Tariff Wars and the United States Trade Deficit

Independent Economic Consultant

The Issue:

The Trump Administration has argued, including in an April 2025 Executive Order, that U.S. trading partners have used tariffs and non-tariff barriers to trade in ways that have led to “large and persistent annual U.S. goods trade deficits.” This has been a central rationale for the Administration to raise tariffs significantly, reversing several decades of U.S. trade liberalization and triggering retaliatory tariff hikes by some other countries. However, considerable research has mostly concluded that foreign trade policies have not been a significant contributor to the U.S. trade deficit. Similarly, recent research suggests that the recent tariff hikes will have only a limited impact on the U.S. trade deficit, at the cost of a significant worsening of U.S. and global economic prospects.

There is a broad consensus among economists that tariffs have not played a major role in determining the size or persistence of the U.S. trade deficit.

The Facts:

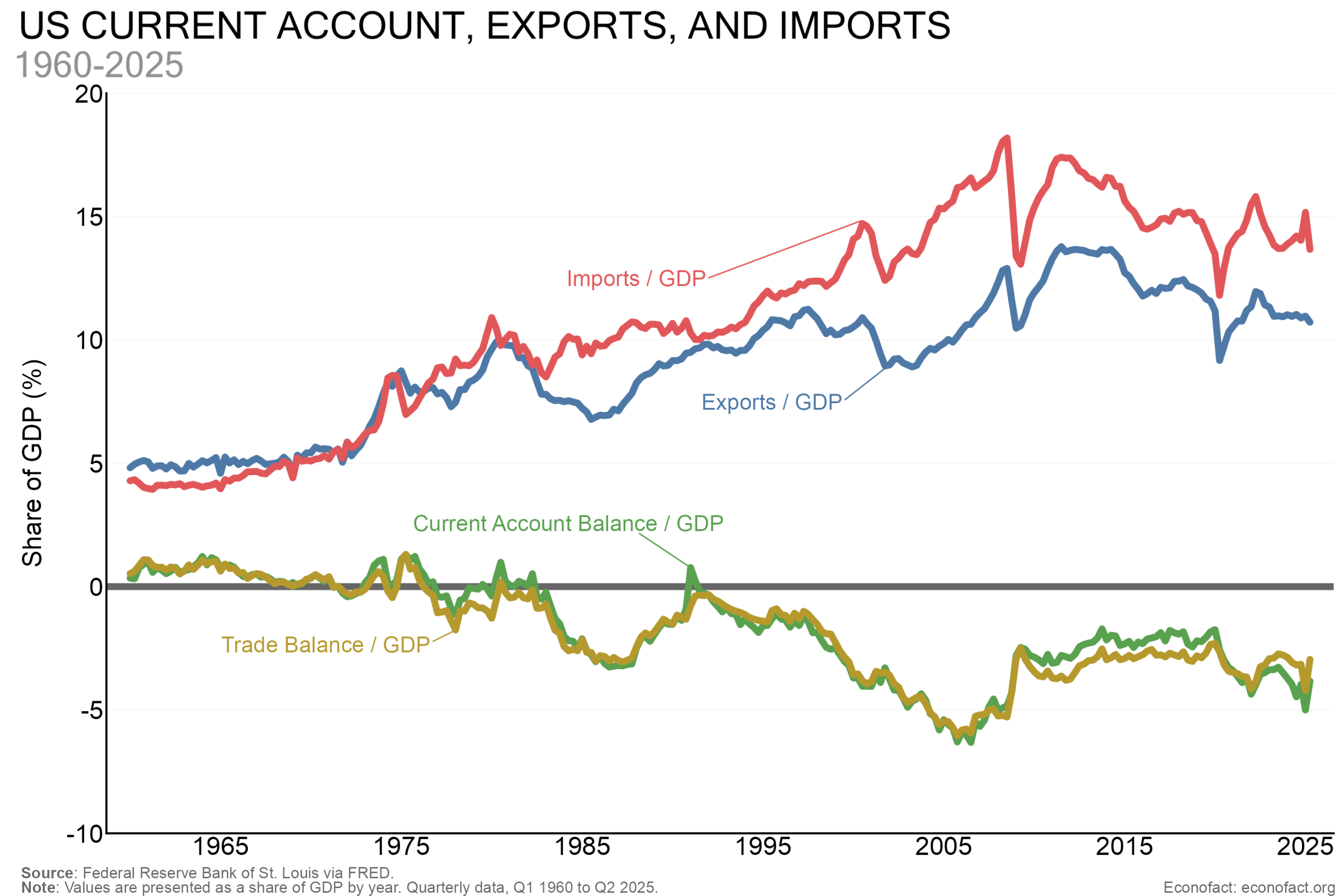

- The United States has run large trade deficits for decades. As shown in the graph, U.S. exports and imports (of both goods and services) have risen significantly since the 1970s, but the more rapid rise in imports has resulted in substantial overall trade deficits that have averaged 3½ percent of Gross Domestic Product (GDP) since 2000. This deficit had been partially offset in the past by net income inflows (income earned by Americans on foreign assets minus income earned by foreigners on American assets that they hold). However these net flows have turned negative in recent years, which has left the deficit on the current account—which represents the sum of the trade account and net income flows—at almost 4 percent of GDP, the third largest rate among all OECD countries. And since current account deficits have to be matched by borrowing from abroad, the United States’ net indebtedness to the rest of the world has risen steadily to reach 82 percent of GDP by end-2024.

