Government Budget Deficits and Economic Growth (UPDATE)

Fletcher School, Tufts University

The Issue:

The Congressional Budget Office (CBO) projects that the United States Government Budget deficit will be $1 trillion in 2020, which would represent 4.6 percent of Gross Domestic Product (GDP). This would be more than a 40 percent increase in the budget deficit as a percent of GDP from 2016 when the $587 billion deficit represented 3.2 percent of that year’s GDP. One striking aspect of this large increase in the deficit is that it has occurred during a time of low unemployment and moderate GDP growth; typically, deficits tend to decrease during periods like this because of increased tax revenues and lower spending on social safety net programs. Furthermore, the CBO forecasts that the budget deficit will average more than 5 percent of GDP in the last three years of this decade. In contrast, the Trump Administration forecasts the budget deficit being 1.5 percent of GDP in 2028 and 0.6 percent of GDP in 2029.

Why are the administration's and the CBO's budget deficit projections so different? And, why does it matter?

The Facts:

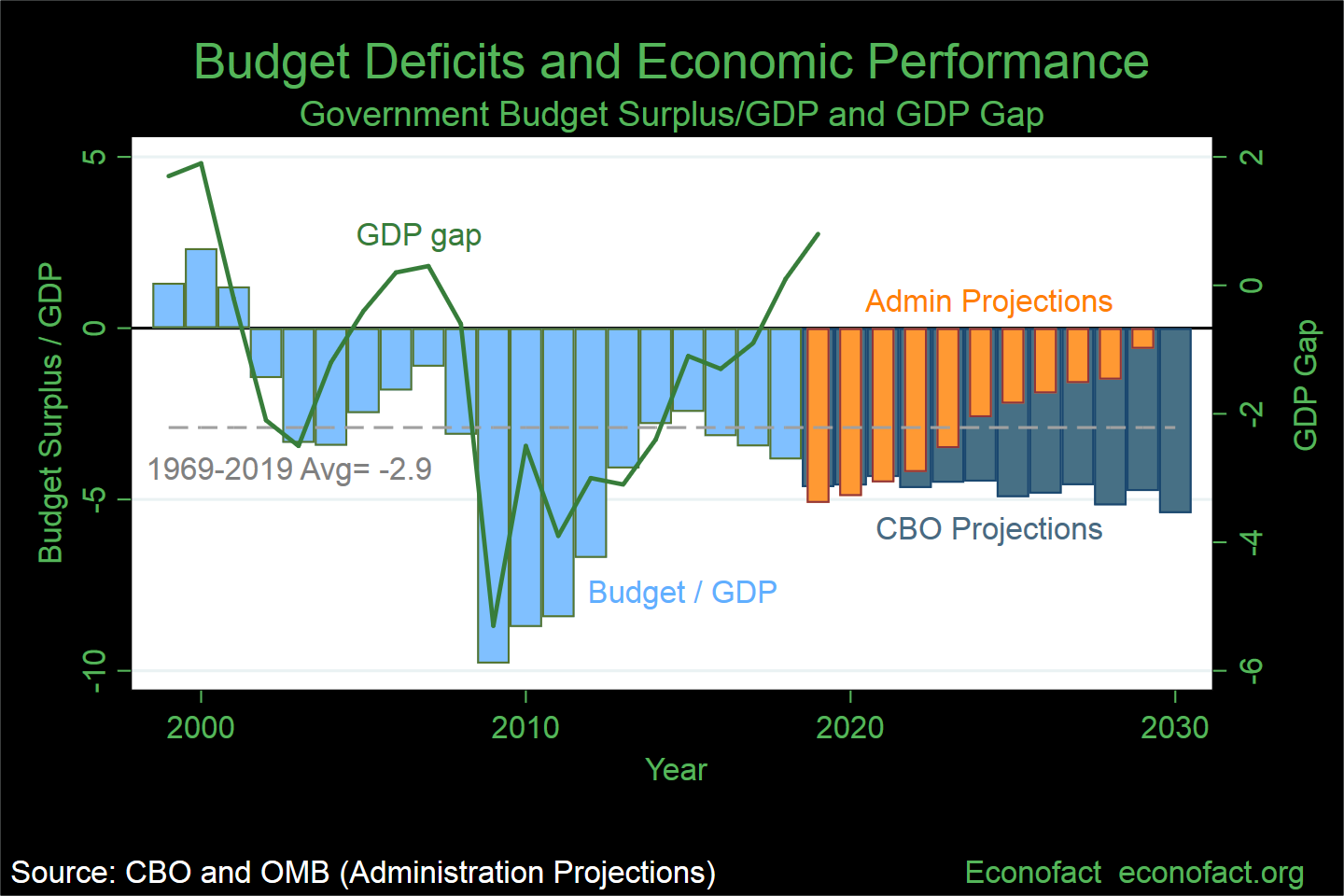

- In any given year, the difference between federal tax receipts and federal spending, including spending on servicing the outstanding federal debt, determines whether the U.S. Government has a budget deficit or a budget surplus. Over the past 50 years, the U.S. federal government has run budget deficits every single year with the exception of five years — once in the late 1960s and during four years beginning in the late 1990s — such that the deficit averaged 2.9 percent of GDP between 1969 and 2018. The light blue bars in the chart represent the budget surplus (positive values) or deficit (negative values) as a percent of GDP between 1999 and 2018, the last year for which the actual deficit value is currently available.

- The size of the federal budget deficit is tightly linked to how well the U.S. economy is performing. When the economy grows at a faster rate this raises tax revenues and tends to lower spending on social safety net programs (since fewer people need these programs when the economy is doing well). Therefore, faster GDP growth reduces the budget deficit, even with no change in underlying economic policies. This works in reverse, too; during a recession, the budget deficit increases, even with no change in underlying economic policies. However, governments might also implement additional policies in recessions aimed at combating the economic downturn that would lead to increases in the budget deficit. For example, in response to the Great Recession that began in Autumn 2008, the most severe economic downturn in the United States since the Great Depression of the 1930s, the American Recovery and Reinvestment Act (ARRA) of 2009 included federal tax cuts, increases in spending on education, health care and infrastructure, and an expansion of social welfare programs, including unemployment benefits, that were worth $787 billion. Subsequently, the budget deficit averaged 8.1 percent of GDP between 2009 and 2012, reflecting both the Great Recession and the policy responses to that downturn. To illustrate the relationship between the federal budget deficit and the performance of the economy we use the GDP Gap in the chart, which is the difference between actual GDP and what GDP would be if the economy were operating at full capacity. In the period from 1999 to 2016, as the GDP gap became more negative, the budget deficit got larger, and vice versa (see chart). But this relationship does not hold for 2018 and 2019 when the economy was strong and yet the budget deficit also increased. The likely reason for this is the change in tax policy with the Tax Cut and Jobs Act, which went into effect at the beginning of 2018 as well as, to some extent, an increase in spending.

