The University Endowment Income Tax: Who Will Pay it and Why Was it Implemented?

Wellesley College

The Issue:

The recently enacted federal tax legislation levies a tax on the endowment income of colleges and universities with large endowments. The schools that will likely be covered by the new provision have large sticker prices and low- and middle-income students tend to be underrepresented in their student bodies. Tom Reed, a Republican congressman from New York, argues the tax will address these issues, promoting “a good-quality education with an affordable price tag” at affected colleges and universities. The schools likely to be affected, though, already have generous financial aid policies and are unlikely to reduce their sticker price as a result. The tax also generates limited revenue, offsetting little of the other tax cuts introduced by the law. This raises the issue of what the tax actually accomplishes.The schools likely to be affected already have generous financial aid policies and are unlikely to reduce their sticker price as a result.

The Facts:

-

- The endowment income tax imposes a tax of 1.4 percent of the net investment income of institutions of 500 or more full-time equivalent students with large endowments. The bill specifies that the tax will be imposed on colleges and universities whose “aggregate fair market value of the assets of which at the end of the preceding taxable year (other than those assets which are used directly in carrying out the institution’s exempt purpose) is at least $500,000 per student of the institution.” The parenthetical statement is critical in determining who will pay the tax, but it is far from clear. Institutions will need to wait for guidance from the IRS before knowing for sure what their status is. Also, not adjusting the $500,000 for inflation means that more institutions will be subject to the tax over time.

