The Challenges Facing Social Security

The Brookings Institution

Executive Summary

Social Security is a cornerstone of America’s social safety net, providing retirement, survivor, and disability benefits to over 70 million Americans — approximately one in five people.

Social Security operates within a dedicated trust fund that funds benefits for current beneficiaries with current workers’ contributions and any past excess contributions in reserve. In large part due to demographic shifts that are fundamentally altering the ratio of workers to beneficiaries, trust fund reserves are projected to be depleted by 2034, at which point incoming revenue would cover only 81% of scheduled benefits. Policymakers face critical decisions about how to restore solvency and create a system resilient to future demographic changes through various combinations of revenue increases and expenditure adjustments that will require evaluating important tradeoffs.

I. Social Security Benefits

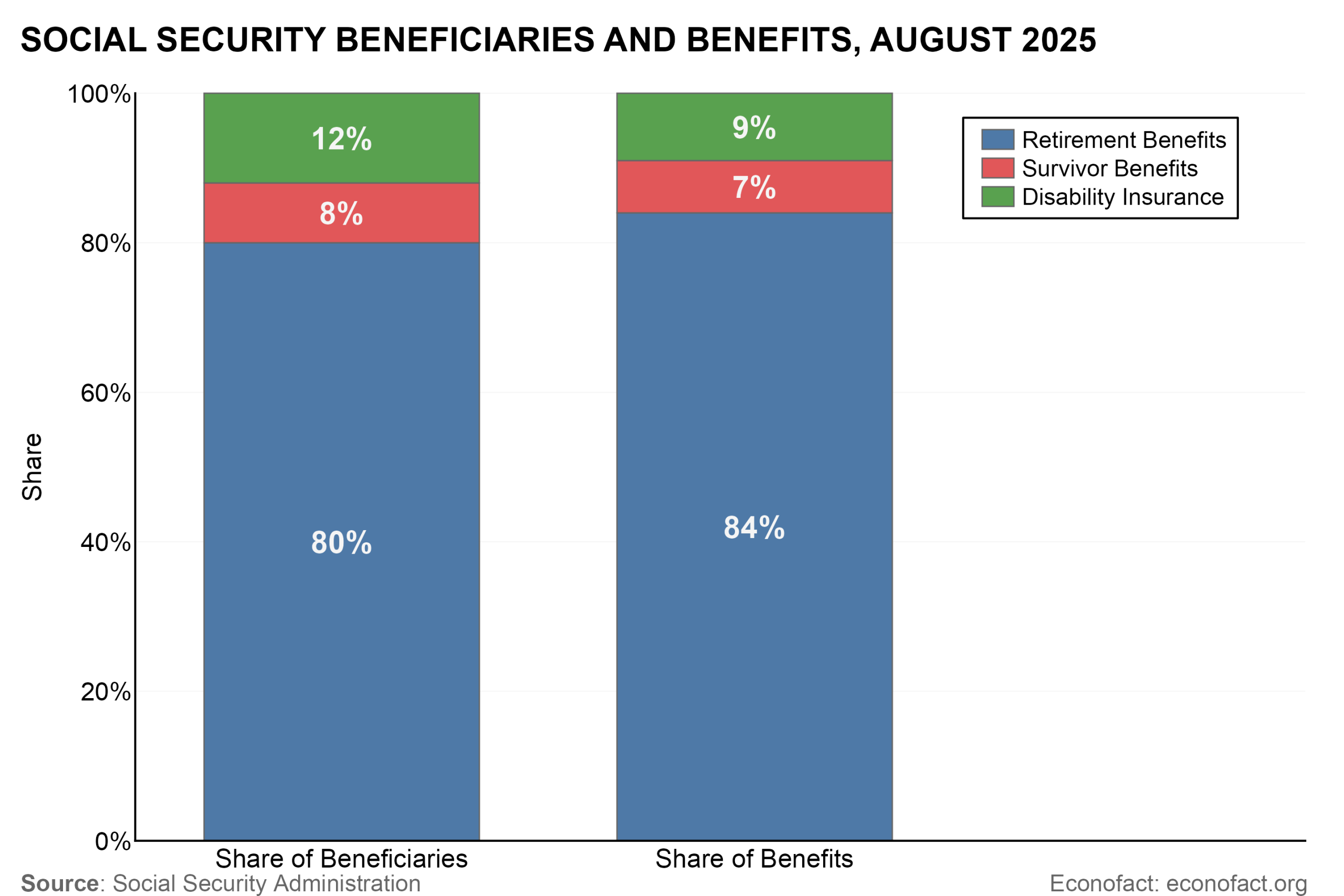

Social Security offers different types of benefits, including retirement benefits, survivor benefits and disability insurance. Retirement benefits are provided to retired workers and spouses/children of retired workers. Survivor benefits are provided to widow(er)s as well as children of deceased workers.1 Disability insurance payments are provided to disabled workers and some spouses and children of disabled workers. Of the $130.7 billion in benefits paid out in August 2025, $109.8 billion went towards retirement benefits, $9.2 billion went towards survivor benefits, and $11.7 billion went towards disability insurance payments. Every year, the Social Security Administration adjusts benefits based on the level of inflation in the economy and increases the benefits by that amount. This adjustment helps protect the purchasing power of beneficiaries throughout their retirement.

Social Security benefits go to about one-in-five Americans. As of April 2026, over 71 million people were receiving Social Security benefits. Of these, almost 63 million were receiving retirement or survivor benefits, while about 8 million were receiving disability insurance benefits. On average, each recipient received $1,933 each month, with the highest average benefits provided to retired workers ($2,081), and lower average benefits paid to survivors ($1,626) and disabled workers ($1,493).

Social Security Retirement Benefits

