SNAP: A Temporary, Fraud-Resistant, Family Friendly Policy

Tufts University

The Issue:

Large cuts and restrictions on America’s anti-poverty programs have been proposed and are under debate in Congress, motivated in part by legitimate concerns that providing assistance could encourage fraud, create dependency, and distort behavior. This worry has been most forcefully articulated by Paul Ryan, Speaker of the House, as the need for “an incentive-based system where people want to get up and make the most of their lives, for themselves and their kids. We don't want to turn this safety net into a hammock.”

The Supplemental Nutrition Assistance Program (SNAP) adheres to Speaker Ryan’s blueprint, using economic incentives to provide temporary aid in cost-effective manner, with less fraud than other major U.S. assistance programs.

The Facts:

- The Supplemental Nutrition Assistance Program (SNAP) program currently reaches about 42 million Americans each month, down from the post-recession peak of almost 48 million in December 2012. Participation is dropping as the economy recovers, with enrollment estimated to have declined by about 5 percent over the past year. Beneficiaries receive State-issued electronic benefit transfer (EBT) cards, replenished monthly with an average of $125 per person for use to buy food at eligible grocery stores. SNAP is funded through the Farm Bill, legislation that is negotiated every 4 to 5 years, and is currently up for renewal in 2018. It is expected that particular scrutiny will be given in Congress during the negotiation process to SNAP (for details see this EconoFact memo.)

