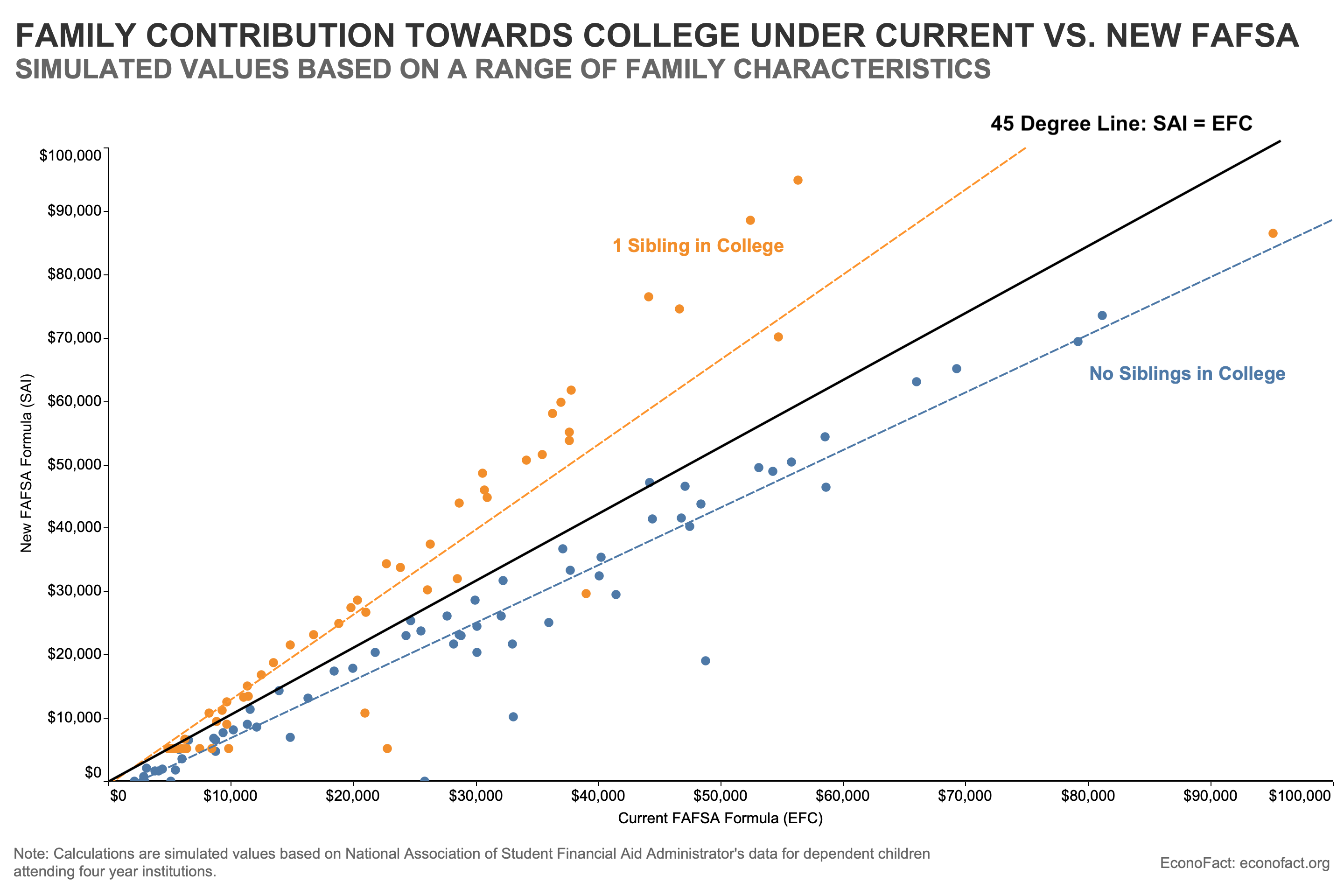

FAFSA Simplification: How New Rules Will Change the Price of College

April 18, 2023

Roughly two-thirds of students will have greater eligibility for financial aid. But some could see a sizable, unexpected increase in cost.

April 18, 2023

Roughly two-thirds of students will have greater eligibility for financial aid. But some could see a sizable, unexpected increase in cost.

