Welfare and the Federal Budget

University of Maryland

The Issue:

As the Trump administration has been preparing a federal budget and Congress has been talking about tax reform, there has been much attention to the federal budget and federal government spending priorities. One notion that has surfaced in the surrounding political discourse is that the federal government ought to spend less on welfare assistance to low-income individuals to both reduce government spending and to promote economic self-sufficiency. Critics have pointed at traditional transfer programs such as the Temporary Assistance to Needy Families and the Supplemental Nutritional Assistance Program. However, especially since the changes brought in by welfare reform in the mid-1990s, federal transfer programs provide very little aid by way of cash assistance to non-working adults. At the same time, social insurance programs including Disability Insurance have been relatively at the margin of reform debates. Yet social insurance programs are a much larger share of the federal budget and have been seeing steady increases in the populations they serve, potentially having negative impacts on employment.

How much does the federal government spend on welfare assistance to low-income individuals? What are the existing eligibility criteria to qualify for these programs? And, what evidence is there for negative employment impacts of these programs?

Since welfare reform in the mid-1990s, federal transfer programs provide very little aid by way of cash assistance to non-working adults.

The Facts:

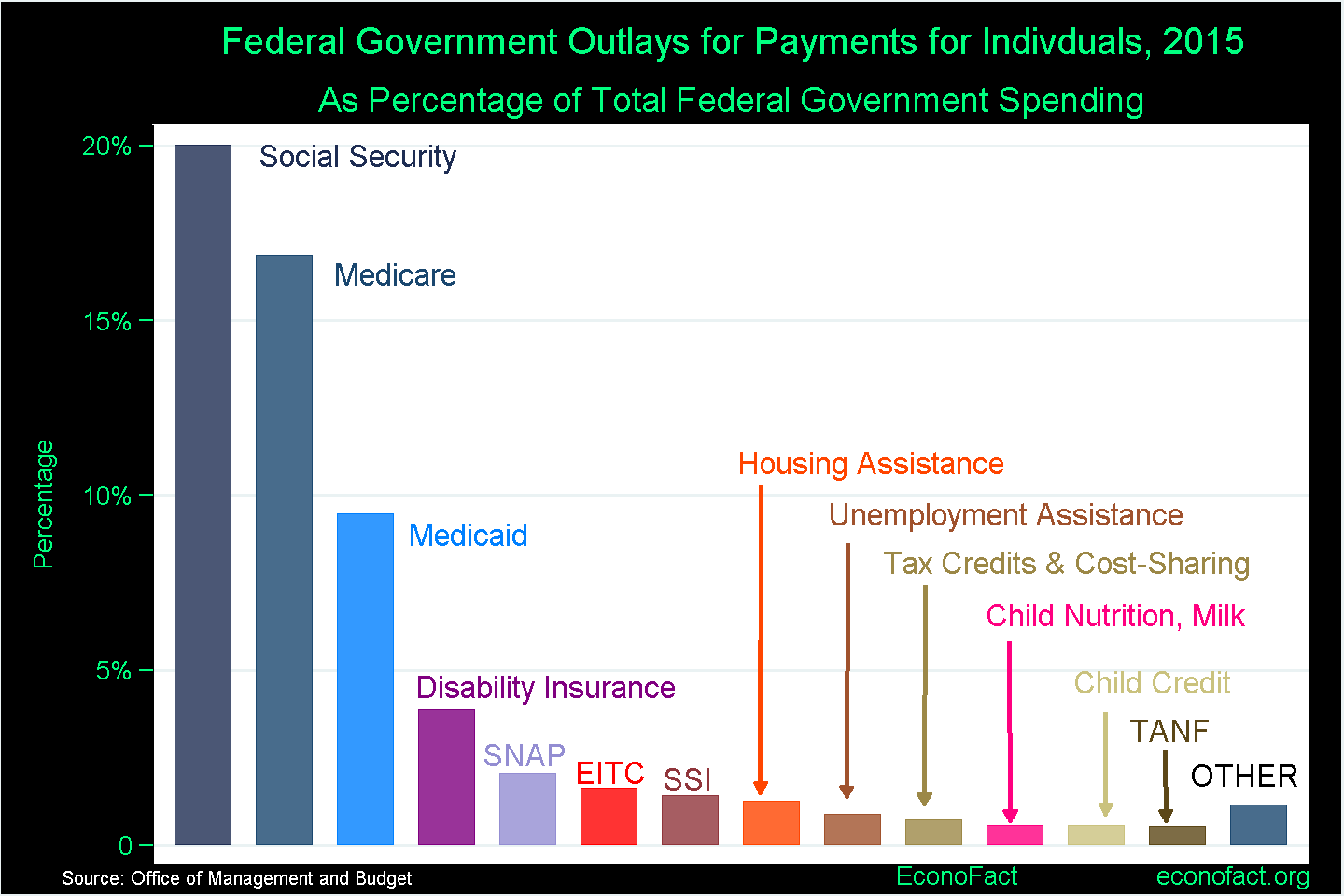

- Spending on cash and near-cash transfer programs to low-income families comprises less than 5 percent of the federal budget. These programs are not drivers of increased government spending (see chart). The program that most closely aligns with the conventional notion of “welfare” in the sense of providing cash income to low-income families – is the Temporary Assistance to Needy Families (TANF) program. In 2015 spending on TANF amounted to 0.54 percent of total federal outlays, amounting to $19.9 billion. In comparison, payments of tax refunds through the Earned Income Tax Credit (EITC) – a cash payment that is only paid to tax filers with low, but positive earnings –amounted to $60.1 billion, 1.63 percent of federal outlays the same year. Spending on income assistance programs to low-income families is dwarfed by spending on social insurance payments to the elderly through the Social Security and Medicare programs.

- TANF is not welfare in the traditional sense of unrestricted cash payments to non-working individuals. The program is time-limited and imposes work requirements on beneficiaries. TANF was implemented as part of the 1996 welfare reform legislation that effectively “ended welfare as we know it” by eliminating the former Aid to Families with Dependent Children program (AFDC). In 2017, an estimated 2.6 million individuals were receiving TANF benefits per month. Like AFDC, eligibility for cash payments from TANF is limited to children and adults with child dependents. Unlike AFDC, TANF is not an entitlement program and has strict work requirements and time limits. Federal rules impose a lifetime limit of 60 months of TANF receipt for a family with an adult recipient, and some states have stricter time limits. Current rules also require that 50 percent of adult TANF recipients in a state must participate in specified work activities. Exempt individuals typically