- A worker’s retirement benefits are based on their earnings history and when they choose to start receiving them. Social Security retirement benefits are calculated based on one’s earnings over their lifetime, subject to a maximum threshold called the taxable maximum. The formula uses the average of someone’s highest 35 years of wage-indexed earnings to determine their Primary Insurance Amount, which represents the benefits they would receive if they retired at their full retirement age. Retirement benefits can be claimed as early as age 62 and as late as age 70, but if someone claims benefits earlier or later than their full retirement age, their benefits are adjusted lower or higher. The benefit formula is progressive and replaces a higher percentage of income for lower earners. These benefits are paid until someone dies, and may continue to a surviving spouse if the surviving spouse’s benefit was lower.

- The importance of Social Security retirement benefits varies across income. One way to assess how important Social Security benefits are to a retiree is to compare them to their pre-retirement earnings. For a worker with very low levels of career earnings, Social Security benefits replace about 80% of prior earnings while for the highest-earning workers the replacement rate is 28%, according to May 2024 estimates from the Social Security Administration.

- Changes to Social Security retirement benefits have been shown to influence people’s behavior. The way benefits are determined can give rise to various incentives that can influence the returns to working or the benefits that people receive when they claim their retirement benefits later. Research has shown that changes in the benefit structure that raise the normal retirement age or increase the returns to delay benefit claiming can extend working lives and shift when people claim their retirement benefits later (Imrohoroğlu & Kitao, 2012; Behaghel and Blau 2012; Duggan, Dushi, Jeong and Li, 2023).

Social Security Disability Insurance

- Criteria for disability insurance payments. Qualifying for disability benefits requires having a medical condition that prevents a person from working and is expected to last at least one year or result in death. In addition to meeting these criteria, applicants must have worked long enough and recently enough in jobs covered by Social Security.2 Screening for disability is a complicated process, and there is potential for errors that lead to both individuals with work capacity being awarded benefits and for those that may benefit to be denied.

- How disability insurance impacts employment. There is evidence that Social Security disability insurance (SSDI) causally reduces employment among awardees (Maestas, Mullen, & Strand, 2013). However, the work capacity of applicants still tends to be extremely low. SSDI applications tend to be countercyclical and increase during recessions, and there is evidence that very few of the people who receive SSDI during a downturn return to substantial work (Autor and Duggan, 2006; Maestas, Mullen, & Strand, 2015).