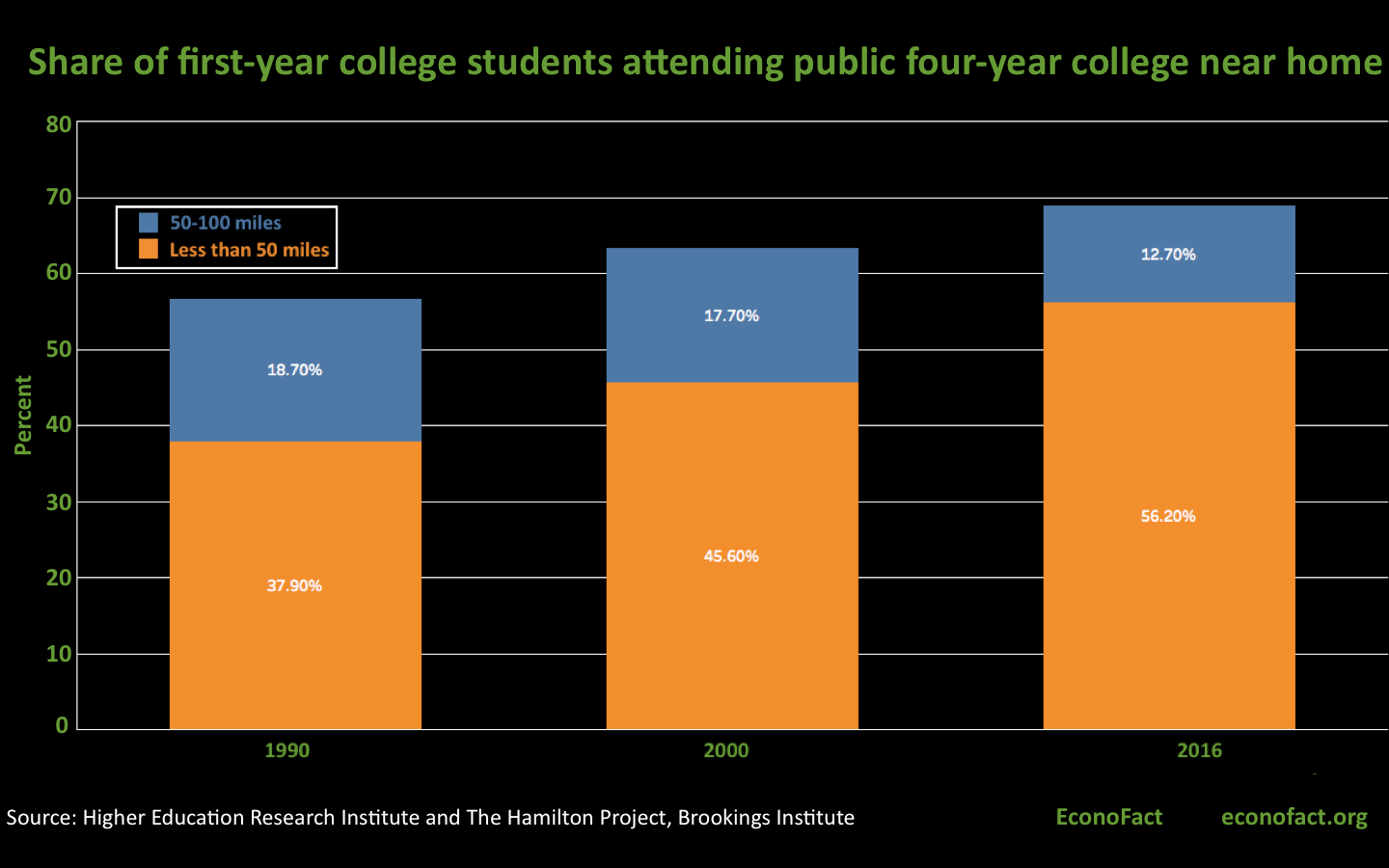

March 22, 2018

Geographic location is important in determining not just where, but whether, a high school senior goes on to college. About 1 in 6 lack a nearby college.