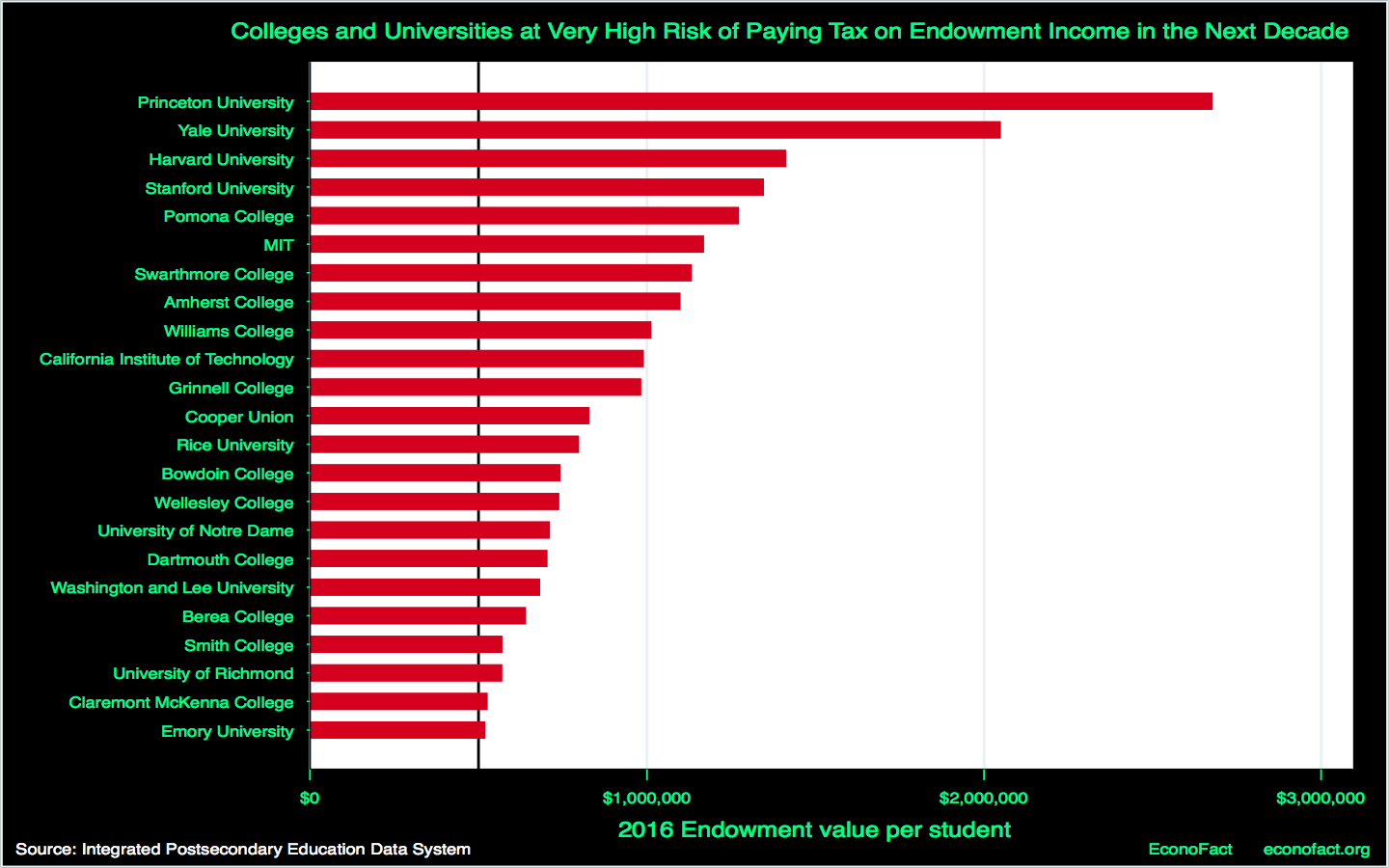

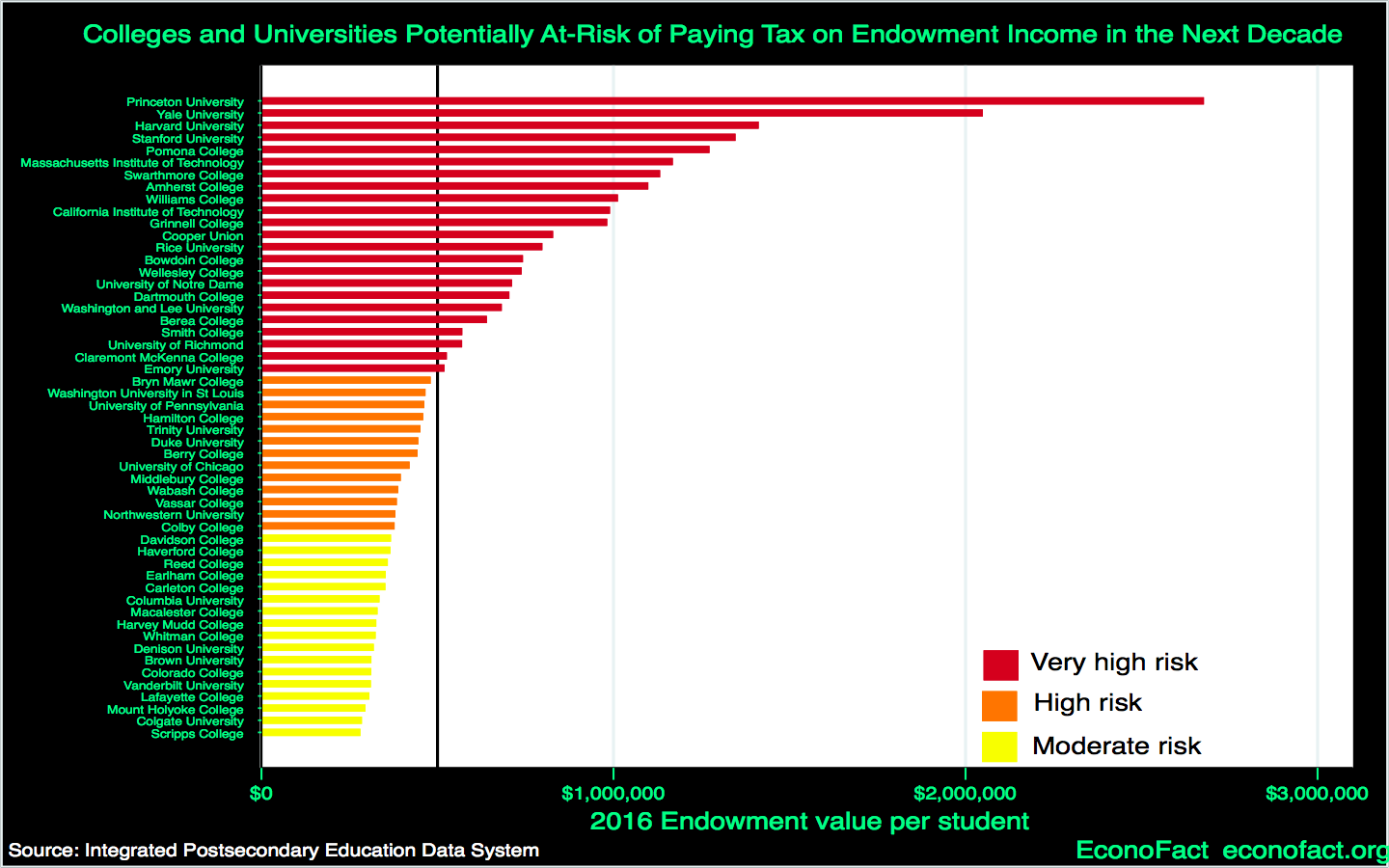

- The ambiguity of the bill means that it is impossible to accurately determine which colleges and universities will pay the tax now and, say, over the next decade. But with a few assumptions, one can get an idea of those that are at-risk of paying the tax (see chart). I used IPEDS (Integrated Post-Secondary Education Data System) data on endowment values at the end of the 2015-16 academic year (the most recent available) and assumed that the entire amount “counts” towards the cut-off. I also assumed a 6 percent rate of growth in endowment values over time (which incorporates investment return, spending from the endowment, and new gifts), which approximates the historical average over the past two decades. This enables me to gauge colleges’ and universities’ “risk status” of paying the tax. Those that are at “very high risk” are already over the $500,000 per student threshold (where full-time students are counted individually and part-time students are counted as half). These institutions only avoid the tax if they are able to disqualify potentially large parts of their endowment based on the ambiguous provision. High risk schools are defined as those whose simulated endowment values over the next five years, and moderate risk schools those whose simulated endowment exceed the threshold over ten years.

- Fifty-three institutions are at moderate or greater risk of paying the endowment income tax in the next decade. Princeton and Yale lead the pack with a value of endowment per student over $2 million (over four times the legislated threshold). Twenty-one additional institutions fall over the $500,000 threshold “now” (as of June 2016), placing them at very high risk. Thirteen more fall into the high risk category and an additional 17 face moderate risk. Scripps College, with 1,000 students and a current endowment of $300 million (current endowment per student of $300,000), is the last institution forecasted to fall into the moderate risk category. (Click here for a full listing of schools that includes those at high and moderate risk of being subject to the tax over the next decade).

- I have argued elsewhere that the law’s stated rationale of encouraging schools to lower their prices and offer more generous aid misrepresents the pricing systems used at the affected colleges. The affected schools’ “sticker price” of upwards of $70,000 is clearly unaffordable for many, if not most, students and their families. But those charges are only faced by those who receive no financial aid. Each of these schools base the actual amount a student and his/her family pay according to their financial resources. The goal is to establish individualized prices that are “affordable” to each student. At these institutions, financial aid is available to students with family incomes up to, perhaps, $250,000 year, assuming typical asset holdings. Meeting full financial need is easy to say and difficult to implement in practice, but in principle, that policy satisfies the goals of access and affordability. Improving communications around that message is something that these schools need to improve, and there are efforts to make this information more available, but schools are unlikely to change their underlying pricing system as a result of this legislation.