- How disability insurance impacts mortality. Gelber et al. (2023) show that more generous SSDI benefits reduce mortality among lower-income beneficiaries, but do not find robust evidence of an effect for higher-income beneficiaries. However, when they look at people who appeal an initial denial of benefits, Black et al. (2024) find that SSDI and SSI receipt actually increases mortality for beneficiaries who are on the margin of receiving or being denied benefits, but reduces mortality for less healthy beneficiaries and those with expensive health conditions.

Social Security survivor’s benefits

- Eligibility for survivor’s benefits. Spouses receive survivor benefits if they are age 60 or older, or if they are caring for the deceased’s child under 16. Ex-spouses receive the same benefits if the marriage lasted at least 10 years. Unmarried children under age 18 also qualify for benefits, as do dependent parents. Additional pathways are available if the surviving spouse or children of the deceased are disabled.

- Impacts of survivor’s benefits on income and labor supply. Survivor benefits operate as income insurance after the death of a wage earner. Research has shown that these benefits provide valuable liquidity that dampens the need for surviving spouses to increase labor supply after a death (Coyne, Fadlon, Ramnath, & Tong, 2024), consistent with broader evidence that fatal health shocks raise spousal labor supply primarily when income losses are large (Fadlon & Nielsen, 2021).

Social Security provides additional forms of insurance. Because Social Security benefits are paid until death, the program provides a form of longevity insurance meaning that a beneficiary cannot outlive their benefits, unlike retirement savings, which can run out unless they are annuitized. In addition, because Social Security benefits increase each year with inflation, they protect beneficiaries from the risk of reduced purchasing power during retirement.

II. Financing Social Security

Social Security is financed primarily through a payroll tax on earnings up to a cap. Social Security is primarily financed through a 12.4% payroll tax levied on all earnings below the taxable maximum, which is set to $184,500 in 2026. The payroll tax is split evenly among employees and employers. Self-employed workers are responsible for paying the full 12.4% tax on their net self-employment income. The program also receives income from the taxation of Social Security benefits for higher-income recipients and interest earned on trust fund reserves.

