Are Growing Federal Budget Deficits and Debt Cause for Concern?

Brookings Institution

The Issue:

Over the next ten years, the United States is on course for routine trillion-dollar annual deficits in the federal budget and the highest debt-to-GDP ratio in its history. Beyond the next decade, large and rising projected annual deficits will push the national debt steadily upwards, reaching almost 200 percent of GDP by 2049 (up from 78 percent today) under plausible scenarios. The projections derive from rising spending on health care, Social Security, and interest payments and, as of yet, an unwillingness either to reduce such outlays or provide the revenues needed to finance them. The projections assume steady economic growth and relatively low interest rates, so they could be far worse under alternative scenarios. What are the implications?

Current debt projections are different from previous high-debt episodes in U.S. history, which occurred mainly during wars or Depressions.

The Facts:

- Making a budget projection is both an art and a science. The Congressional Budget Office (CBO) provides the basic budget projections. But CBO is required by law to make certain assumptions that reflect “current law,” namely that expiring tax provisions are not extended, that mandatory programs are reauthorized as scheduled, and that discretionary spending follows the caps set forth in previous legislation. These assumptions may be unrealistic. In a recent paper, Alan Auerbach, Aaron Krupkin, and I construct “shadow budgets,” adjusting CBO’s figures. These adjustments are not policy recommendations; they simply show the effects of what we view as a more realistic version of “business as usual,” or “current policy.” We assume that major temporary tax-cut provisions (like those in the 2017 Tax Cuts and Jobs Act) are made permanent and that enacted tax rules whose implementation has been postponed twice (such as the “Cadillac tax” on employer-sponsored health insurance that was part of the Affordable Care Act) will never take effect. On the spending side, we assume a budget that allows for the continuation of current services. We allow defense spending to rise with inflation and non-defense discretionary spending (which funds programs ranging from medical care for veterans, to scientific research at the National Institutes of Health, to the National Highway System and aviation safety, among others) to rise with inflation and population growth. Under these "current policy" assumptions federal government deficits would rise from 4.2 percent of GDP in 2019 to 7.0 percent of GDP by 2029. To put that in perspective, since World War II, the only time deficits exceeded even 6 percent of GDP was in 2009-2012, during and after the Great Recession.