- The U.S. trade deficit is most often viewed by economists as resulting from fundamental macroeconomic forces, in particular those driving saving and investment. This is because a country’s current account balance, by definition, equals the difference between national saving and investment in a country’s national accounts. Using this framework, it generally agreed that a key factor explaining the size and persistence of the U.S. trade deficit has been the protracted decline in the personal saving rate that began in the 1980s, when it fell from an average of 12¼ percent in the 1970s to an average only about 5¾ percent in 2000-2025. This decline, and the corresponding increase of consumption, including on imports, has been attributed to a boom in U.S. asset prices and increased credit availability. It is also generally agreed that government budget deficits, which are a form of national dissaving, have also contributed to the current account deficit. U.S. government deficits rose significantly beginning in the 1970s due to both cuts at the federal level of tax rates as well as expanded payments for health and other social programs. Further spending increases and tax cuts occurred with the onset of the global financial crisis in 2008 and the 2020 global pandemic, taking the deficit to an average of over 6 percent of GDP during 2010-2023. The IMF recently concluded that the United States’ large fiscal deficit relative to that in the rest of the world boosted the U.S. trade deficit by 0.6 percentage points of GDP in 2024. Finally, the current account deficit has also been boosted by investment booms, such as the ones in the 1990s (until the bursting of the dot-com bubble in 2000) and again during the first decade of this century (until the collapse of the U.S. housing market). Stimulative monetary policies during these periods are often thought to have contributed to these investment booms, while also helping to dampen the personal saving rate.

- Foreign macroeconomic forces have also had some impact on the U.S. trade deficit since the counterpoint to the U.S. deficit has been large surpluses elsewhere in the world. In 2005, then Federal Reserve Vice Chair Ben Bernanke argued that the U.S. deficit stemmed from excessive savings by emerging market economies (including China) — often termed a “Global Saving Glut.” However, such imbalances have narrowed over the past two decades and the IMF’s recent assessment now views these forces as only “moderately” important. There is also an argument that the demand for the dollar by foreign central banks for their reserves and by the private sector as a safe haven strengthens its value which makes American exports more expensive and imports to the United States cheaper (as argued by now Fed Governor Stephen Miran). However, a recent IMF analysis does not suggest that the dollar’s role as a reserve asset has significantly boosted the trade deficit, possibly because the rate of increase of global reserve positions slowed after 2010 and the share of the U.S. dollar in these positions has also diminished.