include the elderly, the ill or incapacitated, and expectant mothers in their third trimester (see this report for TANF work requirements). Currently, only one-third of TANF spending is on cash assistance. The federal government pays TANF funds to states primarily through a fixed block grant and states have flexibility in determining how much of their TANF funds are paid out to families as cash assistance or used for other types of assistance, such as child care or transportation subsidies, refundable state EITC payment, work supports, etc. Benefit amounts vary widely across states, with the median maximum monthly benefit for a family of three in 2012 being $427. Numerous academic studies have investigated the caseload and employment effects of the shift that happened as part of the 1996 welfare reform legislation. The consensus finding from this literature is that the shift from AFDC to TANF led to higher employment rates among the target population of single-mothers. (See here for a detailed review of TANF and academic evidence on program effects.)

- The Supplemental Nutritional Assistance Program (SNAP), which is one of the nation's largest anti-poverty programs, offers limited assistance to non-working able-bodied individuals without dependents. In 2015 the federal government spent $76.1 billion on SNAP, slightly more than 2 percent of total federal outlays, providing food vouchers to an average of 45.8 million individuals a month. Average monthly benefits per person in 2015 were $126.81 (data available through the U.S. Department of Agriculture see here for the most recent summary table). SNAP, formerly known as "Food Stamps", has come under a great deal of scrutiny, with critics viewing the relatively high (by historical standards) SNAP caseload as evidence of bloated welfare spending. Though SNAP benefits take the form of food vouchers rather than cash, SNAP is a crucial income support program, in part because it is the only income support program not categorically restricted to certain groups of individuals. SNAP eligibility rules are quite restrictive for non-working prime-age (18 to 49 years old) able-bodied adults without dependents (ABAWDs). Most are restricted to three months of benefits within a three-year period if they are not working or in a training program at least 20 hours per week. This feature of the program is essentially tantamount to a work requirement for childless adults (see here for a thorough review of SNAP and research on its effects). By statute, the time limits imposed on non-working ABAWDs are relaxed during periods when unemployment in a state is high, as was the case in most states during the Great Recession. There is no compelling evidence that SNAP outlays lead to a sizable reduction in employment rates, in particular among men. (See here for detailed employment impacts of the introduction of the food stamp program in the early 1960s and 1970s.) Because the program responds to changes in the economy, spending on SNAP increased significantly during the Great Recession but has been decreasing as the economy has been improving.

- Although they are not typically considered welfare programs, the Social Security Disability Insurance (SSDI) program and the Supplementary Security Income (SSI) program are major sources of income assistance in the U.S. Both are social insurance programs administered through the Social Security Administration and they have seen sizable increases in their beneficiary populations over recent decades.