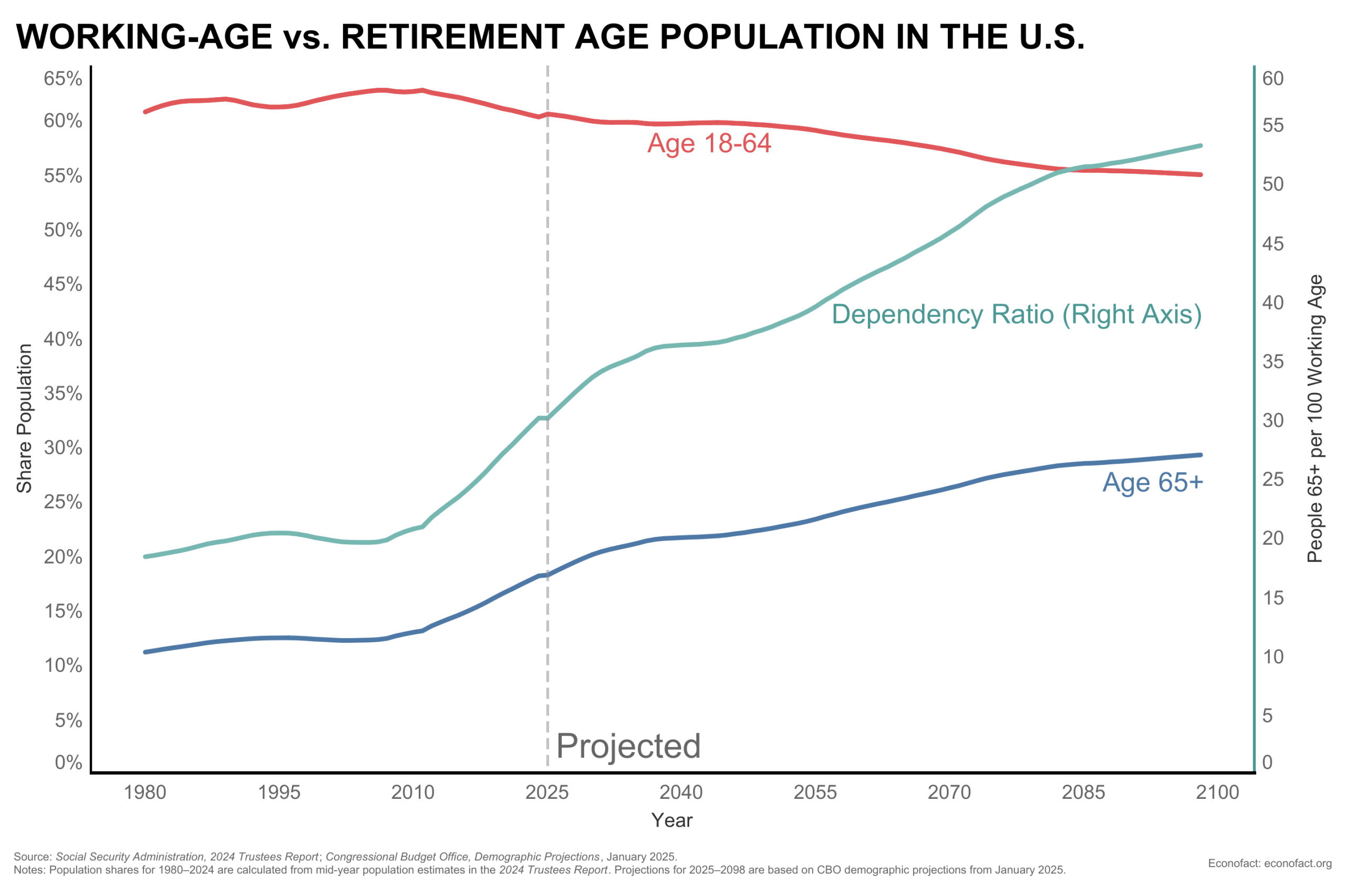

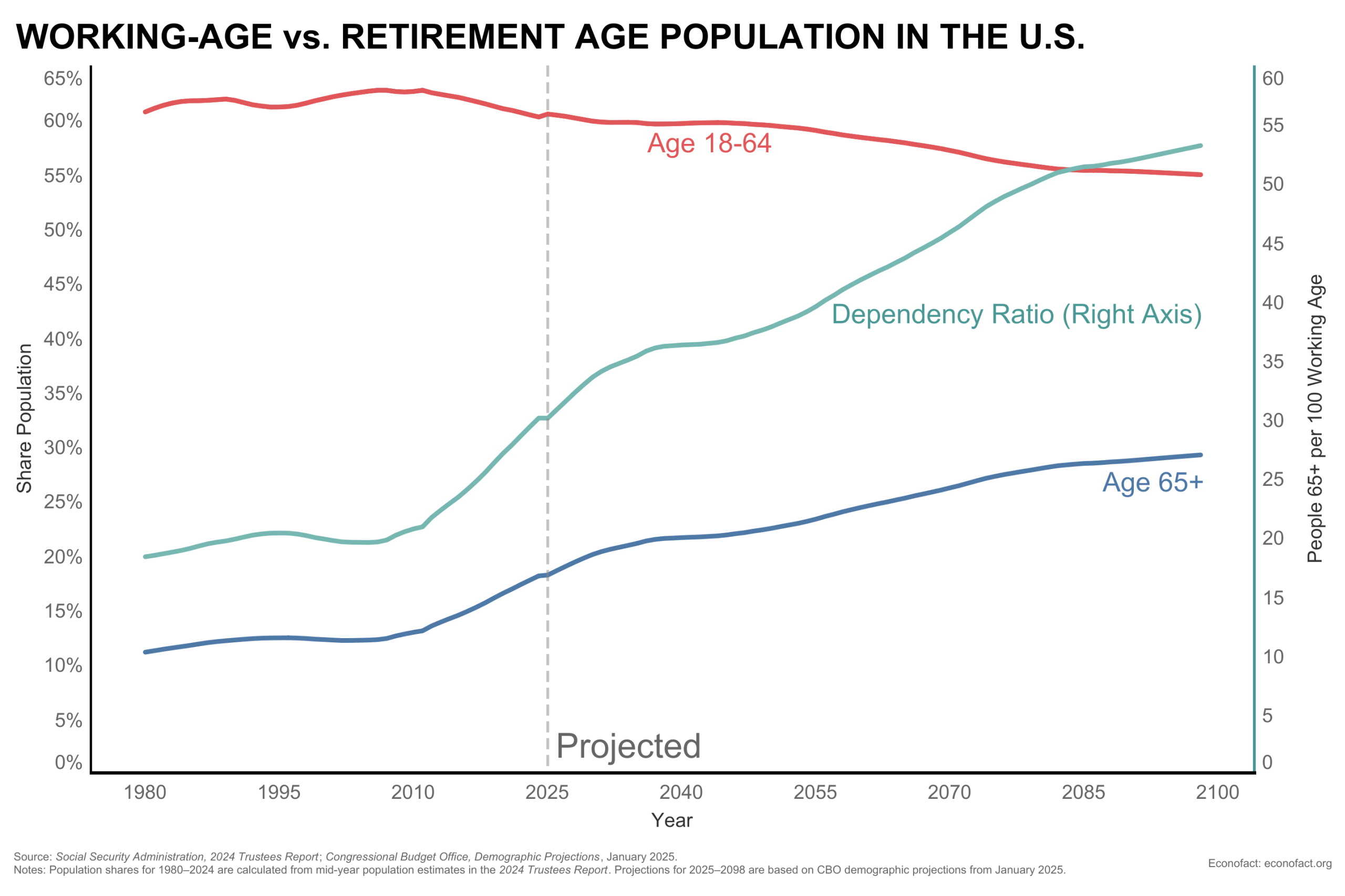

Social Security operates as a “pay-as-you-go” system. Current workers’ contributions fund benefits for current beneficiaries and any excess contributions remain in a dedicated trust fund. Legally, expenditures cannot exceed income and any reserves held in the trust fund. The pay-as-you-go structure did not present problems while the baby boom generation was entering the workforce in the early 1960s, a time when the share of workers paying into the system was rising much faster than the share of the population able to claim benefits. However, in more recent years, the aging of the baby boomers, improvements in life expectancy, and declines in fertility have dramatically reduced the number of workers supporting each retiree, and this ratio is expected to continue to decline into the future. The chart below shows the share of the population ages 18-64 and 65+ from 1980 to the present, and projected shares until 2100. While the share of the population between ages 18-64 has been declining and is expected to continue to decline, the share 65 and over is experiencing the opposite trend. Both of these factors result in the dependency ratio, or the ratio of the share age 65+ to the share age 18-64, to rise. By the year 2100, it is projected that there will be more than 50 people age 65 and over per 100 people age 18-64, up from 30 in 2025.

Click here for a larger version of the graph.

