Supply Disruptions and Energy Security

University of California, San Diego

The Issue:

As the war in Iran continues, the costs and risks to the global economy are mounting. Central to these risks are constraints on the safe flow of oil by tankers through the narrow Strait of Hormuz. In good times, about one-fifth of world oil supply travels the Strait. As the Strait closed to nearly all traffic and the risks of war drove insurance rates to punishingly high levels, some oil has been redirected to other export routes, including sea lanes in the Red Sea that are vulnerable to attacks from the Houthis. Iran has allowed some ship-borne cargoes destined for China, India and a few other nations but the United States is now instituting its own blockade of these ships. At the war’s peak of disruption (so far), about 8 percent of global supplies were unable to find any exit from the Persian Gulf in what has been the largest oil disruption in modern history. These facts have been a reminder that “energy security” is often taken for granted — until it does not exist. A new wave of efforts to boost energy security will likely follow, although many of the important initiatives — such as protecting sea lanes, investing in alternative export routes, and building stronger mechanisms for coordinating stockpiles — will require levels of international cooperation that are hard to muster these days.

The impact of the shock so far has been dampened in part due to past policy and market actions.

The Facts:

- Despite reductions in oil dependence since the 1970s, and rising oil production in the United States, reductions in worldwide supply still have important adverse consequences on the US economy. At the time of the first oil shocks in the early 1970s, every $1000 in global economic output (2015 prices) was associated with burning one barrel of oil; by the eve of the Covid pandemic that number had dropped by more than half. Most of that decline is due to improved efficiency in energy systems and a shift in economic output from energy-intensive heavy industry to services. In addition, the use of oil in many applications such as electric power generation has been nearly eliminated. Nonetheless, oil remains vital for some sectors and activities — most notably in transportation, where liquid fuel with high energy density that is easy to store on board in tanks has unrivaled convenience. The United States has become a much more important source of oil production since the 1970s largely due to the revolution in producing oil from shale. Nonetheless, the price that US consumers and businesses pay, and which US oil producers receive, still largely tracks the worldwide price of oil.