- Because of the close link between economic growth and fiscal health, projections of the federal government's fiscal balance depend critically on projections of the economy’s performance. Widely different forecasts of the economy's expected rate of growth underlie an important part of the differences in the budget deficit forecasts by the Trump administration (orange bars in the chart), the CBO forecast (the dark blue bars in the chart) and other forecasts. The administration's view is based partly on the assumption that the United States will average GDP growth of 2.9 percent through the 2020s. In contrast, the CBO projections are based on an assumed average economic growth rate of 1.7 percent in the years 2020 to 2029. Also, by statute, the CBO budget forecast must assume the maintenance of current laws. An alternative estimate that uses the CBO’s economic growth forecasts but assumes tax cuts that are set to expire will rather be continued (a so-called current-policy assumption rather than the CBO’s current-law assumption by Alan Auerbach and Bill Gale results in bigger budget deficits than the current law estimates in each year after 2018, with the deficit rising to 6.2 percent in 2029 (as opposed to the CBO current-law forecast of 4.5 percent and the Administration forecast of 0.6 percent).

- An ongoing growth rate of almost 3 percent over the coming decade is at odds with other forecasts and analyses of likely United States GDP growth. Higher rates of growth would lead to lower deficits, but there are reasons to think that the rates of growth will not be high enough to bring down the deficit-to-GDP ratio. The International Monetary Fund predicted a 1.7 percent growth rate in the five years 2020 to 2024 in its Article IV report on the United States (published in June 2019),stating “medium-term risks are growing,” citing financial vulnerabilities, ongoing trade disputes and the unsustainable path of government debt. Much faster growth on a sustained basis would require either large increases in the growth of the labor force or in worker productivity, or some combination of the two (see here). Thus it is unlikely that high GDP growth will save the economy from rising government budget deficits.

What this Means:

Large government budget deficits may be warranted at times when the economy is in a downturn, like during the Great Recession that began in 2008, in order to stimulate spending and mitigate economic weakness. But large deficits that occur when the economy is at or near its full-capacity raise concerns of increasing costs of borrowing, reduced private capital formation, and potential financial and economic destabilization. Deficits can shrink with strong economic growth, but the combination of likely policies and plausible GDP growth rates for the United States point towards rising deficits over the next decade. As Bill Gale points out, a period of relative economic prosperity is when policymakers should address fiscal imbalances and the longer we wait to do so, the more difficult and more disruptive the eventual needed correction.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.