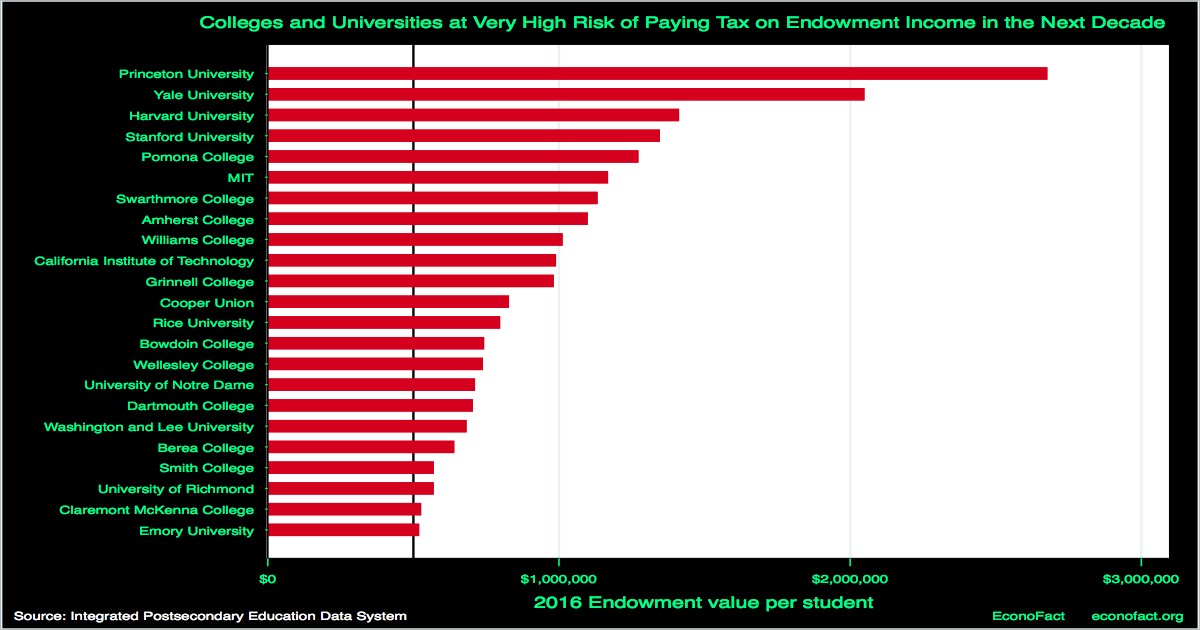

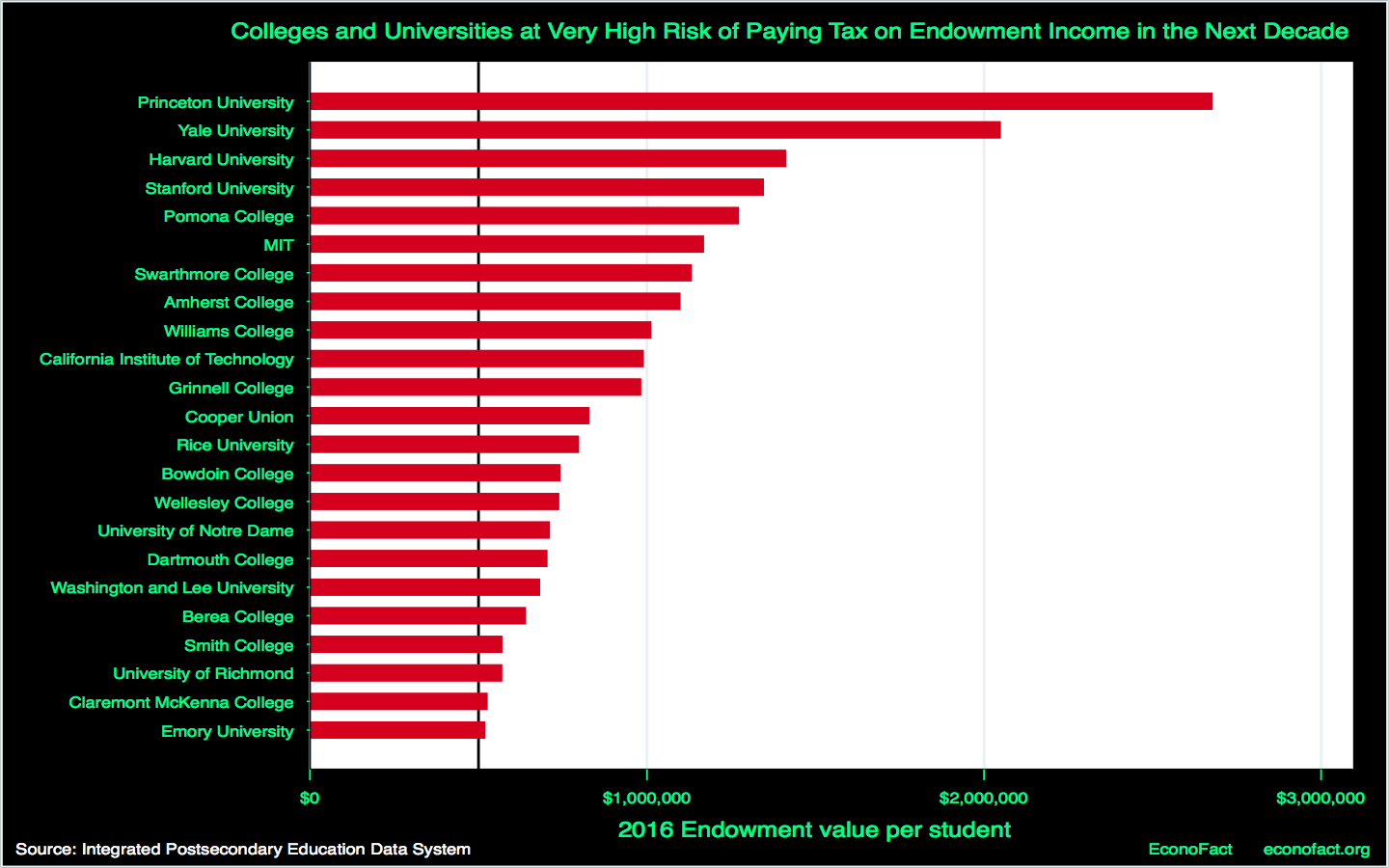

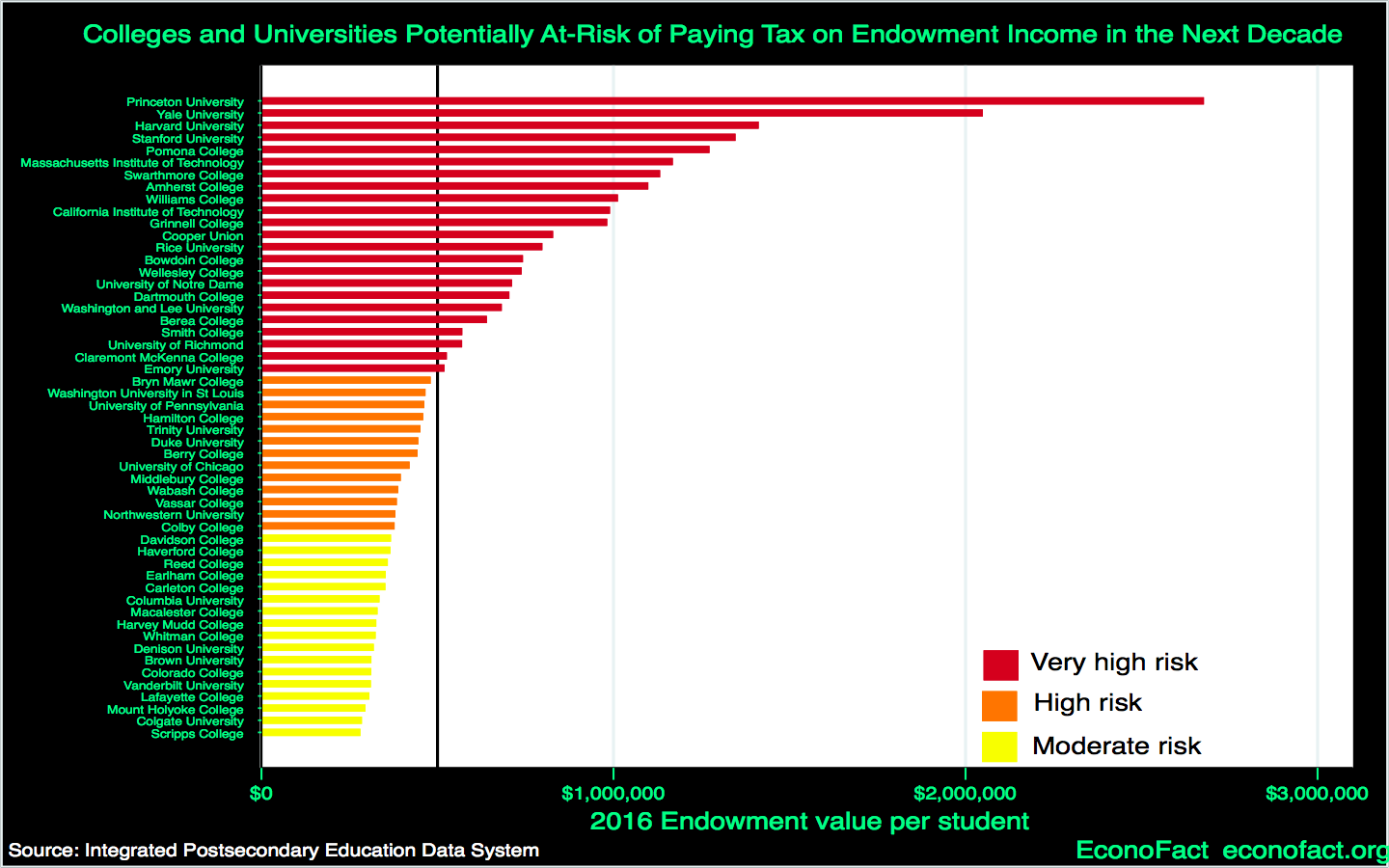

January 25, 2018

The recently enacted federal tax legislation levies