Taxing the Rich (UPDATED)

Reed College

The Issue:

The coronavirus has ravaged the economy, and today’s high unemployment and extremely low interest rates provide ample justification for budget deficits. Still, in the years ahead, many feel that the U.S. government needs more revenue, in order to fund urgent fiscal priorities such as infrastructure, climate change response, healthcare, and education. As policy-makers search for new revenues, those at the top of the income distribution are natural targets for tax increases, since their incomes have grown the most rapidly in recent decades.

Tax increases for those at the top can achieve two aims: providing revenue resources from those that have experienced the greatest gains in income, and countering economic and social inequalities.

The Facts:

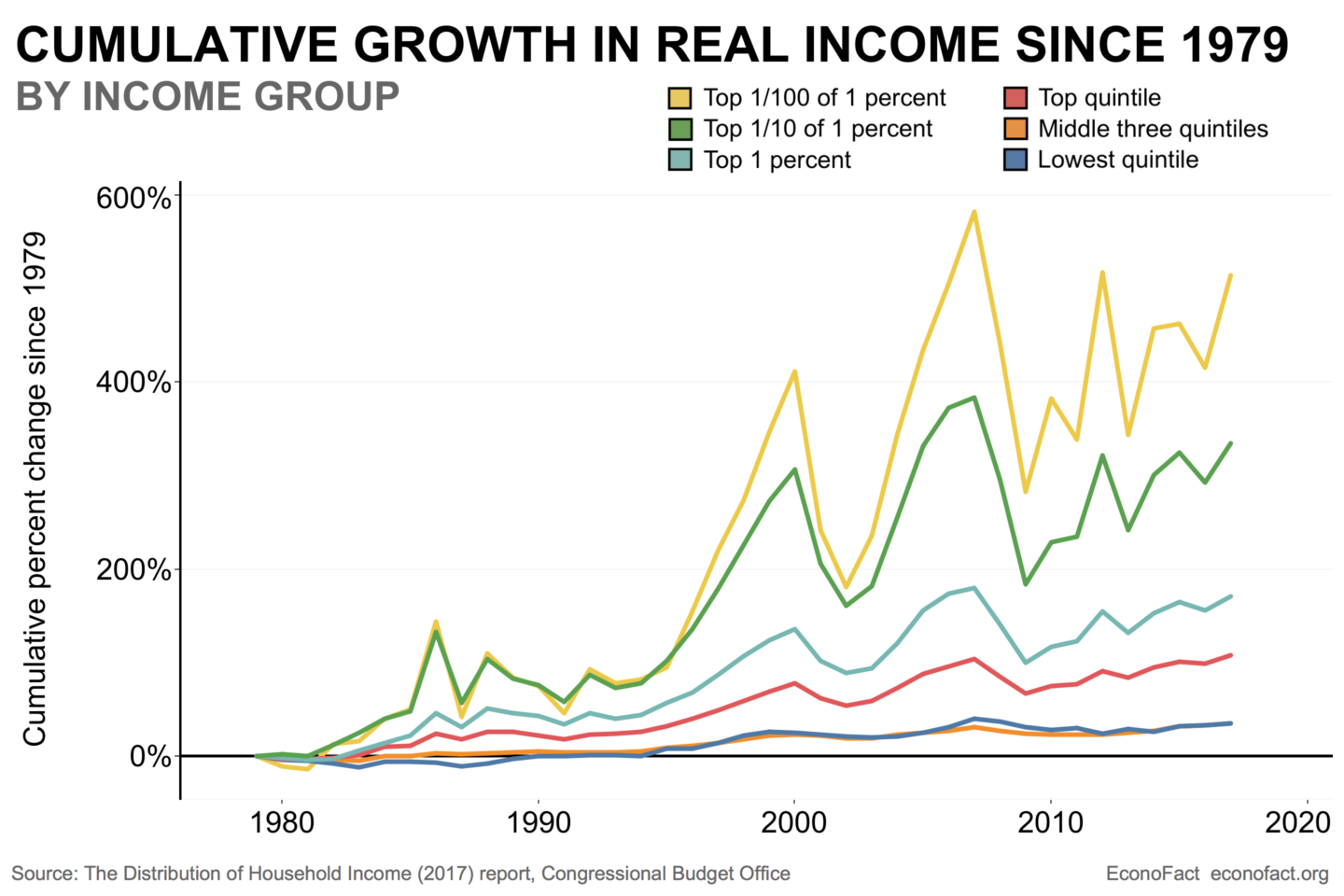

- Economic inequality has increased dramatically in the United States, and because of this, gains from economic growth are often not shared evenly. Many Americans have not felt the benefits of strong GDP growth in recent decades, as thirty-five years of rising income inequality have concentrated income growth at the top of the distribution (see chart). At the same time, incomes in the bottom 80 percent of the distribution (bottom 4 quintiles) have seen very little gains compared to those at the top. Income growth for those in the top 10 percent, and especially the top 1 percent and the top 1/10 of one percent, has been enormous: Over this time period, cumulative income growth has exceeded 300 percent for those in the top 1/10 of 1 percent. Moreover, the coronavirus pandemic and the associated economic downturn have further increased economic disparities over the past year. But widening inequality is not inevitable. In the 35 years after World War II, economic growth was widely shared, and real incomes doubled for those in the bottom 90 percent of the distribution while growing more slowly for those at the top.

- Despite increasing inequality, recent changes in tax policy have generally not made our tax system more progressive. While the federal income tax system is progressive overall, it has failed to counter widening inequality, and some of our past tax policy changes have in fact exacerbated inequality. The Tax Cuts and Jobs Act concentrated tax cut benefits at the top of the distribution, and prior decades of cuts in tax rates (for both labor and capital income) have also exacerbated income inequality. These trends have strengthened the case for increasing tax burdens on those at the top of the distribution — both as a way to increase revenue, since much of income growth has materialized at the top of the distribution, and to counter widening inequality. While there are disagreements regarding the extent to which government policy should address inequality, many observers note that economic inequality can be harmful for society; that it leads to the concentration of political and economic power, and it reduces the extent to which American society feels a sense of shared economic prosperity.