{kind=link}

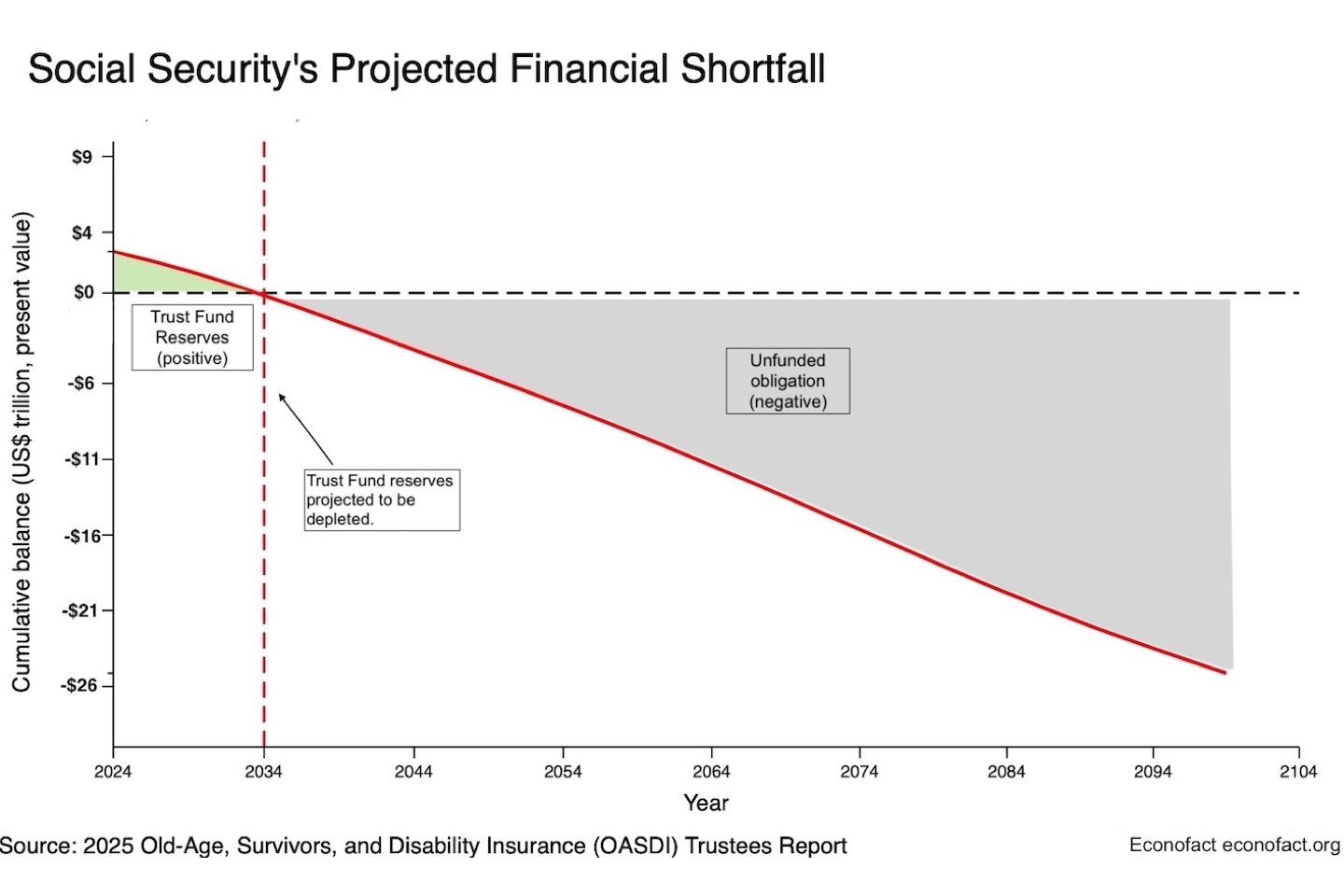

Reports indicate that the trust funds will be depleted within the next decade, and the program will only be able to meet 81% of their scheduled obligations at that time. According to the latest Trustees report, the combined Old-Age, Survivors and Disability Insurance (OASI and DI)Trust Fund reserves held $2.72 trillion at the end of 2024, but these are expected to be depleted in 2034. When the trust funds are depleted, benefits can only be paid from the income that is coming in — about 81% of the benefits that are scheduled to be paid — as there won’t be anything in the reserves to supplement that income. Social Security’s combined retirement and disability programs will have used up all past surpluses by 2034, after which the system owes more than it takes in. In the 10 years following the depletion of the reserves, the Social Security actuaries project an accumulated unfunded obligation of $3.76 trillion. By the end of the century, that gap is expected to grow very large — about $25 trillion in today’s dollars — showing how much the program would need to stay fully funded under current rules.

The challenges to Social Security’s finances are not new. The Social Security trustees have found that the program faces a shortfall over a 75-year horizon for every single report published since the last major set of reforms to the program in 1983 which were prompted by concerns about solvency. These reforms included gradually increasing the retirement age, taxing benefits for higher-income recipients and accelerating scheduled increases in payroll tax rates. The reforms resulted in excess revenue into the program while the baby boomers were working that were meant to keep the program solvent for a 75-year period. However, demographic changes and economic factors since 1983 have accelerated the date the trust fund reserves are expected to be depleted. More recently, last year’s passage of the Social Security Fairness Act, repealed certain provisions that had reduced benefits for public sector workers receiving pensions from non-Social Security covered employment, increasing their benefits and accelerating the depletion date further.

Click here for a larger version of the graph.

III. Policies to put Social Security on solid financial footing

Policymakers have several revenue-raising and benefit-adjusting levers available to address the funding gap. The specific combination of policies chosen involves fundamental trade-offs between adequacy, equity, and fiscal sustainability that reflect broader values about intergenerational responsibility and the role of social insurance in American society.

