Facing the Social Security Shortfall (Updated)

The Brookings Institution

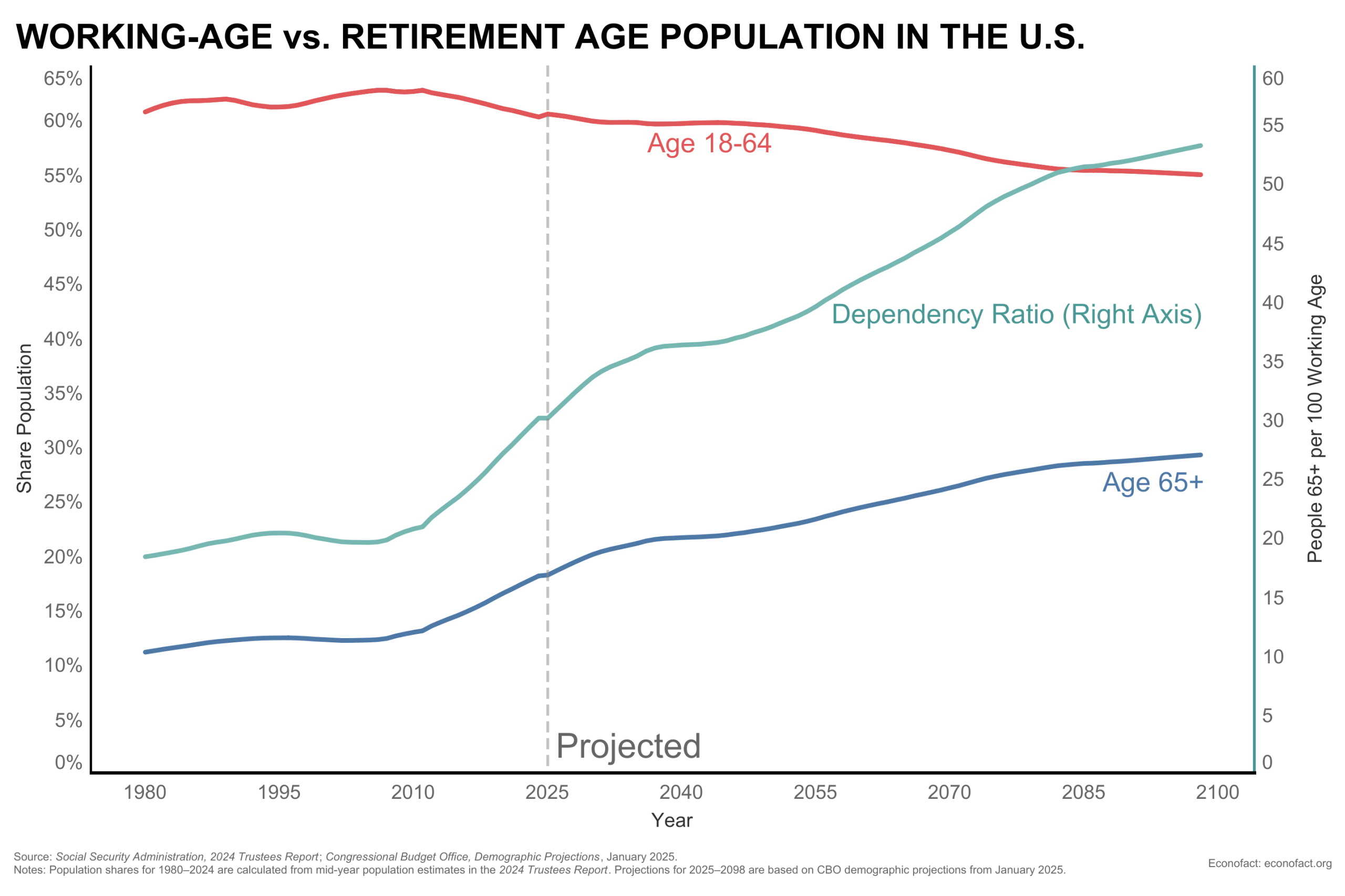

Click here for a larger version of the graph.