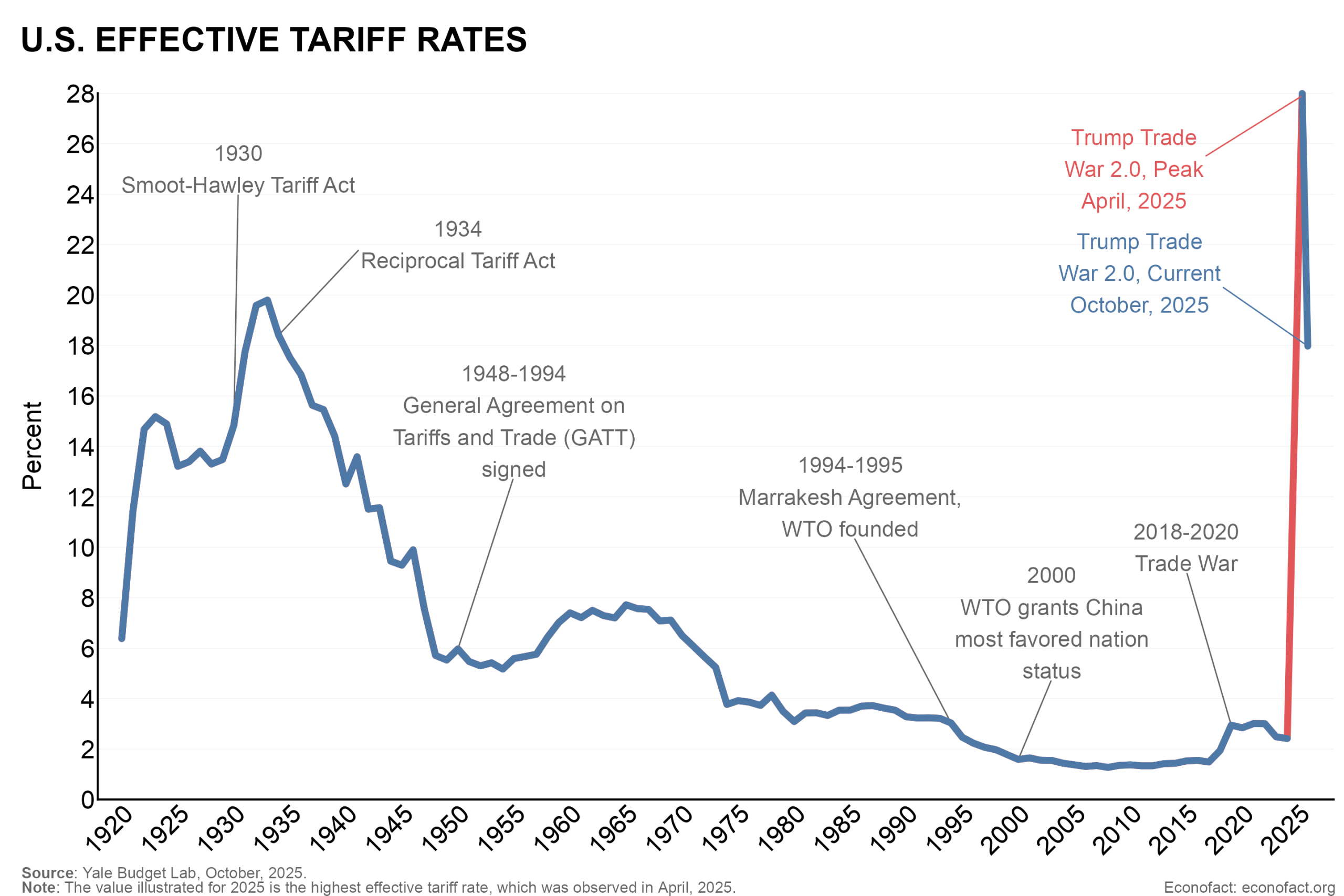

- There is a broad consensus among economists that tariffs (and other trade policies) have not played a major role in determining the size or persistence of the U.S. trade deficit. United States tariff rates were high in the pre-World War II period, in particular during the 1930s (see graph). But these rates came down after the war and have fallen significantly since the 1970s. This was in the context of concomitant cuts by other countries as part of international trade agreements that were actively promoted by the United States (e.g., multilateral initiatives such as the World Trade Organization and regional trade agreements such as the U.S., Mexico, and Canada Free Trade Agreement). A recent study by the Federal Reserve Bank of Dallas finds no apparent correlation between the size of trade balances and effective tariff rates for a wide sample of countries, a result consistent with other research.

- Against this background, most analysts have concluded that the recent U.S. tariffs would have only a modest impact on the U.S. trade deficit. One important reason is that export competitiveness would be damaged as a significant share of the U.S. tariffs has fallen on products such as steel, aluminum, copper, lumber, semiconductors, etc., that are key inputs for U.S. exporters. The IMF has estimated that if tariffs were actually imposed at the levels recently announced (including the retaliatory measures taken by China) this would lower the U.S. current account deficit by less than ½ percent of GDP by 2030.

- Moreover, higher tariffs would likely come at the cost of weaker U.S. growth and incomes. For example, the IMF estimated that the impact of the tariff war would be to lower U.S. GDP by roughly 1 percent relative to baseline in three years, with the loss rising to as much as 1.3 percent annually in the longer run. In the nearer term, output losses stem from the impact of tariffs on inflation and investment, and in the longer term from the negative impact on U.S. productivity as capital and other resources move into sectors where the United States has a comparative disadvantage. The IMF’s more recent analysis highlights in addition that uncertainty regarding trade policies is likely to further weigh on activity by dampening business and consumer confidence. This result is consistent with findings in other studies (e.g., here and here and here). An additional consequence is that the costs of tariffs fall disproportionally on the poor by raising prices of imported goods, which represent a larger share of their consumption.

What this Means:

There are considerable analyses and real-world experiences to suggest that the U.S. administration’s tariff increases would only modestly lower the U.S. trade deficit, largely because tariffs would not appreciably address the deficit’s more fundamental root causes—large U.S. fiscal deficits and high levels of U.S. personal consumption. Any improvement in the U.S. trade balance that might be achieved through tariffs would likely come at the cost of a dampening of employment and incomes, both domestically and abroad. These adverse effects on U.S. growth prospects would be exacerbated if recent U.S. tariffs and other policies erode global confidence in the U.S. dollar and global demand for U.S. assets.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.