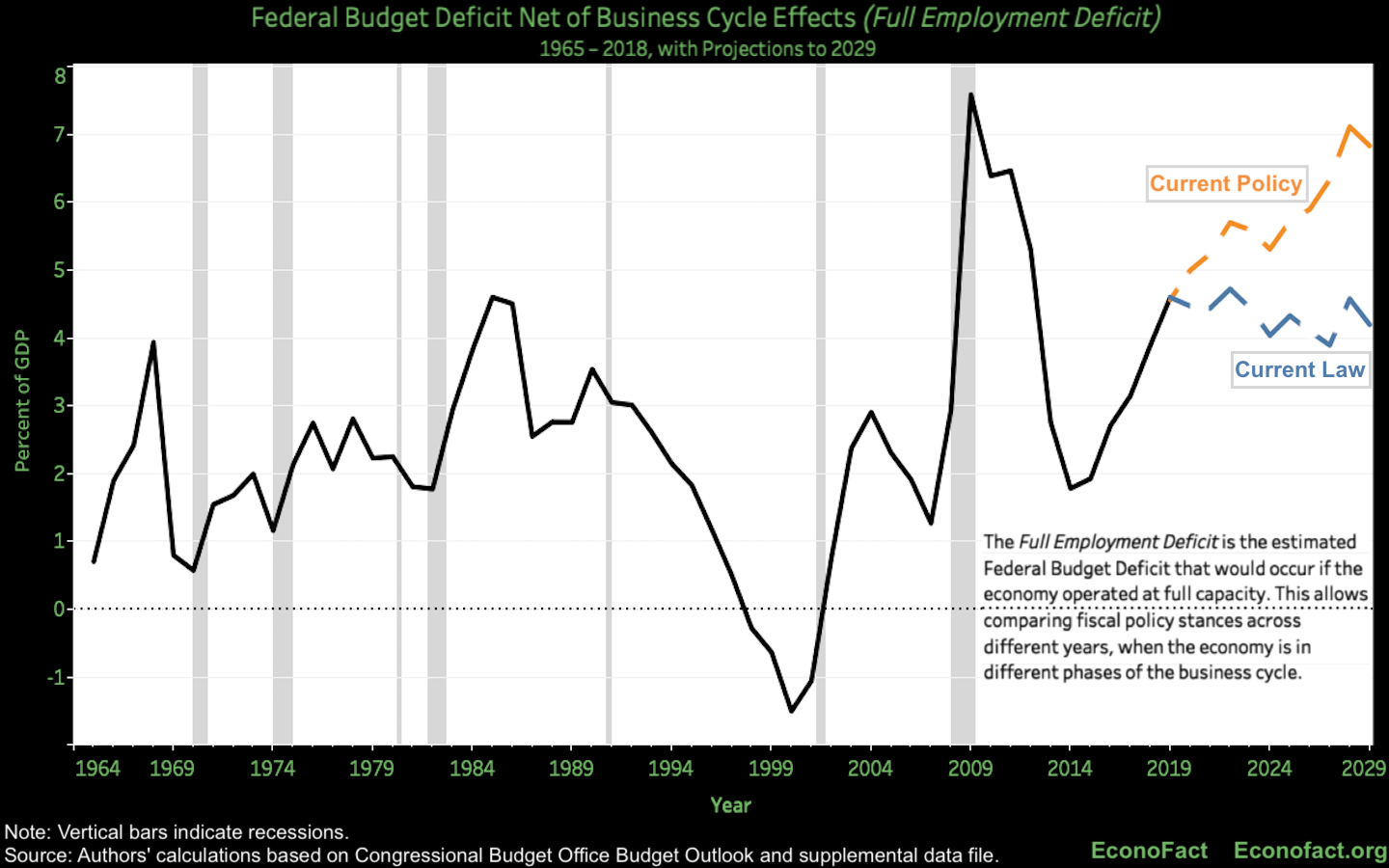

- Examining the full-employment deficit shows how imbalanced current policy is. The full-employment deficit measures the size of the budget shortfall if the economy were at full employment. It is a convenient way to gauge the fiscal stance across different years, when the economy is at different stages of the business cycle. (The government's deficit automatically widens during recessions, as tax receipts fall and social expenditures such as unemployment insurance rise without any change in policy.) The average full-employment deficit between 1965 and 2018 was just 2.7 percent of GDP. In contrast the full-employment deficit is projected to rise to a steady 4 percent of GDP under the CBO's current law assumptions. As the top chart shows, this would be the first time in history that the U.S. maintained persistent, sizable full-employment deficits. Even worse, under our current policy assumptions, the full-employment deficit would rise to 7 percent of GDP by 2029.