a tax on the endowment income of colleges and universities with large endowments.

(This is an interactive graph. Hovering over the dots reveals institution names.)

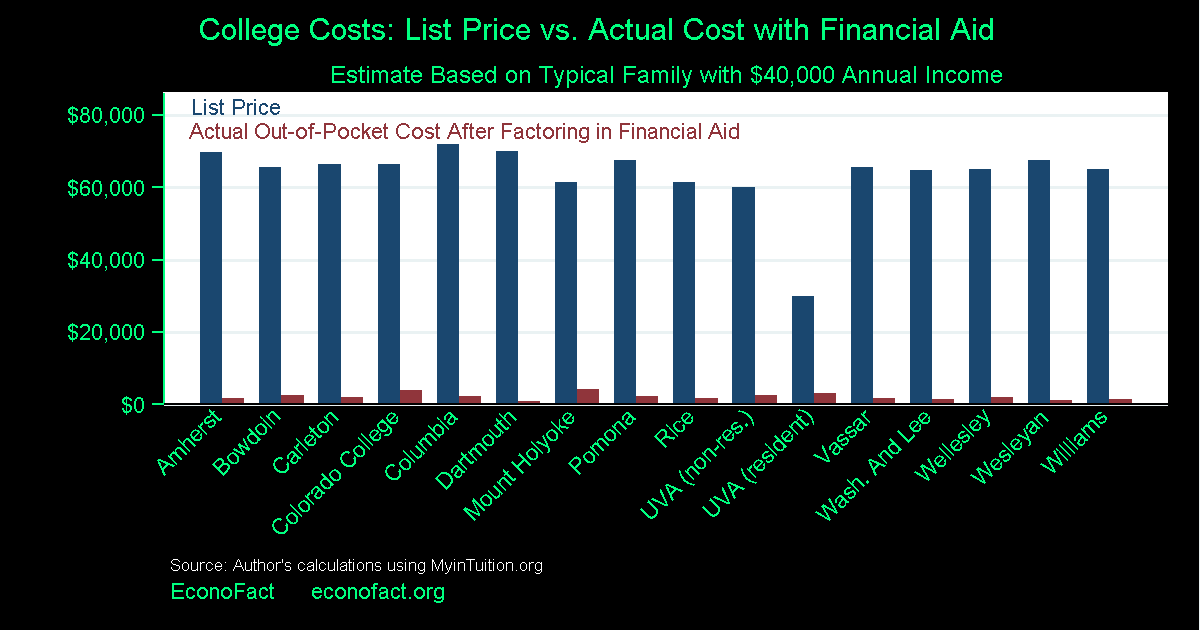

May 30, 2017

How much would a college education really cost? Schools are making it easier to answer this question and it may make a big difference for low-income students.

{kind=link}