Putting the Recent Swings in Stock Market Indexes into Context

Brandeis University

The Issue:

The volatility in the stock market in the first week of February 2018 stands in stark contrast to unusually low volatility throughout 2017. The past year was the first one ever that the Standard and Poor’s 500-stock index did not experience any decline greater than 3 percent. The past week, however, has seen some large moves in market indexes. After a stock selloff that began the prior Friday, the Standard & Poor’s 500-stock index fell by more than 4 percent on Monday, February 5. On Tuesday, February 6, it ended the session up by about 1.7 percent and then fell again on Thursday. This volatility has raised concerns about the relationship between the value of stocks and household wealth, and, more generally, what these market gyrations mean for overall economic performance.Stock market volatility has raised concerns about what these market gyrations mean for overall economic performance.

The Facts:

- Well-developed stock markets such as the New York Stock Exchange and the Nasdaq markets in the United States play a vital role by providing access to capital for businesses and by providing ways for people to invest their savings. A share of stock represents ownership in a publicly traded, for-profit company. Selling shares to the public is an important way for companies to raise money for new investments in plant and equipment, as well as other projects. At the same time, shares of companies are an important part of the set of financial assets households use to invest their savings. Households invest in stocks through direct purchases, through wealth management companies, or through pension funds. They earn a return on these investments as companies’ profits are paid out to them as dividends, or when they sell the shares of stock to another investor or back to the company.