Raising Revenues: The most straightforward approach involves modifications to the payroll tax. In 2026, earnings above $184,500 (the taxable maximum, which adjusts annually with wage growth) are not subject to Social Security payroll taxes. Raising or eliminating this cap would subject more high earners’ income to taxation, significantly increasing revenue relative to costs. Alternatively, policymakers could increase the payroll tax rate itself, which is currently split between employees and employers at 6.2% each for OASI and DI combined. Even a relatively modest increase of 1 percentage point could close the gap by 26 percent and improve the system’s finances. Some proposals also suggest expanding the tax base by including certain types of compensation — like health insurance premiums that employers pay on behalf of their employees — that are currently excluded.

Reducing Expenditures: These reforms typically focus on adjusting benefit formulas or eligibility parameters. One commonly discussed option is gradually raising the full retirement age beyond its currently scheduled increase to 67, reflecting increased longevity. This effectively reduces lifetime benefits by requiring workers to wait longer to receive their full benefits. Another approach involves modifying the benefit calculation formula itself, such as reducing the replacement rate for higher earners or changing how benefits are indexed to inflation by switching from wage indexing to price indexing for initial benefit calculations.

Fundamental Restructuring: Some proposals would transform Social Security from an earnings-related social insurance program into something closer to a universal basic income for seniors. A flat benefit system would provide all retirees with an identical monthly payment regardless of their earnings history and would sever the link between contributions and benefits. Opponents argue that this type of change would undermine the program’s political durability and public support, while proponents maintain that the link between contributions and benefits is already weak, and that a flat benefit would more efficiently target poverty prevention among the elderly and eliminate regressive elements of the current system. Other more fundamental changes could include borrowing today to create a sovereign wealth fund to fund future Social Security benefits, replacing the current defined-benefit system with mandatory individual retirement accounts, introducing progressive price indexing that would eventually turn Social Security into a flat benefit over several years, or establishing a two-tier system with a universal flat benefit supplemented by earnings-related benefits. Each of these approaches represents a major shift from Social Security’s original design.

Acting early expands the menu of policy options available and reduces the severity of changes needed. With more time to phase in adjustments, policymakers can implement gradual, moderate reforms rather than face the choice between cutting benefits among those near or in retirement or immediate tax increases. Waiting until trust fund depletion is imminent could force policymakers into crisis mode, where the political pressure for immediate action might result in poorly designed policies that disproportionately harm vulnerable populations without adequate protections. Each month of delay requires more painful adjustments to avoid insolvency.

Expedient reforms can also help retirees plan. When policymakers delay addressing known shortfalls, it creates uncertainty that can undermine retirement planning across all age groups. Current retirees worry about potential cuts to their benefits, while younger workers question whether the program will exist in a meaningful form when they retire, potentially leading them to either over-save out of excessive caution or under-save because they do not anticipate cuts that will impact their future benefits. By contrast, enacting reforms well in advance demonstrates political commitment to the program’s sustainability and allows the public to understand exactly what they can expect from Social Security throughout their retirement years. When changes are implemented decades before they take full effect — such as gradually raising the retirement age or adjusting benefit formulas — individuals in their 30s, 40s, and 50s can recalibrate their financial plans, perhaps choosing to work longer, save more, or adjust their expected retirement lifestyle.

IV. Providing Longer-Term Viability and Sustainability

Beyond addressing the immediate 75-year actuarial shortfall, policymakers should consider several broader questions that will determine Social Security’s long-term viability and effectiveness as the cornerstone of America’s retirement security system.

Are benefit levels adequate for those who depend most heavily on the program—particularly lower-income workers and vulnerable populations such as widows and the disabled? Some reform proposals include enhanced minimum benefits to ensure all career workers receive payments above the poverty line, special protections for the oldest beneficiaries whose resources have depleted over long retirements, and caregiver credits for those who left the workforce to care for children or elderly relatives. Strengthening these elements might increase costs but would better align the program with its anti-poverty and insurance objectives. Additionally, consideration should be given to whether Social Security should adapt to changing family structures, career patterns, and the rise of gig economy work that doesn’t fit traditional employment models.

