How Big is the Problem of Tax Evasion?

Brookings Institution and Tax Policy Center

The Issue:

Tax evasion – the act of not paying taxes that are owed – is illegal and is an underappreciated problem in the United States. About one out of every six dollars owed in federal taxes is not paid. The amount of unpaid taxes every year is plausibly about three-quarters the size of the entire annual federal budget deficit. The rate of income misreporting is significantly higher for income from sole proprietorships and farms, and it is likely higher for high-income households than lower-income households.

Along with the obvious problem of the underfunding of the government, tax evasion raises fundamental questions about the fairness of the tax system.

The Facts:

- Tax evasion can be deliberate or inadvertent and is distinct from tax avoidance. Deliberate evasion occurs when, for example, individuals do not report income or do not pay taxes. But unintentional mistakes made in filing tax returns can also give rise to inadvertent tax evasion. Illegal tax evasion is distinct from tax avoidance, which is taking advantage of legal ways to reduce tax liability, such as using the mortgage interest deduction. However, due to ambiguities in the law, differences in interpretations, the creation of new circumstances, and other factors, there can be some gray areas where it is difficult to distinguish between avoidance and evasion.

- The standard measure of tax evasion is the "tax gap." The tax gap is the amount of taxes that are owed but are not paid in a timely or voluntary manner. The Internal Revenue Service (IRS) collects information on the size and composition of the tax gap by conducting periodic studies that draw on a number of sources. For the major component of the tax gap—underreporting of individual income taxes—the IRS collects information each year from examinations of a random sample of taxpayers. The most recent tax gap report was published in 2016 for tax years 2008-2010. The net tax gap (which accounts for late payments made either voluntarily or as a result of enforcement action) averaged $406 billion per year from 2008-2010. About 16 percent of taxes went unpaid. This was equivalent to 2.8 percent of annual gross domestic product (GDP) and 18 percent of annual federal revenues during that period. If the tax gap stayed constant relative to GDP since then, it would have reached $560 billion by 2018. If it stayed constant relative to tax revenues, it would have reached about $600 billion. For perspective, the federal budget deficit in 2018 was $779 billion, so the tax gap could plausibly have been 70-80 percent as large as the entire budget deficit in 2018.

- Evasion rates differ across different types of taxes and are relatively high for income taxes. In 2008-2010, the individual income tax accounted for about 72 percent of evasion, but only about 44 percent of taxes paid. In contrast, payroll taxes, which are the second largest source of government revenue in the United States, have a much lower evasion rate. Payroll taxes — paid on the wages and salaries of employees and used to finance social insurance programs such as Social Security and Medicare — and self-employment taxes accounted for about 19 percent of evasion, but 39 percent of taxes paid. The corporate tax evasion ratio was relatively low compared to income taxes, since corporate taxes accounted for both about 9 percent of evaded taxes and 9 percent of actual revenues.

- Tax evasion rates may well be higher for high-income households than middle-income households. Data from 2001 – admittedly, some time ago – finds that households in the top income decile accounted for 61 percent of tax evasion, but just 44 percent of earned income, a ratio of about 1.4:1. (The evasion rate was even higher for those at the very top of the income distribution: Those in the top 1 percent accounted for 28 percent of tax evasion but 18 percent of income, a ratio of about 1.55:1.) The bottom half of the income distribution accounted for just 12 percent of evasion and 14 percent of income, a ratio of less than one. Although the information is dated, it is likely to still be the case that evasion rates are higher among high-income households since income from capital, especially self-employment or pass-through businesses, has increased over time and is both highly concentrated among high-income households and associated with high evasion rates.

