Staring Down the Debt Limit, Again

Brookings Institution and Tax Policy Center

The Issue:

In what has become a predictable cycle, policymakers meet under pressure to raise the “debt ceiling,” the legal limit on the amount of debt the federal government can accumulate. In spite of the frequency with which this situation occurs, discussion around the debt ceiling is often shrouded in confusion. Why does the United States have a debt ceiling, and what does it mean to raise it? How have debt-limit negotiations changed over time? What would happen if the debt limit is breached?

Raising the debt limit is a matter of paying bills that we've already incurred.

The Facts:

- The U.S. government is in constant need of borrowing resulting from the contemporary trend of running federal deficits. When the government spends more than it collects in revenues (and thus runs a federal budget deficit), it needs to borrow to make up the difference. The government borrows by selling bonds to investors around the world. While the deficit measures the amount of borrowing the government does over a set period, typically a year, the debt is the sum of all accumulated borrowing, less repayment, that the government has done up to a given point in time. The federal government has run a budget deficit every year since the 1970s with the sole exception of the four years between 1998-2001. The annual deficit exceeded $1 trillion in 2009 in the midst of the Great Recession. More recently, the COVID pandemic sharply raised the need for federal spending. This came on the heels of the 2017 Tax Cuts and Jobs Act, which had lowered government revenues. As a result, the U.S. government deficit surpassed $3 trillion in FY2020, $2.7 trillion in FY2021 and $1.3 trillion in FY2022 (see here). The necessary consequence of this deficit spending is a continual need to borrow.

- Why do we have a debt ceiling? The Constitution granted Congress the powers to tax, borrow, and spend. Until World War I, every issuance of federal government debt explicitly required presidential and congressional approval. During the war, however, President Wilson and Congress eliminated that rule and created an overall limit to make it easier to finance the mobilization. Hence the debt ceiling was born. Since then, Democratic and Republican presidents and Congresses have raised or suspended the debt ceiling more than 100 times, including more than 78 times since 1960 and about once a year this century. It's a common occurrence. (Suspending the debt ceiling, or temporarily allowing the Treasury to supersede it, was relatively rare in the debt ceiling's history. However, Congress has suspended the debt limit seven times since 2013 – most recently between August 2019 and September 2021.) It happens under Democratic and Republican administrations and Congresses and, so far in our history, it's always been passed or suspended when that was the needed action.

- Voters often assume – and lawmakers often assert – that a vote to raise the debt ceiling is a vote for new spending programs. In fact, however, raising the debt limit is about paying for past choices, and debt limit debates are about whether Congress should authorize the government to borrow to pay for spending that it has previously authorized. The government cannot spend any money without Congressional approval. The only reason the debt ceiling becomes an issue is because when Congress authorizes, say, $100 in new spending and $70 in new taxes, it does not automatically authorize the needed $30 in new borrowing. Essentially, Congress requires the government to spend a certain amount of money but, at the time of passage, does not necessarily also authorize the government to raise the funds needed to pay for the program. So, while the rhetoric around raising the debt ceiling centers around “fiscal responsibility” and disciplining federal spending, these discussions should in reality have taken place before legislation that results in increased government spending or reduced government revenue is approved.