Is Social Security viable and sustainable beyond its traditional 75-year planning horizon? The standard 75 year planning horizon for actuarial projections has limitations that can create a false sense of security. Reforms that appear to “solve” the shortfall within this window may simply push costs beyond it, leaving future generations to confront the same challenges. Achieving sustainable solvency—where the program remains in balance indefinitely rather than merely for 75 years—requires different policy choices that incorporate the growth rates of program income and costs into the future.

How can policymakers best account for highly uncertain future demographic and economic projections? The current financing challenges stem largely from ongoing demographic shifts—the baby boom generation’s retirement, increasing longevity, and falling fertility rates—and future demographic trends are no less uncertain. Future birth rates, immigration levels, labor force participation, and mortality improvements will all profoundly affect the age structure of the population and the ratio of workers to beneficiaries. A resilient system might include automatic adjustments tied to factors such as the dependency ratio, longevity indexing that automatically adjusts retirement ages or benefit formulas as life expectancy changes, or parameters that respond to actual economic and demographic conditions. This approach, used successfully in several European countries, would depoliticize ongoing adjustments and ensure the program adapts continuously rather than lurching from crisis to crisis.

Who bears the costs of reforms? Any set of reforms involves difficult decisions about who bears the cost of closing the funding gap—current beneficiaries through benefit reductions, future beneficiaries through lower promised benefits, current workers through higher taxes, or all taxpayers through general revenue transfers. These distributional choices reflect fundamental values about fairness, intergenerational equity, and the appropriate degree of progressivity of the tax and benefit structure. While the current system’s trust fund mechanism is designed to urge policymakers to take action in face of future shortfalls, the way that shortfalls are addressed is subject to political pressures and thus creates uncertainty in the economy.

How can other policies support Social Security viability? Policies that strengthen economic growth and the size of the labor force can improve the underlying demographic and economic fundamentals that determine Social Security’s sustainability. While technically outside the program itself, broader policies that affect the number of workers contributing to the system and the wage base subject to taxation can contribute to the program’s future success.

Further reading

Autor, D. H., & Duggan, M. G. (2006). The growth in the Social Security Disability rolls: A fiscal crisis unfolding. Journal of Economic Perspectives, 20(3), 71–96. https://doi.org/10.1257/jep.20.3.71

Behaghel, L., & Blau, D. M. (2012). Framing Social Security Reform: Behavioral Responses to Changes in the Full Retirement Age. American Economic Journal: Economic Policy, 4(4), 163–179.

Black, B., French, E., McCauley, J., & Song, J. (2024). The effect of disability insurance receipt on mortality. Journal of Public Economics, 229, 105033.

Coyne, D., Fadlon, I., Ramnath, S. P., & Tong, P. K. (2024). Household labor supply and the value of Social Security survivors benefits. American Economic Review, 114(5), 1248–1280.

Duggan, M., Dushi, I., Jeong, S., & Li, G. (2023). The effects of changes in social security’s delayed retirement credit: Evidence from administrative data. Journal of Public Economics, 223, 104899.

Fadlon, I., & Nielsen, T. H. (2021). Family labor supply responses to severe health shocks: Evidence from Danish administrative records. American Economic Journal: Applied Economics, 13(3), 1–30.

Gelber, A., Moore, T., Pei, Z., & Strand, A. (2023). Disability insurance income saves lives. Journal of Political Economy, 131(11), 3156-3185.

Imrohoroğlu, S., & Kitao, S. (2012). Social Security reforms: Benefit claiming, labor force participation, and long-run sustainability. American Economic Journal: Macroeconomics, 4(3), 96–127.

Maestas, N., Mullen, K. J., & Strand, A. (2013). Does disability insurance receipt discourage work? Using examiner assignment to estimate causal effects of SSDI receipt. American Economic Review, 103(5), 1797–1829.

Footnotes

- Survivor benefits are also paid to some widowed mothers and fathers and parents of deceased workers. ↩︎

- While not the focus of this piece, the Supplemental Security Income (SSI) program also offers disability benefits regardless of work history, and some people receive benefits from both Social Security disability insurance and SSI. SSI is a needs-based program funded by general tax revenues, but uses the same medical standards to evaluate disability. ↩︎