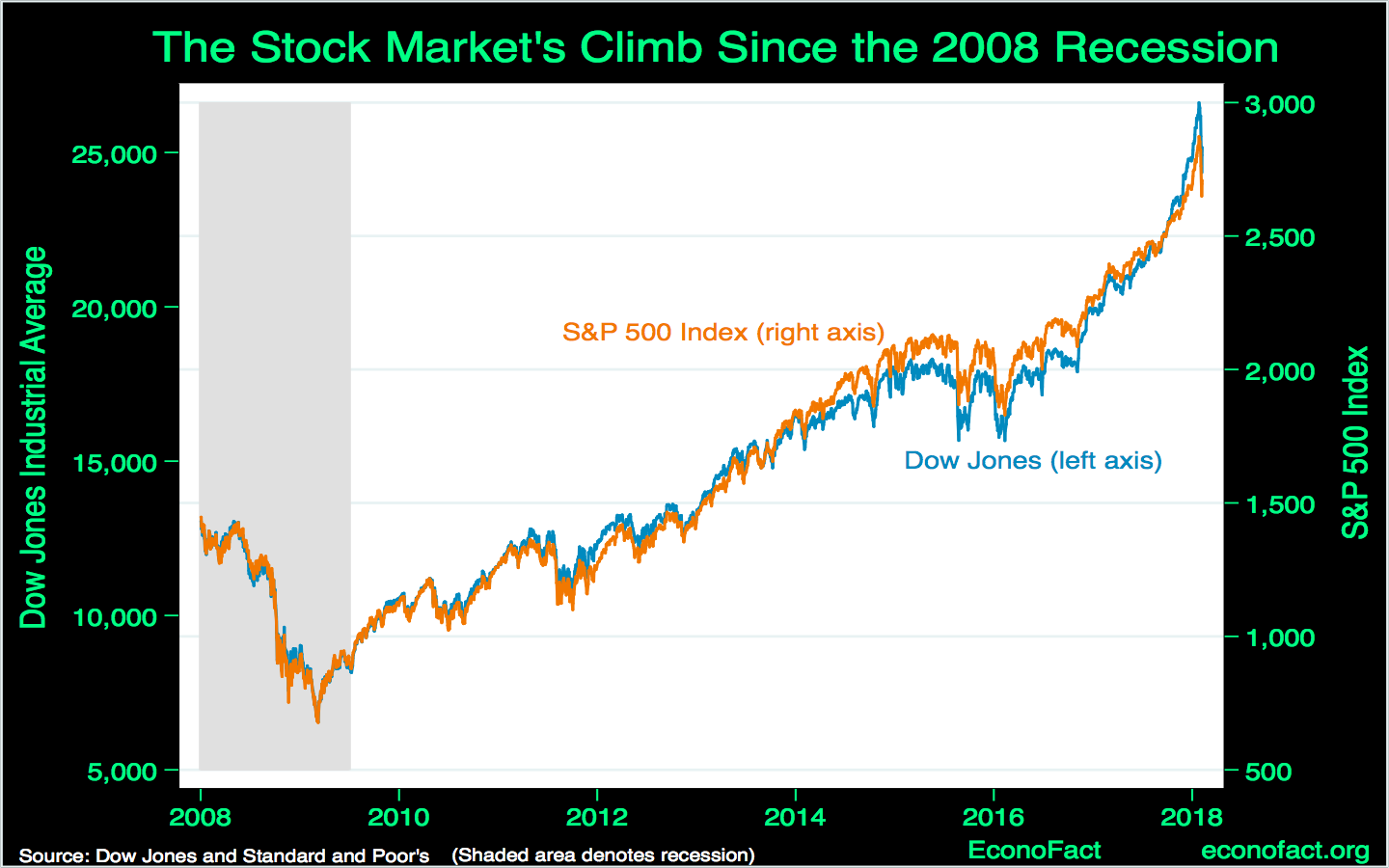

- Many different indexes track the performance of United States stock markets and provide somewhat distinct windows to evaluate the performance of stocks and the outlook for different types of companies. These indexes provide useful information about the prices of a range of companies’ shares and the returns that investors have earned by investing in those shares. The best-known stock market index is probably the Dow Jones Industrial Average (DJIA), which was created in 1896 and has been maintained ever since. This index is based on the average value of the shares of thirty different companies whose stocks are traded on the New York Stock Exchange (NYSE). The set of companies included in this index changes periodically, and the intent of these periodic changes is to ensure that the index remains a reasonable proxy for the larger economy. Today the index includes Apple; at its inception the index included the National Lead Company, which still exists but is not as central to the economy today as it was back then. Another widely followed index is the Standard and Poor’s 500 index (S & P 500), which is a market-capitalization-weighted index based on the stock prices of 500 firms with the largest market capitalizations among publicly traded U.S. companies. This index tilts toward large firms and covers about 80 percent of the investible universe of publicly traded stocks in the United States. A third closely watched index is the price of stocks on the Nasdaq exchange, with the shares traded on this exchange tilted towards the performance of the technology sector.

- Stock market indices have had a long positive run since the Great Recession. Viewed in the context of this long and sustained rise, the fluctuations of the past week are modest (see chart). The percentage change in an index is a better gauge of aggregate stock market performance than the changes in the index’s level or its “points”. Scaling point changes as a percent of the index value is important for understanding the real magnitude of a given change. When the DJIA fell almost 1200 points on Monday, February 5, 2018, it was the largest point move in its long history. However, because the DJIA has been experiencing a long positive run, this fall represented a 4.6 percent drop given that the index started the day at around 25,000. The day’s experience does not rank even in the top 20 largest drops of all time as measured as percentage change. In contrast, the 508-point index drop on October 19, 1987 represented a 22.6 percent drop in the value of the index.

- Today’s stock prices reflect what investors are willing to pay for all of the expected future dividends that a company will pay to its shareholders. A key word in the previous sentence is “expected” – people can only estimate what the future dividend payments will be. Therefore, any news about the fortunes of a company, whether the news is specifically about a particular company or more generally about broader economic performance, will influence investors’ perceptions about the stream of dividends likely to be paid in the future. Stock prices should move as soon as news like this is revealed to the market. But even in the absence of news about future corporate profits, share prices can rise or fall purely on the basis of what investors today are willing to pay for those profits and these changes may not reflect a change in views about the profits or dividends that the stock will generate.

- The recent volatility of stock market indices could reflect changing perceptions of the fortunes of the broad macroeconomy and the path of interest rates. There are many potential explanations for why investors could be changing their views about stock prices. For instance, an expectation of higher interest rates might impact stock prices in part because higher interest rates will raise borrowing costs for companies and tend to slow economic growth. There are a number of reasons to expect that interest rates may be higher in the future. Incipient signs of wage inflation may lead the Federal Reserve to increase its targets for interest rates in an effort to cool the economy. In addition, the recently passed tax bill will likely raise the borrowing needs of the United States government, and interest rates will rise as the government competes with private-sector borrowers for funds. But while these are reasonable explanations, no one can say for sure why stock prices first fell so much on Monday, and then recovered a large part of their losses the next day. After-the-fact commentary on large stock market movements often comes from commentators who offer an excessive sense of certainty about their views, particularly when it comes to short-term market movements.

- “Price-earnings” (P/E) ratios, one measure of how “expensive” stocks are, are high by historical standards. Price-earnings ratios capture the relationship between the prospects of company and its current stock price. These measures are typically calculated by dividing the current stock price by some measure of recent company earnings, or by a forward-looking estimate of company earnings. A P/E ratio might rise because of good news about companies’ future expected earnings. P/E ratios can also be calculated for broader market indices, not just for individual companies. Market-wide P/E ratios today are high by historical standards, exceeding their values during any historical episodes other than the period just before the 1929 market crash and during the technology boom of the early 2000s. The two previous occasions during which P/E ratios have been as high as they are today have eventually been followed by stock market declines. However, during the dot-com boom, before they fell back market-wide, P/E ratios reached levels that are significantly higher than what we are observing today.

What this Means:

Stock markets are extremely useful for allocating capital to companies with investment opportunities, and for giving households tools for investing their money. But it is important to realize that the stock market, while it serves the economy, is not the entire economy. Positive developments for companies that contribute to higher stock prices may even have some costs from a societal perspective — a hypothetical example might be a change in regulatory posture that lowered production costs but led to greater pollution. Moderate declines in stock price indexes are not a catastrophe and do not indicate an imminent downturn or recession. While stock prices are important, the extreme level of focus on the minute-to-minute performance of the stock market comes, at least in part, because these measures are available at a minute-to-minute frequency. Other measures of economic performance, for example unemployment, inflation, and national income, are only available at lower frequency. While these measures don’t seem to provide the same visceral stimulation as watching stock prices fluctuate at high frequency, they are equally important indicators of how our economy is doing.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.