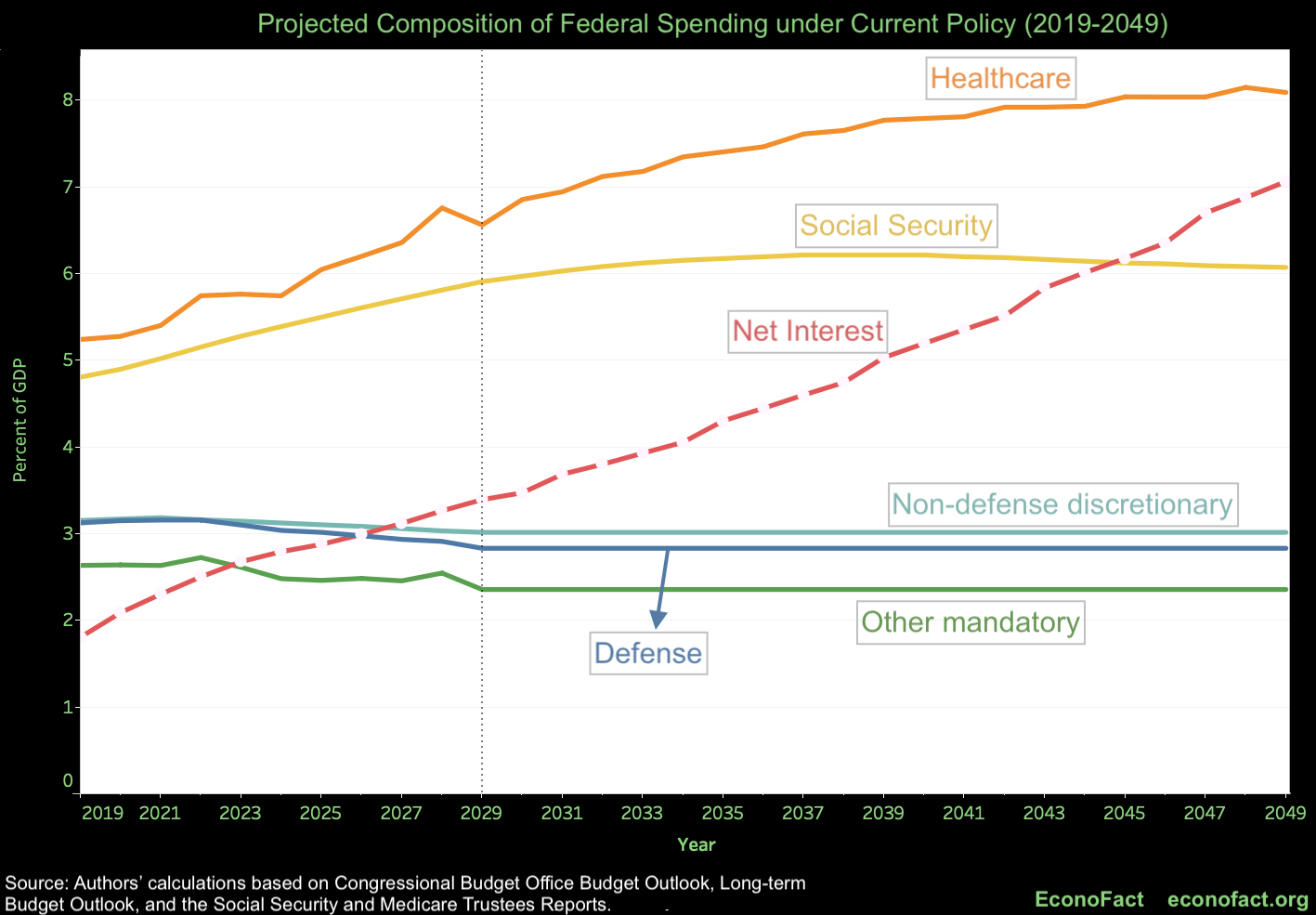

- Looking only at the next ten years gives an incomplete and overly optimistic picture of the fiscal outlook, even with current policy adjustments. Looking beyond 2029, we expect deficits to grow steadily as a share of the economy (see Figure 1, here). We use data on Medicare and Social Security from the respective programs’ Trustees’ reports, and data on GDP, interest rates, and other healthcare spending from CBO for longer-term projections. The projections embody significant changes in the composition of government spending, with outlays on healthcare, Social Security, and interest payments on the debt rising as a share of the economy.

- If they occur as projected, the high annual federal deficits will add up, increasing the country's national debt to historically high levels. Debt rises from 78 percent of GDP in 2019 to 93 percent of GDP in 2029 under the CBO's "current law" projections and 106 percent under "current policy" assumptions. This would be the highest ratio in U.S. history. And it would continue to climb, rising to 193 percent under "current policy" by 2049.

- The fiscal gap is substantial. To ensure the debt-to-GDP ratio 30 years from now does not exceed the current level would require a combination of immediate and permanent spending cuts and/or tax increases totaling 3.9 percent of GDP. In 2019, this would be equivalent to a 21 percent cut in non-interest spending, a 47 percent increase in income tax revenues, or a 24 percent increase in all tax revenues.

- The debt projections are different from previous high-debt episodes in U.S. history, which occurred mainly during wars or Depressions. In such episodes – the Civil War, World War I, and World War II – the debt-to-GDP ratio was cut in half roughly 10 to 15 years after the war ended. In the projections, however, the nation faces a built-in chronic imbalance between revenues and spending, due in considerable part to the aging of the population, rather than a temporary spike in spending due to a war or a temporary decline in revenue due to a Depression.

- Growth in annual net interest payments – largely due to projections of rising interest rates – accounts for a significant part of the rising debt projection. However, even if interest rates remain unchanged over the next 30 years, the debt-to-GDP ratio in 2049 would rise to 156 percent. That is, there is a significant fiscal imbalance even if interest rates stay low.

- Large deficits and accumulated debt can leave the U.S. in a weaker position to handle future shocks. Sustained deficits and rising long-term debt can make it more difficult to garner political support to conduct routine policy, address major new priorities, or deal with the next recession, war, or emergency. In addition, the fiscal trajectory raises the possibility of a financial crisis, even if such an outcome remains a low-probability event.

- There is renewed discussion among economists about the use of fiscal policy and expansion of public debt when interest rates are low. Olivier Blanchard, former chief economist at the International Monetary Fund, argued in a recent, highly-publicized article, that if the interest rate on government debt is smaller than the growth rate of the economy — and if primary deficits (excluding interest payments) are small — the government can roll over debt and still have the debt-to-GDP ratio stay constant or fall. Under those circumstances, there is no need to raise taxes or cut spending in order to sustain a given debt level (though the impact of higher debt on the economy may nonetheless provide a reason to cut debt – as discussed below). However, this scenario does not completely describe the current U.S. situation (see this Financial Times Alphachat podcast). Despite the fact that interest rates are low, the debt-to-GDP ratio is projected to rise inexorably in the future, because projected primary deficits are large and persistent, even if the economy stays strong and even if the interest rate remains below the growth rate of the economy (as noted above).

What this Means:

Not all debt is bad. When it finances government investment or anti-recession efforts, increased debt can boost the economy in the short-term and the long-term. But the debts we are accumulating do not involve these priorities. Indeed, federal investment in infrastructure and human capital is slated to decline as a share of GDP. As a result, the current level of government borrowing will likely reduce future national income.

One of the arguments for more debt and less austerity during the Great Recession and the aftermath was embodied in Keynes’s famous quote, “The boom, not the slump, is the right time for austerity at the Treasury.” Well, this is the boom. If the future deficit path looked favorable, i.e., if our current primary deficits were thought to be temporary, the argument for simply letting them evolve would be stronger. But if policymakers do not address the fiscal imbalance now, it will only become a harder problem in the future, due both to the growing size of the problem and the increased economic costs and political difficulty of enacting spending cuts or tax increases in less favorable times. Addressing the fiscal imbalance now does not require sharp, immediate spending cuts or tax increases. Rather, the changes should be phased in over time. Nevertheless, the longer we wait to act, the larger and more disruptive the eventual policy solutions will need to be.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.