The Issue:

Social Security is a hugely important program to a large share of Americans, with about one in five people in the United States receiving benefits in 2025. Both major political parties have been reluctant to reduce Social Security benefits and averse to raising payroll taxes. Yet the economic reality is that there will have to be some kind of change in the program in the next decade. Given its funding structure, if the program continues to roll forward in its current trajectory — and no action is taken by Congress — Social Security will only be able to cover 81% of promised benefits starting in 2034, according to the latest estimates of the Social Security trust funds report. Beyond deciding how to distribute the burden of revenue increases and benefit cuts needed to close the gap, addressing the Social Security shortfall provides an opportunity to take a comprehensive look at how policy can best help people manage the risks they face in retirement.

The economic reality is that there will have to be some kind of change with respect to Social Security in the next decade.

The Facts:

- Almost 69 million Americans per month receive Social Security benefits in 2025, totaling about $1.6 trillion in benefits paid during the year. The program, created in 1935 in the wake of the Great Depression, has been instrumental in reducing elderly poverty. Retirement benefits account for almost 80% of total Social Security benefits paid and are awarded to those who have worked a certain number of years and are at least age 62. In addition to retirement benefits, Social Security provides disability and survivorship benefits. Disability benefits are awarded to workers who have contributed into the program for a set number of years and who can no longer work due to a disability that meets medical criteria. In addition to being paid to the disabled worker, disability benefits can also be paid to spouses, children, and other dependents of the disabled worker. Survivor benefits are paid to family members of a worker who dies, including spouses, children, and dependent parents.

- The amount of the monthly Social Security benefit is not meant to replace all of a worker’s prior earnings. How important these benefits are to a retired worker’s overall income varies greatly over the income distribution. Retirement benefits are based on a worker’s prior earnings and on the age at which they start claiming benefits. The average benefit paid to a retired worker in 2025 is about $1,900 per month. The higher a worker’s prior earnings (up to a maximum taxable amount — $176,100 in 2025), the higher the benefit. How much people depend on Social Security Benefits as a source of income in retirement varies greatly across the income distribution. One way to assess how important Social Security Benefits are to a retiree is to compare them to their pre-retirement earnings. For a worker with very low levels of career earnings, Social Security benefits replace about 80% of prior earnings while for the highest-earning workers the replacement rate is 28%, according to May 2024 estimates from the Social Security Administration.

- Beyond being an income transfer program, Social Security is also an important source of insurance. As someone approaches retirement, their financial security depends on factors such as whether they experience a health condition that limits their ability to work; whether their sources of income can keep up with the prices of goods that they purchase; the chance of being widowed at a relatively young age; the chance of having their health deteriorate and requiring costly care for a long period; or even the risk of living too long and outliving their savings. Social Security provides some insurance to all contributing workers against a work-limiting disability or the income losses incurred by the early death of a family wage-earner. Social Security also provides a degree of longevity insurance because — unlike retirement savings which can run out unless they are annuitized — Social Security retirement benefits continue to be paid until death. Moreover, every year, the Social Security Administration adjusts benefits based on the level of inflation in the economy and increases the benefits by that amount. While it may not provide a perfect adjustment if, for instance, medical costs are a big share of spending and those costs increase faster than inflation, it does go a long way towards insuring some of the inflation risk that people might experience in retirement.

- The way in which Social Security is funded exposes the program to challenges. Unlike other forms of saving for retirement, where workers put away savings into an account that is dedicated to them, this pay-as-you-go system acts more like a checking account: current workers are paying into the system and the current beneficiaries are receiving those funds out of the program. This structure did not present a challenge while the baby boom generation was entering the workforce in the early 1960s, with the share of workers paying into the system rising much faster than the share of the population able to claim benefits. Since the early 2000s the tables have turned: the share of the population that is 18-64 has been declining while the share that is 65 and older grew at the fastest rate in over a century going from 13.0% of the total population in 2010 to 16.8% in 2020. As a result of these opposing trends, while there were about 18 people aged 65 and older for every one hundred working-age Americans in 1980, this dependency ratio grew to 30 retirement-age Americans per hundred workers in 2025 (see chart). The ratio of retirees to workers is likely to continue increasing beyond the retirement of the baby boomers because of the lower fertility rates that the US has experienced over the last 15 years or so.