- The federal government had SSI program outlays of $52.3 billion in 2015 – comprising 1.42 percent of federal outlays – providing federal benefits to 9.03 million people. (For data see Tables 1, 2, and 3 here). The maximum monthly federal benefit amount was $733 for an eligible individual. SSI essentially operates three programs for distinct populations: blind or disabled children, blind or disabled non-elderly adults with limited earnings history, and individuals 65 and older (without regard for disability status). Approximately one-in-six SSI recipients are under the age of 18, one-in-four are 65 or older, and the remaining 60 percent are between the ages of 18 and 64. The fraction of non-elderly adults receiving SSI benefits has increased substantially over time, from 1.5 percent in 1988 to 2.5 percent by 2013 (see here for details).

- Does the SSI program lead to lower rates of employment among beneficiaries and their family members? The design of the SSI program potentially discourages labor supply among non-elderly recipients by requiring a medical disability diagnosis and low levels of earnings. To the best of my knowledge, there is no evidence of sizable dis-employment effects of the SSI program on working age adults (see this review I co-authored for an overview of the program and a review of research on its effects). This is not surprising, as non-elderly adults who participate in SSI have very low pre-program employment rates. There is a separate issue of whether the SSI program for children reduces parental employment. Rigorous evidence suggests that the removal of a child’s benefits leads to a sizable increase in parental earnings. A related study shows that child recipients who themselves are removed at age 18 are not readily able to transition into stable employment as young adults. Though SSI spending is a relatively small share of the federal budget, given the potential dis-employment effects of the SSI children’s program, both for parents of SSI child beneficiaries and children transitioning off the program as adults, there is justification to consider a re-evaluation of the design of the SSI children’s program.

- The federal Social Security Disability Insurance (SSDI) program paid out $143 billion in cash payments to 8.91 million beneficiaries in 2015, according to data from the Social Security Administration. Spending on SSDI accounts for 3.89 percent of the federal budget, making it the only cash assistance program other than Social Security Old Age and Survivors Insurance (the Social Security retirement program) that comprises more than 2 percent of the federal budget. SSDI replaces the lost earnings of qualifying individuals with significant work histories. Medical eligibility for the program requires a disability diagnosis, defined by the SSA as “the inability to engage in substantial gainful activity because of a medically determinable physical or mental impairment that is expected to last at least 12 months or result in death.” By definition, the program is designed for long-term receipt, and in practice, very few beneficiaries exit the program for a reason other than death. (Only about 1 percent of beneficiaries are removed from the rolls based on health improvements, according to this study.) DI benefit amounts are determined as a function of prior earnings using the same formula as is used for Social Security retirement benefits. The wage replacement rate is 90 percent of the first $826 dollars of prior monthly earnings, 32 percent of monthly earnings between $826 and $4,980, and 15 percent of monthly earnings above $4,980. The average monthly cash benefit amount for a disabled worker was $1,165 in 2015. In addition, DI beneficiaries automatically qualify for Medicare benefits, making the total transfer amount much higher.

- Does the SSDI program lead to lower rates of employment among beneficiaries and their family members? The share of working-age Americans receiving SSDI benefits has increased significantly, rising from 2.2 percent in the late 1970s to 3.6 percent in the years immediately preceding the 2007–2009 recession and 4.6 percent in 2013 (see here for an analysis of this increase). There has been a corresponding change in the composition of DI recipients, with more recipients claiming benefits for hard-to-verify impairments such as mental conditions and back pain, and with the program providing a safety net backdrop for low-skilled workers with weakened economic prospects (see here). Researchers attribute the tremendous growth in the DI caseload to a combination of policy, economic, and demographic factors. There is compelling evidence that the existence and current benefit structure of the DI program have caused some individuals with weak labor force attachment to work at lower rates than would otherwise be the case (see for instance here, here, here, and here).

What this Means:

If policymakers have dual goals of reducing federal government spending and reducing cash support for non-working individuals to increase employment rates, a focus on welfare programs that provide income support to low-income families is misplaced. Those programs constitute a tiny share of federal spending and already have stringent work requirements. Instead, policymakers should focus on social insurance programs, namely, reforming the Social Security Disability Insurance program, which is by far the largest source of cash assistance to non-working, non-elderly individuals and comprises 3.9 percent of the federal budget. Well-designed reform of the SSDI program could have both a substantial positive fiscal impact on the federal budget as well as the economic self-sufficiency of individuals currently served by the program.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.