Flood Insurance in a World with Rising Seas

Queens College, City University of New York

The Issue:

Flooding is a major cause of damage and property loss to homeowners in the wake of hurricanes. Even absent major weather events, flooding has become an issue for coastal communities like Miami Beach, where rising sea levels and decades of development — combined with local characteristics — have been increasing flood exposure. Yet most homeowners insurance policies do not cover damage from floods. And, the government program designed to fill this void in flood-prone areas was $23 billion in the red as of 2016.

Sea level rise and coastal development mean a higher share of population and higher value of property are at risk of severe flooding.

The Facts:

- Rising sea levels have increased the risk of coastal flooding over the last few decades, becoming the most economically damaging impact of climate change for many coastal locations. The increasing flood risk has been shown to arise from increased likelihood of tidal flooding in low-lying areas, increased frequency and severity of coastal flooding, and intensification of extreme flooding events.

- While the risk of flooding has been increasing, so too has the share of population and the value of property at risk in the coastal U.S. There has been a large increase in population in shoreline counties in the United States. For instance, the population of counties that are susceptible to hurricane damage grew 22 percent faster than the overall U.S. population between 2000 and 2010, according to a report by the Congressional Budget Office. (The disproportionate growth of coastal counties is a long-standing trend and was even more rapid between 1950 and 2000, when the population of coastal counties grew over three times faster than that of the U.S. as a whole.) According to AIR Worldwide, a firm that estimates the risk of catastrophic events, more than $1 trillion in property assets are currently located on the 100-year flood zone — areas estimated to have a 1 percent chance of flooding in any given year by the Federal Emergency Management Agency (FEMA) — in the east coast of the United States.

- Due to the lack of availability of flood coverage by private insurance markets, the U.S. government established the National Flood Insurance Program (NFIP) in 1968. The goal was to provide affordable (i.e. subsidized) flood insurance to encourage homeowners to protect against the risk entailed by living in flood zones. The goal was also to encourage risk reduction efforts by local communities (for instance, installing drainage or levee systems that could mitigate flooding risks would lead to reductions on flood insurance premiums). The program, managed by FEMA, establishes detailed flood maps that determine the risk faced by each individual property, and the resulting insurance premia. Participation was originally voluntary but, since 1973, properties located on the 100-year floodplain are required by law to purchase flood insurance if they have federally-backed mortgages or have received FEMA assistance in the past (see here). Coverage by the NFIP has risen to over 5 million policy holders.

- The existence of federally subsidized insurance means that homeowners do not bear the full cost of owning a property in an area at high risk of flooding. In theory, if people faced the more expensive premiums that reflect the full flooding risk they might choose not to build or to buy properties in high-risk areas. The availability of subsidized flood insurance through the NFIP may have contributed to the increasing population in flood-prone coastal areas. About one fifth of NFIP policies — generally older structures in high risk areas — are explicitly subsidized by the federal government according to the Congressional Budget Office. However, the subsidy provided by the federal government is greater to the extent that FEMA's estimates of flood risks are outdated or too low (see here page 20).

