The Success of the Earned Income Tax Credit

University of California, Berkeley

The Issue:

The Earned Income Tax Credit (EITC) is a major anti-poverty program that benefits both children and adults. It is a program with wide bipartisan support since, by providing a tax credit to lower-income working families in a way that incentivizes work, it both promotes greater labor force participation and supports the working poor. It currently does not provide much support for individuals or households without children, but there has been bipartisan support in the past for an expansion of the program to provide greater benefits to this group as well.

The EITC reduces poverty directly through the tax credits it provides working families, but also indirectly – and quite significantly – by incentivizing work.

The Facts:

- The EITC is a refundable federal tax credit that low- to moderate-income families and individuals can claim on their tax returns. The EITC encourages work since the credit is only available to those with earned income. The EITC essentially acts as an earnings subsidy for the lowest levels of income for which it is applicable, does not decrease in dollar terms for the intermediate range of relevant income, and then, in the highest levels of income for which it applies, the credit is phased out with each additional dollar of adjusted income. The phase-out is more gradual compared to many other benefits, which may be why research finds that it does not discourage greater earnings. The actual values of income relating to these three ranges depend upon the number of children in the household and whether or not the tax return is for a married couple or an individual.

- The EITC reached 28.5 million tax filers in 2014. Under the 2015 tax rules, a single taxpayer is eligible for an EITC if he or she has an annual income up to $39,131 and if they claim one child as a dependent, up to $44,454 with two children, and $47,747 with three or more children. The median household income in that year was $56,516, so the EITC extends deeply into the income distribution. The refund available from the EITC can be as much as 45 percent of a family’s pre-tax income; the maximum credit in 2015 was $3,359 for families with one child, $5,548 for families with two children, and $6,242 for families with three children.

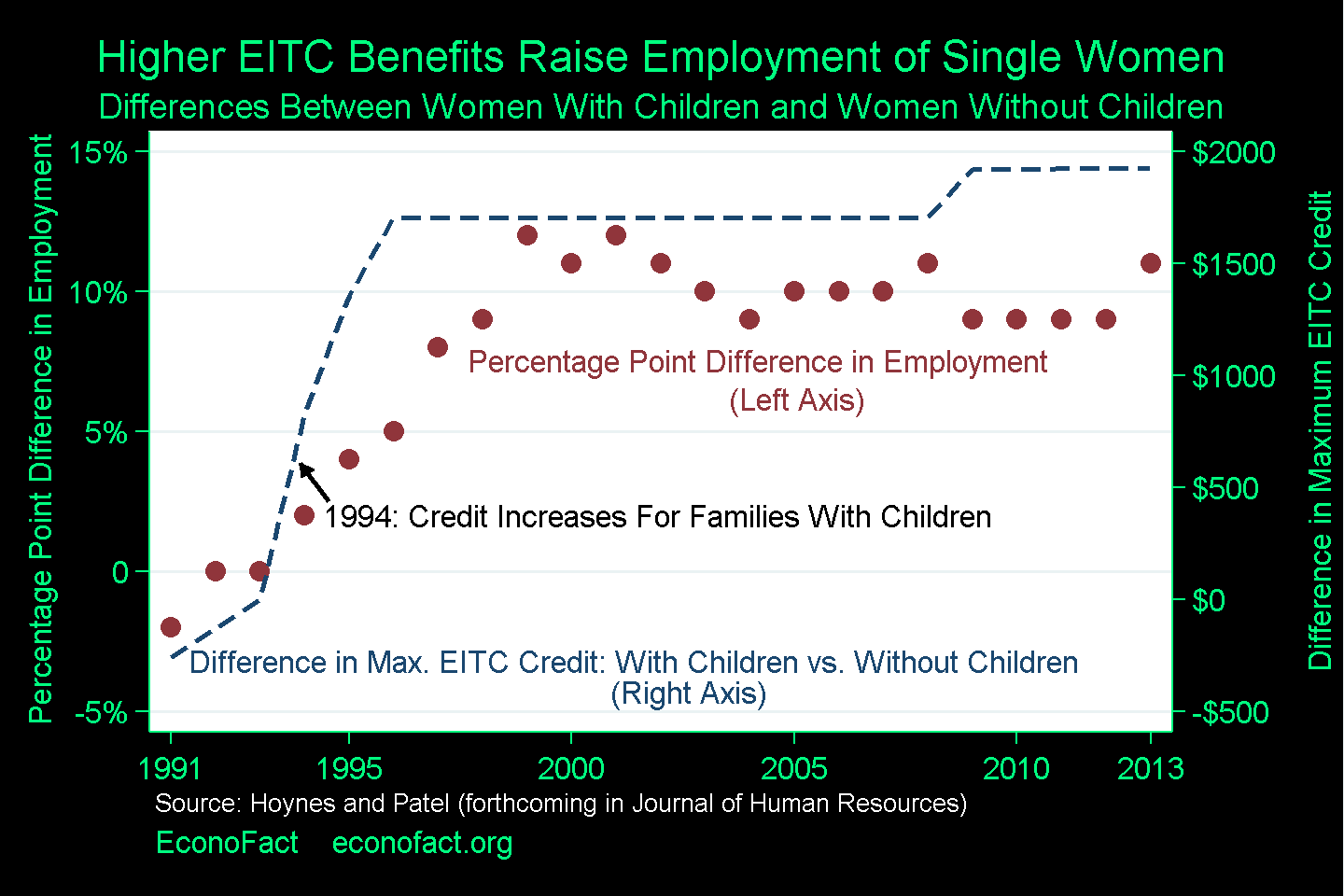

- The EITC increases after tax income and reduces poverty due to the direct tax benefits and, importantly, indirectly as well by incentivizing work. Its effect on promoting work is shown with reference to the last major policy change in the EITC, in 1994, when there was an increase for credits for families with children relative to that for families without children (see chart). The dashed line represents the difference in the maximum credit for single women with children as compared to the maximum credit for single women without children; this line shows the effect of the policy change that began in 1994. The circles represent the estimated difference in employment between single women with children and single women without children. The figure shows that the increase in the relative benefits of working due to the policy change that favored families with children is associated with an increase in the estimated employment difference across these two groups of single women. In a forthcoming publication with Ankur J. Patel, we show that failing to take into account these indirect benefits leads to an underestimation of the anti-poverty benefits of the EITC by as much as 50 percent.

- The benefits of the EITC have been shown to extend to maternal and children’s health, as well as to children’s development. Changes in the EITC in 1993 offer a type of natural experiment that enabled researchers to consider the effects of the program on a range of outcomes. The EITC was found to improve the health of mothers, and reduce their smoking, as well as smoking by pregnant single mothers. The EITC was also found to improve birth outcomes, raise test scores for children, increase high school completion and college attendance rates, which translate into better employment outcomes.

What this Means:

Much of the recently proposed tax reforms are regressive in that the main changes benefit the upper income earners. This regressivity extends to the proposed changes in childcare tax breaks, which would provide little or no benefit to lower income families. Alternatively, the EITC has proven to be an important way to support the working poor and the children in these families. But the EITC largely bypasses families without children – in 2015, the maximum benefit from this program accruing to them was only $503. An extension of the successful EITC to this set of people is warranted as well.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.