- For several years the trustees of the Social Security Trust Fund have been projecting that the program has promised more benefits than it is able to pay out. According to the latest Trustees report, the combined Old-Age, Survivors and Disability Insurance Trust Fund is expected to be depleted in 2034. That means that, at that time, benefits can only be paid from the income that is coming in, as there won't be anything in the reserves to supplement that income. Legally, the trust fund cannot borrow money. At that point, the trust funds would only be sufficient to pay about 81% of the benefits that are scheduled to be paid.

- Unless policymakers make deliberate efforts to clarify how to handle shortfalls, it is likely that the program will face similar uncertainties in the future. Right now, we face uncertainty in how the gap between the funds coming in and the benefits promised will be closed. It is not clear if beneficiaries will face those benefit cuts; if taxpayers will be liable for those tax increases, or something else. Both the benefits paid and the contributions into Social Security are prescribed by law. This means that it is likely that demographic or economic assumptions will change again at some point in the future, resulting in an imbalance between the benefits that are scheduled to be paid and the revenue that is expected to come in. For example, when there’s an economic downturn, there are fewer people working and contributing into the trust fund.

- There are other ways in which the retirement security system is lacking that could be addressed. While the existence of Social Security and Medicare have contributed to a dramatic reduction in elderly poverty, some groups face persistent challenges. Although survivor benefits provide helpful protection to surviving spouses, there is some evidence that the existing level of survivor insurance may not be adequate to cover the costs that a surviving spouse incurs. In 2019, among those 60 and over, 16% of new widows lived in poverty, compared to 10% overall.

- There remain significant expenditure risks that the elderly face that are not fully addressed by Social Security and Medicare. While Social Security does not provide any kind of medical payments, Medicare provides a source of health insurance for most people over the age of 65. However, Medicare doesn't cover everything, and there are significant copayments and deductibles that a person may be responsible for. For example, annual out-of-pocket spending on healthcare was on average $6,663 for all beneficiaries enrolled in traditional Medicare in 2019, according to a study by AARP. This average out-of-pocket spending for health care was equivalent to about 38 percent of the average annual Social Security retirement benefit ($17,460) in 2019. Moreover, there is a significant coverage gap regarding long-term care services for chronic conditions. Assistance with things like using the bathroom, feeding or walking across a room due to a chronic condition is not something typically covered by Medicare. This type of care is costly and largely paid for either out-of-pocket, through state Medicaid programs for those who qualify, or provided by unpaid caregivers, often spouses and adult children, who indirectly bear the costs through reduced labor force participation and adverse impacts on their own health. A person turning 65 between 2021 and 2025 is estimated to incur, on average, $120,900 in paid long-term care costs, of which 37 percent is estimated to be paid out-of-pocket, and the remainder covered by a combination of Medicaid (and other sources of public insurance) and private insurance (see here).

What this Means:

The economic reality is that there will have to be some kind of change with respect to Social Security in the next decade. What that looks like is unclear at this stage. Would it be an across-the-board cut or a cut that applies more to certain people than others? Will costs fall on all taxpayers, or increase the burden on current workers? Delaying real talk about the program makes it harder to solve. As we wait, the timeline that we have to fix it is shorter and the change that is needed is more drastic than it would be otherwise. While addressing the imminent financial challenges of the program will be unavoidable, we shouldn’t just be thinking about the issue of solvency. What is the role of government and markets in providing this protection? How can we ensure that our major entitlement programs that people rely on are not just solvent but sustainable for the long term? Social Security reform offers an opportunity to move towards a comprehensive look at how policy can best help people manage the risks they face in retirement.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.