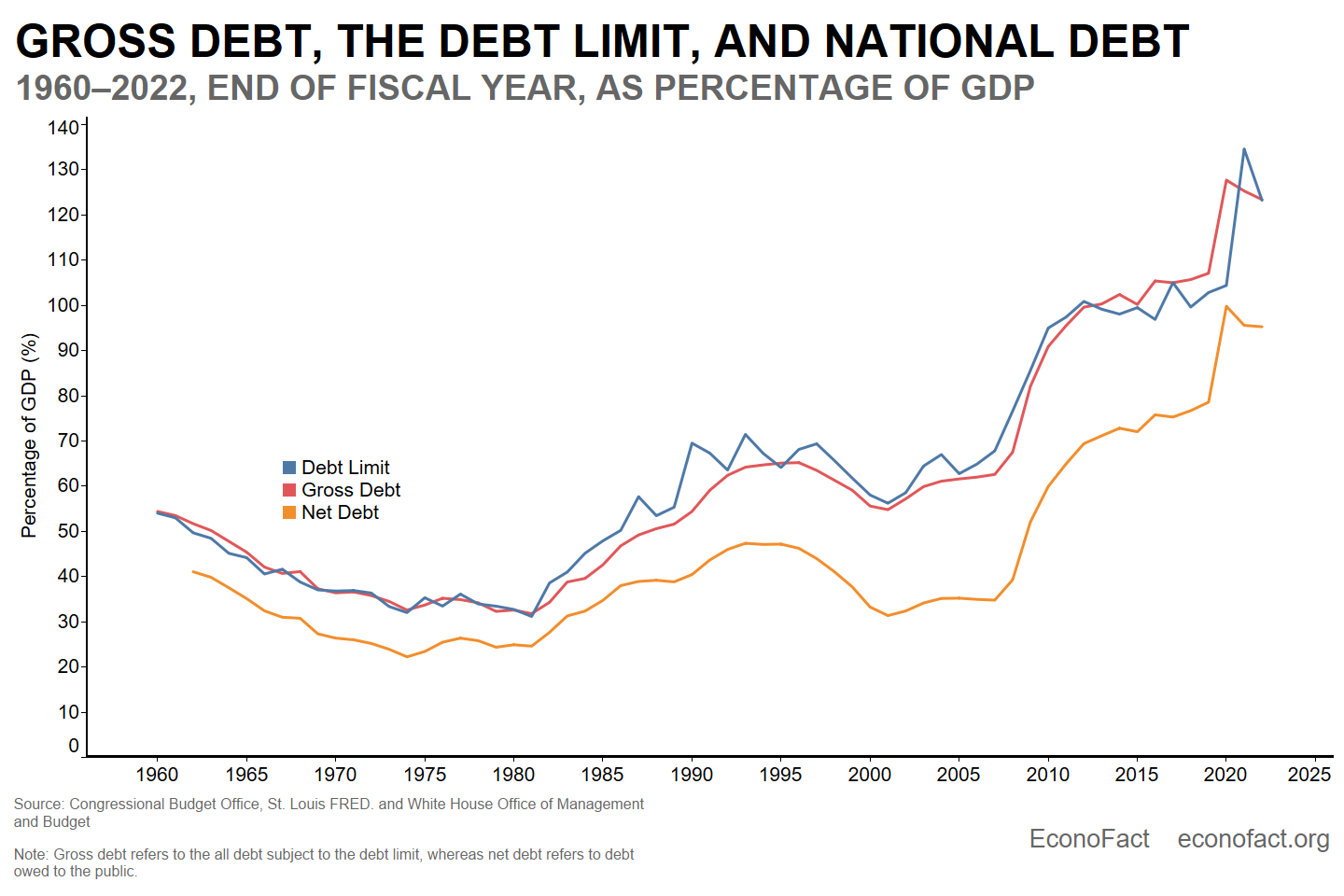

- Gross debt vs. net debt: The debt ceiling applies to a concept that has no economic meaning. For historical and legal reasons, the debt limit applies to what is called “gross debt,” the sum of net debt plus intragovernmental debt. Net debt is what the government owes the public — including investors, pension funds, and domestic or foreign central banks — and it is the measure that economists consider to be important (see chart). Intragovernmental debt is simply what one part of the government owes another. An example is money held in government-owned trust funds, like the Social Security Trust Fund (more detail below). Because it is akin to your right pocket owing your left pocket money, intragovernmental debt has no economic content. By extension, then, gross debt is a legal concept that has no economic significance. Sadly, the popular discussion sometimes focuses on “gross debt.” (Anyone who uses the “$31 trillion” figure is – knowingly or unknowingly – using gross debt. Even Manhattan’s national debt clock focuses on gross debt. That’s a mistake.) The gross debt measure is such a misleading concept that if, for example, the Social Security Trust Fund runs a surplus — that is, when program receipts exceed program costs in a given year — gross debt increases. This happens because the Social Security Trust Fund sends the surplus to the Treasury Department and, in return, it receives bonds from the Treasury (which counts as gross government debt). By investing in these bonds, Social Security benefits have another way to be paid if (and when), in future years, the Trust Fund runs a deficit. Bonds could be redeemed from the Trust Fund, and the Treasury would return some of what it “owes” to Social Security in the process. In the meantime, though, accounting definitions for “gross debt” say that the assets Social Security receives (bonds) are exactly offset by the new “intragovernmental debt” that Treasury faces. Similar patterns apply to other government trust funds.