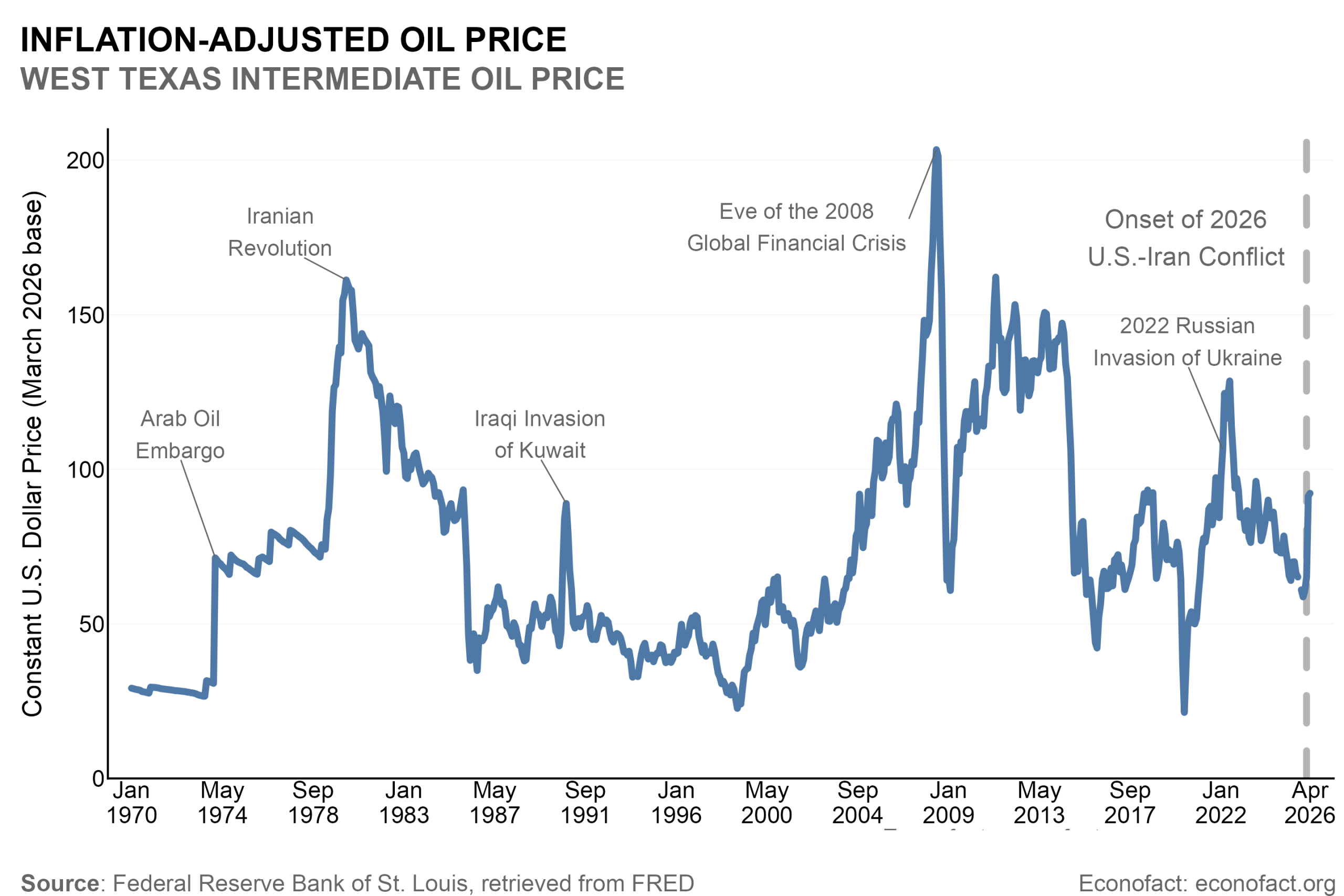

- Global commodity markets have mitigated the price spike of oil but physical shortages are starting to have a bigger impact on those markets. There is no singular global price of oil, but most analysts look to a handful of widely traded oil types that, more or less, move together. Among those with the longest track record is West Texas Intermediate (WTI). During the oil shocks of the 1970s, the West Texas Intermediate oil price rose by more than 130 percent between December 1973 and January 1974 and by 150 percent between April 1979 and April 1980. By contrast, during the first month of the Iran war WTI rose only about 50 percent (see chart). One of the reasons for this relatively muted response is that the markets for oil and refined products are deeper and more integrated globally than a half-century ago. But prices will rise further as shortages become more acute. Producers and refiners started to throttle back operations almost immediately after the start of the war; that strategy worked for a while, but shutting operations will be more costly and take longer to reverse as the war continues. Furthermore, attacks that damage infrastructure such as the pipeline that takes oil west across Saudi Arabia to the Red Sea and to various refineries, as well as other war-related damage, will also limit the supply of oil and petroleum products. The effects of physical shortages are apparent in looking at the prices of different types of oil that have different properties (e.g., viscosity and sulfur content, which affect the cost and ease of refining oil into products) and locations. For example, the blockage of oil that would have travelled through the Strait of Hormuz has led to the immediate price of a benchmark for North Sea oil called “forties” to trade at 50% above typical global benchmark crude because oil from it could be reliably delivered at locations (European refineries) that urgently need physical barrels of oil. (By contrast, WTI measures oil prices at a location that is already abundantly supplied.) In addition to the variability in prices created by the physical deliverability of oil during times of shortage, there have been big differences between current and future prices, with the latter often lower because the futures markets reflect an expected proximate end to the war.

- Coordinated releases of oil from stockpiles have also limited the increase in prices. Prior to the war, about 1.2 billion barrels of oil were in various forms of publicly owned or publicly managed stockpiles. Governments agreed to release 400 million barrels in total (of that, 172 million barrels from the U.S.) as the war continued. Physically putting that oil on the global market takes time —about four months — but the prospect helped calm the markets. By mid-April a failed ceasefire followed by the United States announcing it would fully block vessels that Iran would otherwise allow to pass through the Strait of Hormuz has increased pressure for additional releases from stockpiles. This could be a source of tension among nominal allies because some countries acutely dependent on oil from the Gulf, such as Korea and Japan, will be wary of over-releasing lest that yield even bigger vulnerabilities in the future. China has its own stockpiles and has managed its releases for its own consumption, but this still affects the global market price. To a point, China has been able to reduce its vulnerabilities by arranging to have China-bound cargoes given safe passage through the Strait. (India has obtained some cargoes of oil and LPG using similar methods). These autarkic strategies seem likely to fail if the US imposes a full blockade on the Strait. That said, one of the central challenges in any strategy for economic sanctioning is finding ways to apply sanctions that cause maximum harm to enemies while minimizing harm to oneself and allies. The harm to India so far has been palpable and that will erode future prospects for US-India cooperation.