- Taxing capital is an important part of taxing the rich. Capital income is more concentrated than labor income, and it is a growing share of national income. Thinking amongst economists about capital taxation has been evolving. In past decades, many economists emphasized the large efficiency costs of taxing capital because capital taxation discourages savings and investment — hurting the economy in the long run. But, early arguments about the inefficiency of capital taxation were often based on overly simplistic theoretical models; more realistic models suggest higher capital tax rates, similar to those that apply to labor. The case for taxing capital is particularly strong once one recognizes that large parts of “capital” income are in fact rents, or above-normal returns to investments that are received by those with market power or luck.

- Taxing capital is an important part of a healthy tax system. The wealthiest taxpayers often have some discretion in terms of the form in which they earn their income. If labor income is taxed more heavily than capital income, those with discretion may choose to receive more of their income as capital income. (For example, entrepreneurs may choose to take more of their compensation as capital income rather than as wages.) Thus, there are good arguments for taxing income from labor and income from capital at the same rate for particular taxpayers.

- The corporate tax is an important part of taxing capital. Currently, about 70 percent of U.S. equity income goes untaxed at the individual level, and the taxable share of U.S. corporate equity has declined dramatically in recent decades. And, while there is some disagreement about the incidence of the corporate tax, most economists assign the vast majority of the corporate tax burden to those at the top of the income distribution. Thus, proposals to improve our revenue collection from the corporate tax are an important part of taxing the rich. Unfortunately, the recent Tax Cuts and Jobs Act moved the tax system in the other direction, as corporate tax rate cuts were undertaken without sufficiently broadening the tax base. As a consequence, corporate tax collections are shrinking in both absolute terms and as a share of GDP.

- Increasing tax burdens on the rich was an important theme during the democratic primary, and Vice President Biden has proposed about $3 trillion in tax increases over the next decade, falling largely on the richest Americans. Biden’s suggested tax increases include higher top rates on income, increased capital gains taxes (alongside taxing unrealized gains at death), increased estate taxes, and increased business taxes. The corporate tax rate would increase to 28 percent (below the 35 percent rate before the Tax Cuts and Jobs Act but above the current 21 percent rate), and a strong minimum tax would counter the incentive for multinational companies to move jobs or paper profits offshore. Biden’s plan also addresses low-end incomes by increasing the child tax credit, and making that credit fully refundable, although that provision is (at present) temporary. Also, new tax credits are proposed for renters, for first-time home-buyers, and for dependent care expenditures.