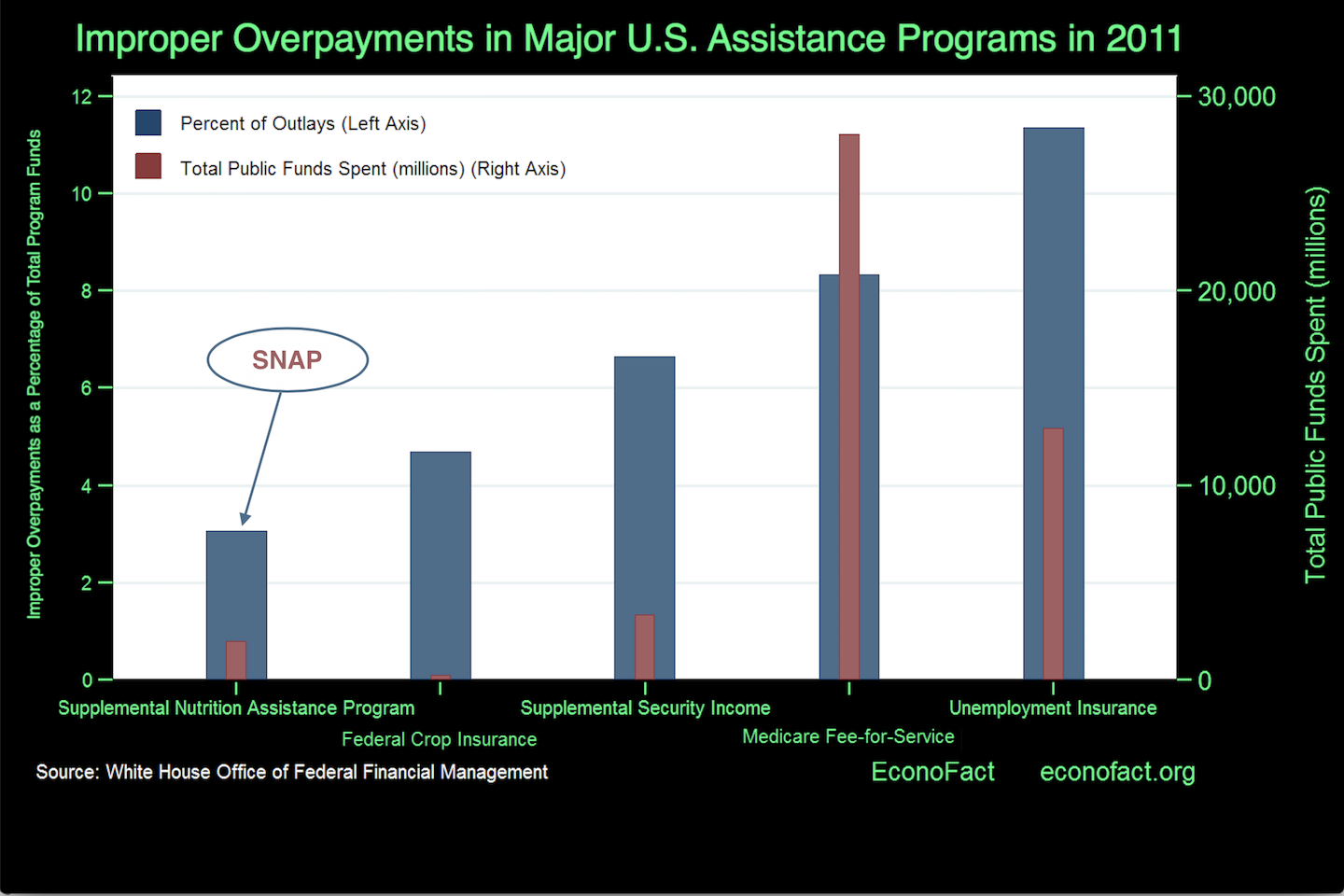

- SNAP has low rates of fraud and abuse. The U.S. Department of Agriculture’s most recent study of redemptions found more than 98 percent of benefits are used as intended for the purchase of eligible items. The White House’s Office of Management and Budget compares payments to eligibility, and most recently found that SNAP had a rate of total overpayment above mandated benefit levels of 3 percent. In contrast, USDA crop insurance had overpayments of almost 5 percent, Supplemental Security Income (SSI) disability had overpayments of 7 percent, Medicare had overpayments of 8 percent, and Unemployment Insurance had an overpayment rate of 11 percent (see chart). Due to the different program sizes, total overpayments in Medicare are 14 times larger than in SNAP, and overpayments in Unemployment Insurance are 7 times larger. Overpayments are low because criteria are clear. And fraudulent redemptions are low because the system offers few incentives to cheat: benefit levels are deliberately calculated to be less than the value of food that families would want to consume each month, so it is in each recipient’s interest to use the card as intended. Recipients spend out their EBT balance early each month and must then turn to other sources of food, consuming less healthy foods or skipping meals entirely at month-end, until the EBT card is replenished. This behavior reveals that beneficiaries actually need to use the cards for food, thus limiting the incentives for resale or trafficking.

- SNAP is primarily temporary aid, with median length of SNAP participation falling to 8 months in the 1990s then rising to 12 months during and after the 2008 recession, before falling again. Able-bodied adults without dependents who do not work are eligible for only up to three months every three years. Most SNAP recipients are already working, and exit SNAP voluntarily when their incomes rise. Benefits taper off with additional earnings at low-income levels, and the most recent estimate of SNAP recipients’ average marginal tax rate on earned income is 24 percent. This means that for every additional dollar a SNAP recipient earns, her benefits decline by only 24 percent. This is lower than the marginal tax rate on earned income for people with higher income levels, which start at 25 percent and rise to a top rate of almost 40 percent. SNAP rules interact with tax laws in ways that let recipients keep a slightly larger fraction of their earnings than other Americans, thus avoiding incentives that would promote dependency and discourage paid work.

- SNAP supports meals at home, helping families cook and eat together instead of relying on fast food away from home. Benefit cards can be spent only at eligible grocery stores, where they can be spent on any food to be prepared and consumed later. Hot foods or other items to be eaten in the store are excluded, as are non-food items, alcohol and tobacco. There is no differentiation among types of food, and the program does not generally provide incentives for healthier or less healthy items. Participants do tend to use their higher purchasing power to buy more nutritious foods early in the month until benefits run out, but the main effect is to promote meals at home instead of fast food or other sources away from the family.

What this Means:

SNAP is already the temporary, low-fraud, family-friendly safety net that conservatives would like to see. It helps families with children bounce back from periods of hardship — more like a trampoline than a hammock.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.