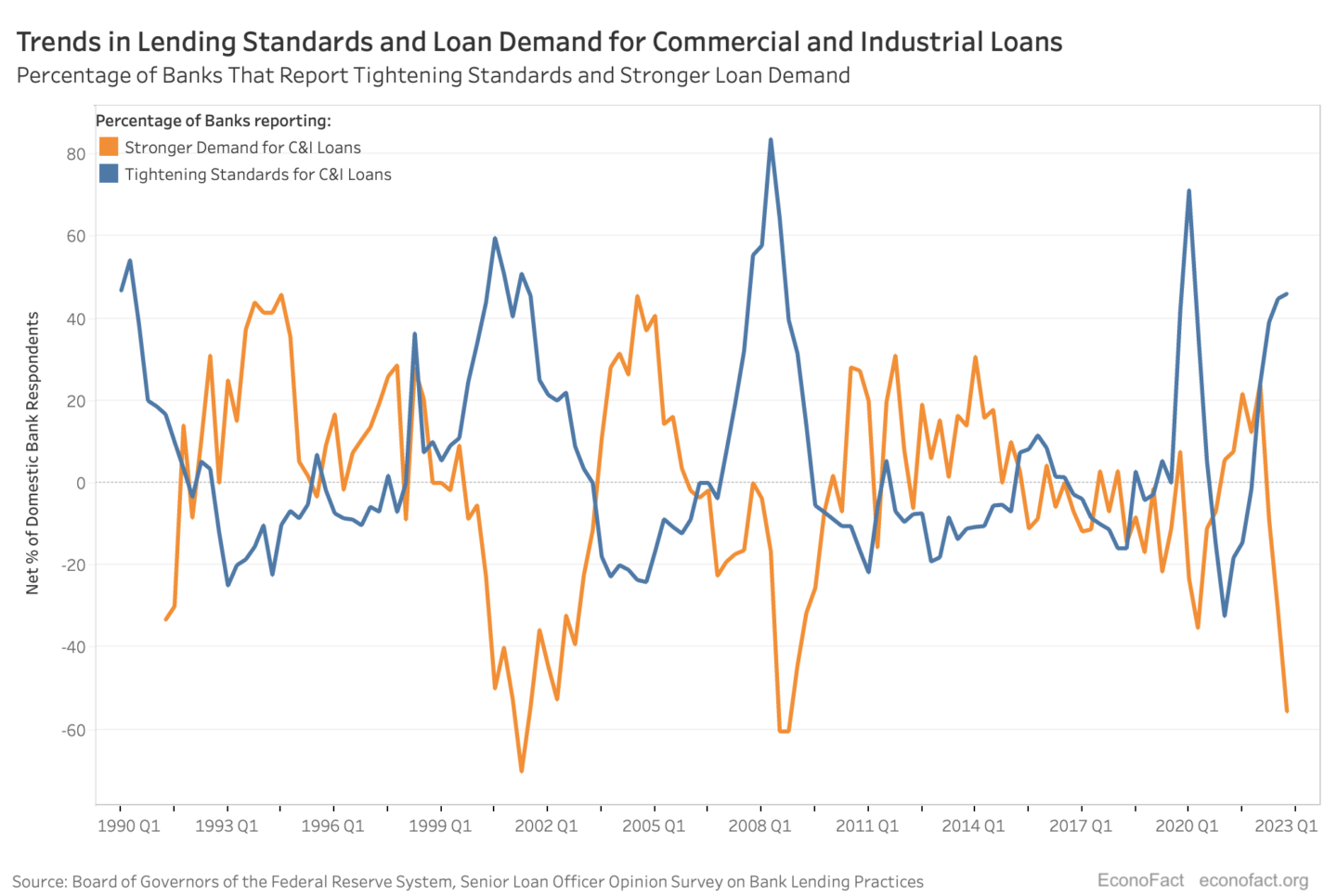

- There is evidence of both a tightening of credit by banks and decreasing demand for loans in the recent bank turmoil according to recent data from the Federal Reserve. The Board of Governors of the Federal Reserve publishes the results from an opinion survey by banks’ senior loan officers each quarter, with the most recent survey sent to 65 domestic banks at the end of March 2023 with responses due by April 7. One set of questions asks whether banks tightened lending standards, which, roughly speaking, indicates a credit crunch for the supply of loans. Another set asks whether banks report stronger demand for loans. The chart shows the net percentage of banks answering that lending standards were tightened and the net percentage answering there was stronger demand for loans (net percentages are those answering tightened minus those answering eased, and those answering stronger minus those answering weaker, respectively). The chart shows that the past two years have been marked by both a tightening of lending standards and a fall in loan demand.

- Credit crunches due to bank distress can undermine investment and economic growth. An early and influential analysis by Ben Bernanke, who went on to the Chairmanship of the Federal Reserve and served during the 2008 Great Financial Crisis, analyzed the effects of bank failures during the Great Depression. He found that bank failures had a particularly strong effect in reducing the amount of borrowing by households, farmers, and small businesses in that period, which contributed to the severity and duration of the Great Depression. The banking system has been made more resilient since that time, but there is still evidence of the effect of a credit crunch on regional economies. For example, researchers have studied the 1990-1991 recession when there was a collapse of real estate values in New England and bank weakness at that time was found to have an effect on small and medium-sized businesses in that region at that time. As to the current situation, the April 2023 IMF Global Financial Stability Report (p. 3) argued that the credit crunch in the United States could reduce lending by 1 percent, which would lower GDP growth by almost 0.5 percentage points.

What this Means:

Finance is important for the operation of the economy, and banks are an important source of finance for many households and small and medium-sized businesses. Banks can be put in distress through loan failures or depositor runs. A current concern is banks’ exposure to commercial real estate loans, given the weakness in that market in the wake of COVID and much greater working from home. Imperiled banks can force a cutback in borrowing that slows economic growth. While the current situation is not comparable to the early 1930s when widespread bank failures played an important role in cratering the economy – banks are better regulated and safer now, and other forms of financing have developed – bank distress could still have adverse consequences for bank dependent borrowers and the broader economy.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.