- What would happen if the debt ceiling were not raised? If government debt reaches its statutory limit, the Treasury Department can typically use any of several accounting gimmicks known as “extraordinary measures” to postpone the day of reckoning. But these typically last only a few months, and then the government would have to default on interest payments or other obligations such as military pay, tax refunds, or safety net payments. The economic consequences of a large-scale, intentional default are unknown, but predictions range from the merely bad to the truly catastrophic. Even flirting with default can create uncertainty, hurt the economy, and drive up interest rates and government costs. In 1979, a computer error triggered an inadvertent default on a small batch of Treasury securities, and spooked investors enough to raise interest rates that the Treasury was required to pay — the mistaken default cost the government about $50 billion (in today’s dollars) in higher interest payments.

- Debt limit negotiations can become quite contentious, especially of late. The debt limit showdown in 2011, exacerbated by the drive of newly-elected Tea Party members, is just one example of the bitter partisanship becoming commonplace in fiscal policy making. Prominent conservatives at the time threatened to block any debt limit increases and let the government default. While they may have sought to improve their bargaining position, they were playing with fire. As noted by Adam Posen, president of the Peterson Institute for International Economics, it was the first time a solvent democracy flirted with default simply out of political stubbornness. At the same time, the Obama administration thought that the threat of the debt ceiling could make it easier to pass unpopular measures to help address the long term fiscal situation (for instance by cutting spending on entitlement programs by raising the retirement age or adjusting the inflation measure of social security) and that they could do that in exchange for raising taxes on the rich. Although policymakers eventually raised the debt limit in 2011, another confrontation took place in 2013. Republicans refused to raise the debt ceiling unless policymakers enacted legislation to address long-term deficits, though the Republicans had proposed no such legislation. Facing enormous public pressure, Republicans relented, and the debt ceiling was “suspended” for about four months. These high stakes negotiations had a cost. The debt ceiling showdown of 2011 is estimated to have cost taxpayers $1.3 billion during that fiscal year and $18.9 billion over ten years. Similarly, as the debt ceiling deadline approached in 2013, interest rates on government debt spiked as investors started to believe that the country faced a real threat of default.

- There are other factors that make risking defaulting on government debt a bad policy option. First, default is unconstitutional, as the Fourteenth Amendment states that “the validity of the public debt…shall not be questioned.” Second, it would not solve the long-term fiscal problem — it would do nothing to help us pay for Social Security, Medicare, and Medicaid in the future. Third, it would actually make the long-term fiscal problem worse by raising the price of future borrowing.

What this Means:

Politicians are playing with fire when they refuse to raise the debt ceiling, especially given the key role that US debt plays in the world financial system, and the benefit the federal government gets from being able to pay low interest rates on its debt relative to other assets. Raising the debt limit has nothing to do with controlling future spending or raising the taxes necessary to pay for future spending; it’s just a matter of paying bills that Congress already approved. The debate about spending more or accumulating more debt implicitly occurred (or should have explicitly occurred) when policymakers voted to raise spending or cut taxes in the first place. While it is difficult to predict the precise magnitude and composition of the economic effects of a default, it is clear they would not be good. At the broadest level, creating a politically-manufactured crisis that threatens the full faith and credit standing of government debt hardly seems like a smart or patriotic thing to do. For all of these reasons, the idea of lawmakers willfully defaulting on our debt by not raising the debt limit is alarming— this is something to avoid.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.