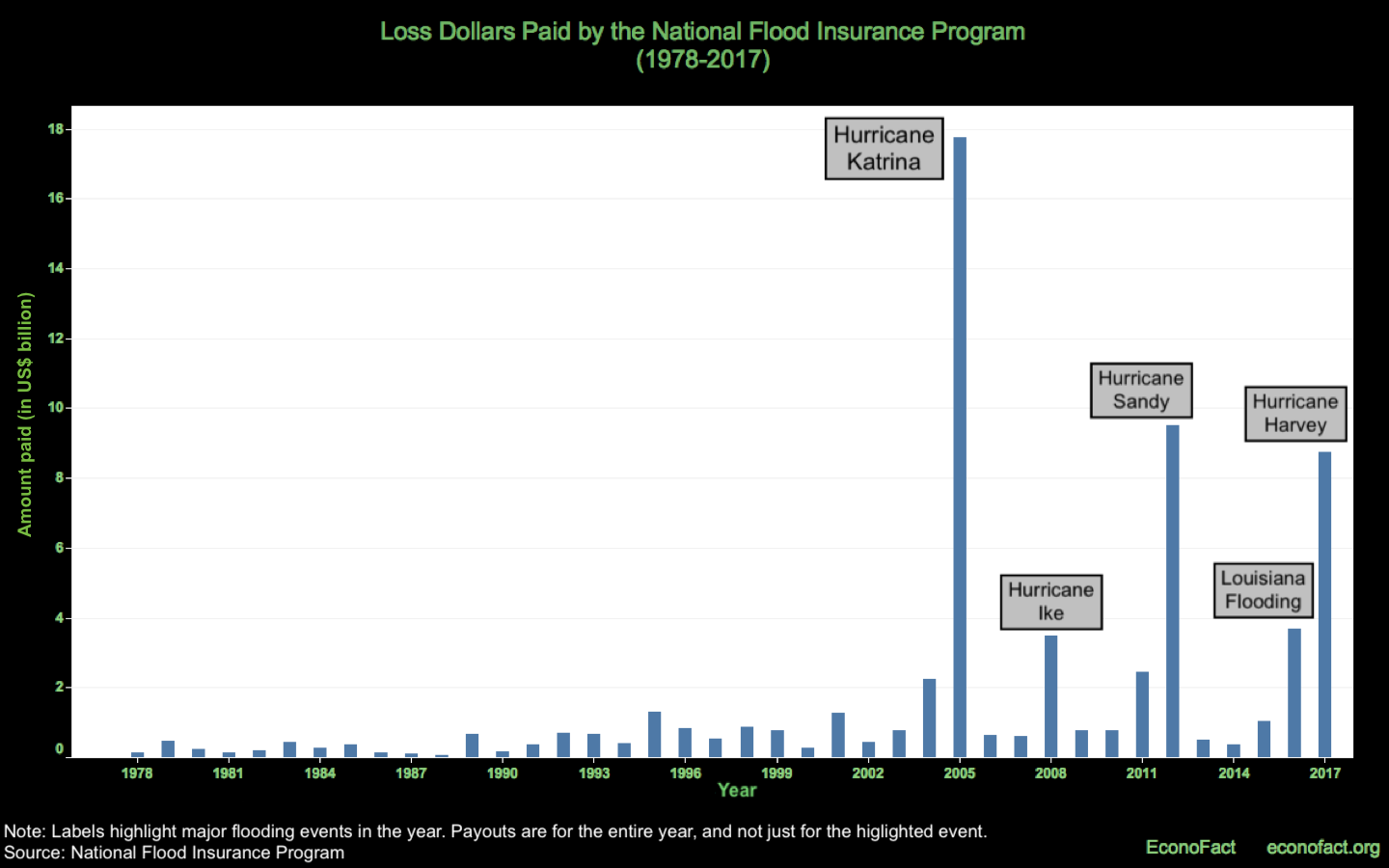

- Over the last two decades, the NFIP has become burdened with enormous amounts of debt. The program has not generated sufficient funds to fully cover losses. This has been exacerbated by several weather events — including Katrina (2005), Sandy (2012), and Harvey (2017) — that have generated losses that dwarf those of the 1980s and 1990s (see chart). Congress had authorized FEMA to borrow from the U.S. Treasury, within certain limits, when the NFIP's revenues fell short. Until the 2005 hurricanes, FEMA had been able to repay the occasional loans, however, as of March 2016, FEMA owed Treasury $23 billion, according to the Government Accountability Office which has listed the NFIP in its High Risk List as a result of the growing imbalance.

- Growing debt and the fact that the increase in sea levels in the last 5 decades has rendered some of the flood maps obsolete, prompted a move to reform the NFIP. In order to make the program financially stable Congress passed the Biggert-Waters Flood Insurance Reform Act in 2012, which planned to eliminate subsidies to flood insurance rates and phase out a number of exemptions. As a result, flood insurance premia were scheduled to increase substantially for many floodplain properties. However, the aftermath of hurricane Sandy and the Great Recession called for a more gradual approach. In response to vigorous public opposition in affected areas, Congress passed the 2014 Homeowner Flood Insurance Affordability Act (also known as Grimm-Waters Act), which repealed some mandates of the 2012 Act and slowed down rate increases (as of April 1, 2015). The reforms also entailed drawing new flood maps. This process is done gradually. For example, the preliminary updated maps for New York were made public in 2012 (but were not yet effective as of October 2018) and the new flood map for Virginia Beach became effective in 2015.

- Do the recent reforms to the NFIP affect housing markets in coastal areas? Increases to flood insurance rates would be expected to result in lower house values for the properties affected, as owners face higher costs. Similarly, properties that see their location re-classified with respect to flooding risk as a result of updated maps would be expected to see changes in their value: Those that are newly classified as being in a high-risk zone would be expected to decrease in value relative to similar properties that are not considered to be at elevated risk of flooding. To assess whether the reforms impacted house prices in coastal flood zones, we matched residential sales for three coastal urban areas in the United States — Miami-Dade county (2008-2015), New York city (2003-2016), and Virginia Beach (2000-2016) — with their FEMA flood maps (see here). We did not find an effect of increases in insurance premia on the values of floodplain properties in Virginia Beach and Miami-Dade as of 2016. There was a reduction in housing values in New York’s flood zone after 2012, but this is more likely to be due to the effects of hurricane Sandy, which hit New York on October of 2012, rather than flood insurance reform (see here). Grandfathering rules and delays in the sale of the properties most affected by the increase in premiums may postpone the effects on sale prices.

- Updated flood maps can impact property prices. Properties that experienced a change in their risk classification by virtue of the updated FEMA flood maps provided mixed evidence. In our data, properties that were newly classified as being high-risk in Virginia Beach and New York did not see a reduction in sale prices. However, houses that were removed from the high risk classification experienced a large price appreciation in both markets, showing that flood maps can impact housing values.Nevertheless, the full effects of the 2012-2014 flood insurance reforms on coastal housing markets may have not yet taken place but could materialize in the future. It may also be the case that owners in high-risk areas have opted for making changes to their properties to make them more flood-resilient in ways that reduce their flood insurance premiums and preserve their value, such as filling in basements, lifting the electrical system to higher elevations, or installing flood vents (see here).

What this Means:

The availability of subsidized flood insurance may have muted the effects of the increase in flood risk in the last decades on housing values. The appropriate policy response to the challenges arising from sea level rise will not be the same everywhere. Fortification and resiliency measures will be appropriate in some areas, but “graceful depopulation” will be the optimal response in other areas. In the latter cases, the NFIP is the most promising tool at the hands of the federal government to incentivize households and businesses to gradually relocate toward less flood-prone areas. The recent reforms to the NFIP go in the right direction. There is a lot at stake. Billions of dollars in damage from future flooding episodes, loss of life and unmeasurable human suffering.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.