- In theory, increasing taxes on investment income through higher rates on dividends and capital gains should be similar to a financial wealth tax, since investment income is simply a return on one’s stock of financial wealth, and tax rates could be adjusted to reach the same burden. One difficulty with investment income taxes is the fact that capital gains are only taxed upon realization (when they are sold), which gives investors an incentive to keep financial assets in order to benefit from the tax-free accumulation of returns. Therefore, some have suggested taxing capital income as it accrues, including a recent floating of this idea from Senator Ron Wyden as well as more scholarly proposals. This would either require mark-to-market taxation (taxing investment income as it is earned, even if the asset is not sold), or deferring tax until sale, but assigning an interest charge that would accrue on the prior tax due. A final option is implementing a withholding tax system that would require regular payments (or a tax lien), with the reconciliation of final tax bills when assets are sold. Such proposals raise important implementation issues, although today’s digitalization of financial information helps solve some problems.

- Taxing unrealized capital gains at death would also be an important reform. At present, when a capital asset is inherited, those that receive it avoid capital gains tax on the unrealized gain, as the new basis is the price of the asset upon transfer. For example, a person who buys stock priced at $200 and sells it for $1000 has to pay capital gains taxes on their $800 gain. But, if the person dies and bequeaths the stock, the heir can reset the value (basis) of the stock to the $1,000 price upon transfer — meaning that if they sell it, they do not pay taxes on the $800 gain. This reform would reduce the incentive to hold assets in order to delay capital gains tax upon realization, and it also prevents capital income from going entirely untaxed.

- Biden’s proposal to increase estate taxation will affect less than one percent of estates. Very few estates pay the estate tax (less than one-tenth of one percent at present), and there is little evidence that estate taxation affects savings incentives for decedents or harms businesses or farms. Also, one might usefully consider incentive effects on heirs, since inheritance can dampen heirs’ incentives to work and save. Another important idea for reform in this area is to transform the estate tax into an inheritance tax, again exempting all but the richest taxpayers.

- While some have informally suggested increasing tax rates at the top as high as 70 percent, such high tax rates are likely to be more distortionary than tax increases at lower levels. Also, since well-off taxpayers have discretion about the form in which they earn their income, it is best to avoid large differences in tax rates across different forms of income. At present, there is substantial room to raise revenue on the rich by simply closing the loopholes affecting corporate income and the income of top taxpayers. Indeed, the Biden plan would raise more than $3 trillion in new tax revenues from these sources over ten years.

- While a recession is not usually a good time to raise taxes, there are still several good reasons to consider tax increases in the near term. First, if new tax revenues from the rich are used to pay for increased stimulus for poorer Americans, on net that will stimulate the economy by increasing overall spending. Since the poor spend more of each additional dollar than do the rich, increasing the progressivity of our tax system increases aggregate demand. Second, higher business taxes will be automatically delayed until companies are earning profits, since companies with losses owe no tax, and they can also use past losses to offset future tax burdens. However, those companies currently earning profits due to market power or luck (such as Amazon and Peloton) can easily afford to pay some of their pandemic profits in tax now. Third, many tax increases (such as increased estate taxes, loophole closures, or enhanced enforcement through improved IRS resourcing) have little to no impact on the incentives that drive economic growth, yet such tax increases would still provide important sources of revenue.

What this Means:

In recent decades, gains in national income have failed to reach many Americans due to increasing income inequality; countering such trends requires increasing the progressivity of our tax system. Proposals that seek to reduce tax avoidance and harmonize the tax treatment of different types of income are likely to raise more revenue at lower rates than more narrow proposals. Many new proposals provide a useful starting point, but they all need careful consideration in order to be ready for implementation. It is also important to remember that economic inequality is not just a “top end” problem. The tax system can also usefully help those at the bottom of the income distribution who have experienced stagnant wage growth in recent decades. Proposals to expand the earned income tax credit do just that, by subsidizing the wages of low-income workers. Pairing an expansion of the earned income tax credit with careful, efficient methods of taxing the rich would tackle economic inequality from both ends.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.