- The closing of the Strait of Hormuz has also affected natural gas markets. Over a period of several decades natural gas has become central to electric power generation and many other industrial applications around the world. One advantage of natural gas is that it burns much cleaner than coal. Natural gas markets are more segmented than oil markets and therefore have greater price differences across locations. Natural gas is more easily transported by pipeline than by ship and is impractical to reroute overland — factors that limit its worldwide transportation. There is a shift towards greater global integration of natural gas markets with the increase in tanker shipment of liquefied natural gas (LNG). About 13% of global gas consumption moves as LNG, but that fraction is rising and for countries such as Japan and South Korea that have few or no other sources of gas, LNG in effect sets the price of local gas. About one-fifth of global LNG supplies come from Qatar. This supply was fully lost when passage through the Strait of Hormuz became dangerous and was closed. This has raised prices and created scarcity in places like India where fertilizer plants have been throttled back and other uses of gas curtailed, such as in cremations. Cargoes in the Atlantic basin have found it profitable to shift to Asia. Qatari production will not fully rebound quickly after the war because its facilities have been heavily damaged and full repairs will likely take years. The creation of new LNG facilities, including the liquefaction plants, ships that can transport LNG, and reception equipment in ports, depends upon whether long-term suppliers are confident in the prospects of obtaining a good return on these capital-intensive investments.

- High oil prices and insecure supplies are motivating responses. In a few countries, notably the United States, political leaders are focused on boosting and diversifying supplies of fossil fuels. Most of the world’s other countries, however, will give renewed attention to energy efficiency and to shifting to alternatives such as biofuels, synthetic fuels and electricity. Most biofuel options currently do not scale well because they involve growing fuel crops such as corn or sugar for ethanol, or canola for diesel and jet fuel, which are both costly and often harmful to the environment. Recycled oils are playing a small role, such as for production of sustainable aviation fuel and some diesel biofuels, but recycling doesn’t much scale to the needed volumes. Synthetic fuels used to be made from coal — a highly polluting and costly option — and now could be made from a variety of different chemical pathways that yield hydrogen, green methanol, ammonia or other options. Many intriguing new options for chemical synthesis exist, although none is poised to scale quickly at reasonable cost. The demand for electric cars and small trucks is surging and now accounts for more than one-fifth of new vehicle sales and 4% of the vehicles on the road worldwide. China is the largest global market by far, accounting for about one-third of all EV sales. But electrification is currently unavailable for the heaviest trucks and long-distance ships and aircraft because of the need for large and heavy batteries. The increasing use of electricity has had little effect on reducing oil consumption; electric vehicles have lowered oil consumption by perhaps 1-2 million barrels per day, a small fraction of the 103 million barrels consumed daily. And some of the electricity needed to power them is generated by natural gas. High prices for natural gas should elicit a stronger response because there are many other options for making electricity. But even those power grids that rely on solar and wind power still rely heavily on other power sources, such as natural gas, that are less variable and intermittently available.

What this Means:

The impact of the shock so far has been dampened in part due to the accumulation of past policy and market actions. Modern economies are much more efficient than in the 1970s. The ability to stockpile and coordinate the release of oil reserves on a global scale was developed in response to the 1973-74 oil crisis. Active efforts to reduce dependence on oil such as through deployment of electric vehicles — a policy rooted not just in concerns about energy security but also climate change — has further decreased world oil dependency relative to the prior crises. But the global political effects of the current war are seismic and will likely make it harder to address future energy security and other global problems. In theory, a major crisis like this might bring countries together around the need for joint action, as happened in the 1970s with the first oil shocks or after 9/11 with the global war on terror. Today’s world, however, is one with fragmenting international institutions and declining trust in the hegemon (the US) to govern in the collective interest. The current event may be a harbinger of future challenges. Hormuz is the biggest choke point in global supply, but there are others. The doomsday scenario for global oil markets has long been focused on Hormuz, but other choke points have included Russian pipelines (now sanctioned, but mainly operating because the world needs the supply) and the narrow Red Sea (and its narrower opening) that has been the locus of earlier attacks on cargoes by Houthi rebels. Other places of interest include the busy sea lanes of Malacca, although they can be bypassed by sailing longer distances.

Topics:

Energy PolicyLike what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.