- Another plausible rationale is to generate tax revenue that can help offset tax cuts introduced elsewhere. Yet the amount of tax that is likely to be collected is small. Using the current and forecast endowment values used in this analysis (based on the assumptions described earlier), I can also simulate tax revenue by making the initial assumption that the annual rate of return on endowment values is 8 percent (note that this represents just a part of the annual change in endowment value, assumed to be 6 percent earlier based on historical data). Alternative assumptions here would simply scale the estimates I report up or down proportionally. Based on that assumption, this tax will generate around $200 million per year now, rising to $400 million per year in a decade. Over the next decade, the tax would generate perhaps $3 billion in revenue. This would offset 0.2 percent of the $1.5 trillion in total recently enacted tax cuts, and this $3 billion represents 0.006 percent of anticipated federal government expenditures over this period.

- Across institutions, these forecasts suggest that, for example, Harvard University will pay $40 million now, rising to $70 million annually over the next decade (assuming the tax is levied on the full value of the endowment). Although it is difficult to downplay those sums for a single institution, it is also true that this represents 1 percent of Harvard’s $4.5 billion operating budget. A similar calculation at Wellesley College also generates a tax of around 1 percent of the operating budget. It is a meaningful burden on the institutions, but it is not a major one.

- It is noteworthy that the endowment income tax, like the cap on the deductibility of state and local taxes, has disproportionate effects on institutions located in states that have voted for the Democratic candidate in recent presidential elections (“blue states”). The figure below provides a common red state/blue state map that superimposes the location of the colleges and universities that are at least at a moderate risk of being affected by the tax on endowment income. Red states and blue states are determined by the results from the 2004, 2008, 2012, and 2016 Presidential elections. Bright red (blue) shading indicates the state voted for the Republican (Democratic) candidate in each of these four elections. Pale red (blue) is the same concept, but for three of the four elections. Purple states split two and two. About three-quarters (39 out of 53) affected colleges and universities are located in blue states. Only 12 are located in red states, with the remaining two institutions residing in purple states. A proposal to exempt Berea College in Kentucky would have reduced this number to 11, but it was dropped for procedural reasons.

{kind=link}

What this Means:

The effects of the endowment tax remain unclear given the ambiguity in its wording. But the likely revenues raised from this tax are minuscule when considered in the context of the overall reduction in tax receipts or the size of the federal budget. Also, the tax is unlikely to affect the sticker price of a college education or to alter financial aid offered by those institutions affected by the tax. When plausible economic justifications for a change in tax policy fail, political considerations become a more credible explanation for their enactment. This seems to be the case regarding the higher education endowment income tax.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.