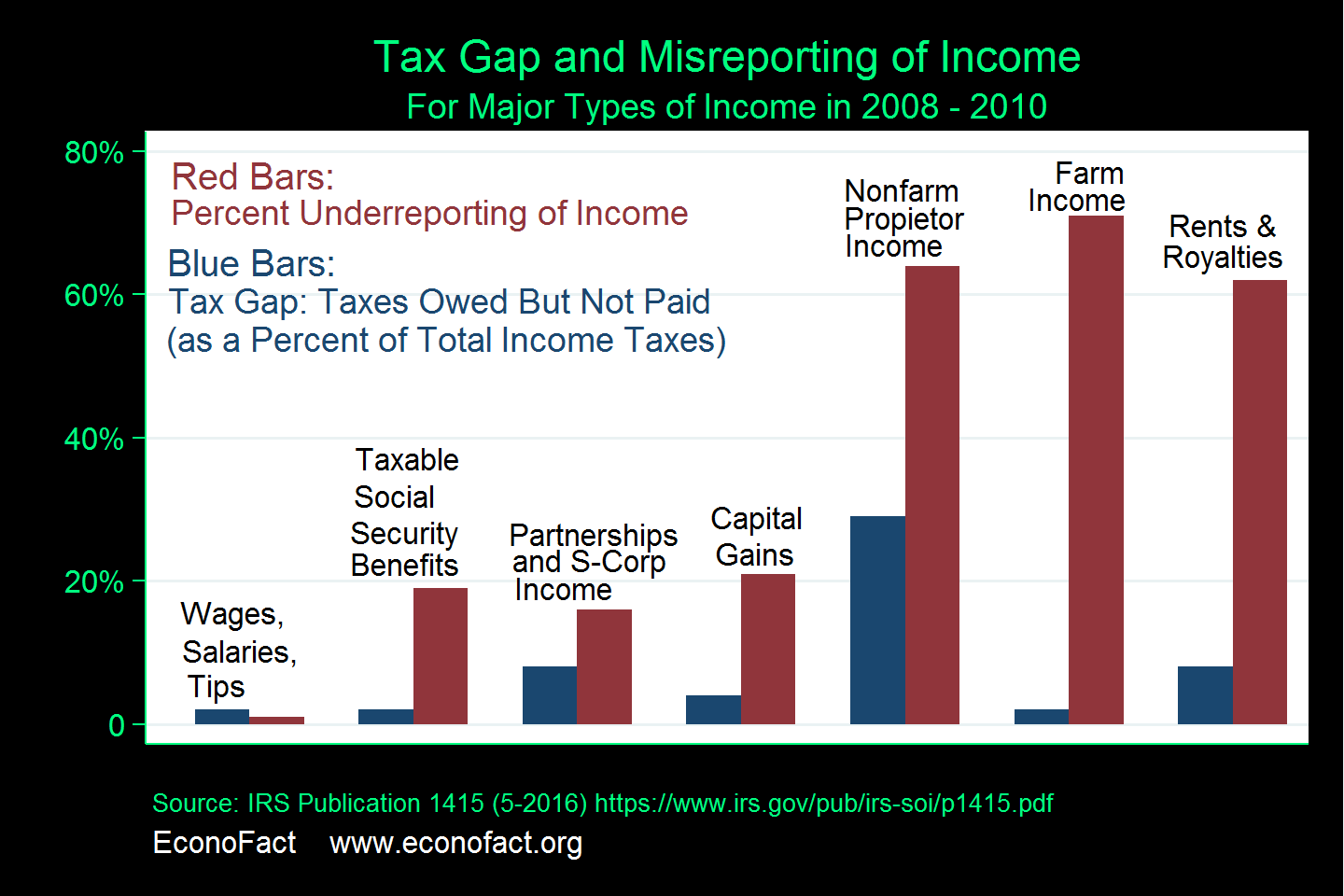

- Evasion rates depend on the tax system’s administrative features. Compliance is highest when third parties report income information to the government and withhold taxes. For example, only 1 percent of income from wages and salaries is misreported on tax forms (see chart). Compliance is lower when a third party reports the income but doesn’t withhold taxes. Some 16 percent of partnership income and 21 percent of net capital gains are unreported to the government by the recipient. The lowest compliance rates occur when there is no cross-party reporting of income and no withholding. This helps explain the estimate that more than 60 percent of farm income and sole proprietorship income is not reported to the government. Underreporting of sole proprietorship income is estimated to account for almost 30 percent of the individual income tax underreporting tax gap.

- The Internal Revenue Service (IRS), which is responsible for enforcing the tax rules, has seen its funding and employment decrease. IRS funding has fallen by more than 12 percent in inflation-adjusted terms from fiscal year 2008 through fiscal year 2017, and IRS employment dropped by more than 15 percent over the same period. The enforcement division of the IRS has had the largest percentage decline, even as Congress has requested the IRS to assume new administrative and enforcement responsibilities related to interpreting and implementing the 2017 tax overhaul, the Affordable Care Act, the American Opportunity Tax Credit, and the Foreign Account Tax Compliance Act.

- In the face of lower funding and increased responsibility, the IRS has conducted fewer audits and provided lower-quality taxpayer service. Audit rates have fallen roughly in half over the past two decades; the IRS audited 0.6 percent of individual returns and 1.0 percent of corporate returns in 2017, compared to 1.0 and 2.1 percent, respectively, in 1998. Likewise, only 38 percent of taxpayers who called the IRS received requested assistance in 2015 as compared to 70 percent in 2011. The average telephone wait time over the same period increased by more than 17 minutes. More generally, the IRS is falling farther and farther behind state-of-the-art computing. Many of the computer systems and programs are antiquated and they are using computer applications from the 1960s.

- It is widely believed that increased funding for enforcement activities would more than pay for itself. Using data from 2017, the IRS estimates that each dollar of investment in enforcement programs yields $12 in additional revenues, while each dollar in the overall IRS budget increases revenues by about $5. In addition, targeting added enforcement activities on high-income households would yield more revenue than using the resources to audit lower-income households.

What this Means:

People who evade taxes are not just cheating the government, they are also stealing from their neighbors who are following tax laws and regulations. Cutting IRS spending, as policymakers have done in recent years, is penny-wise and pound-foolish. While it is unreasonable to expect to receive all taxes that are owed the government, the IRS could do far more if it had the resources. Adequately funding the IRS and making a variety of structural tax changes would help raise collection of taxes owed and mitigate public concern that the system may be rigged in favor of the wealthy. In his FY 2020 budget, President Trump proposed $15 billion to expand tax enforcement over ten years, which was estimated to yield a direct net revenue increase of $33 billion over the same period. The initiative could raise further revenue by encouraging a higher level of voluntary compliance. Additional compliance measures in the FY2020 budget proposal include improving oversight of tax preparers, increasing IRS authority to correct tax return errors, and bolstering information reporting. While the net savings due to these proposals would be a good start, they would only close a small fraction of the tax gap over the next decade. Further changes, listed in a 2006 IRS report, could reduce the tax gap, even without structural changes in the tax law. These include strengthening reporting requirements, expanding IRS access to reliable data, enhancing examination and collections authority, setting penalties at more appropriate levels, and improving the technology used by the IRS. The financial returns from these investments merit their careful consideration. Perhaps just as importantly, reducing the tax gap would improve the public’s faith that the system is not rigged.

Topics:

Tax PolicyLike what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.