Policy Implications from Rising Economic Inequality

Reed College and University of California, Berkeley

The Issue:

A marked increase in income inequality has been a defining characteristic of the U.S. economy of the past several decades. Progressive tax policy and a social safety net that invests in those at the bottom of the income distribution play a role in mitigating widening inequality in the United States. However, policy has not reacted to the widening gap between rich and poor with countervailing responses in these policy areas. In fact, changes to the tax system and to the safety net over the past couple of decades have, in many cases, gone in the opposite direction. The recent policy changes introduced by the 2017 Tax Cuts and Jobs Act are likely to exacerbate existing trends of increasing income inequality.

Tax policy and the social safety net play a role in mitigating inequality, but policy in these areas has not shifted to address the widening U.S. income gap.

The Facts:

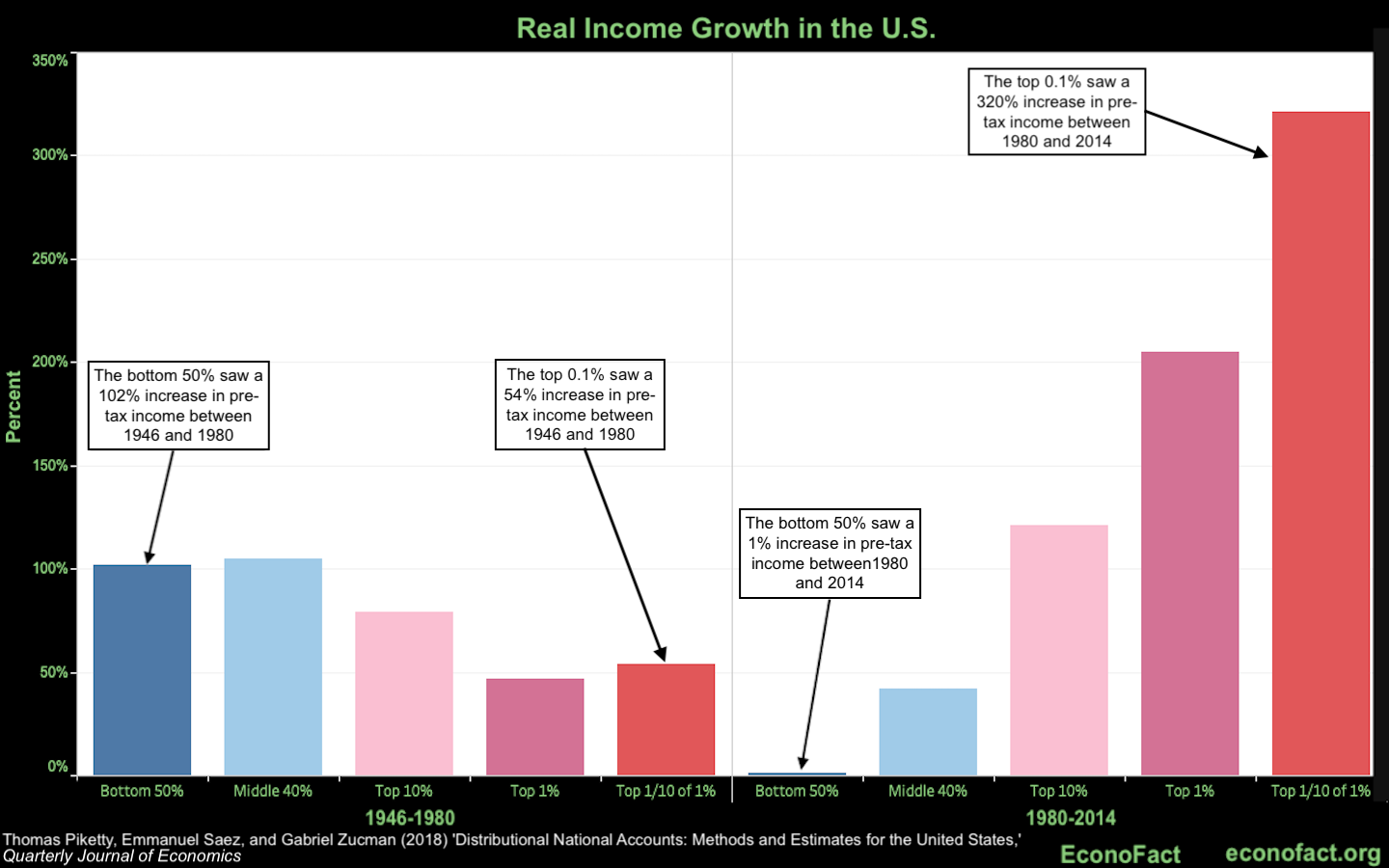

- In the previous 35 years, the United States has faced both increasing income inequality and wage stagnation for many workers. It was not always so. In the 35 years prior to 1970, wage growth was faster at the bottom of the income distribution than the top, and inequality subsequently lessened. Growth in GDP lifted all boats. But since 1980, it has been a different story. Most GDP growth has disproportionately benefited those at the top of the income distribution, leaving workers lower in the distribution behind (see chart). The average pre-tax income of the bottom 50 percent of adults has stagnated since 1980 while the share of national income that went to the top 1 percent increased from about 12 percent in the early 1980s to 20 percent in 2014 (see here).

- On the whole, taxes and transfers make the distribution of income in the United States more equal. Because government transfers go predominantly to lower-income households, income is more evenly distributed when you take transfers into account. And, because higher-income households pay a larger share of federal taxes than lower-income households do, after-tax income also is more evenly distributed than before-tax income. For instance, if you consider after-tax income, the bottom 50 percent saw slightly larger real income growth between 1980 and 2014 of 21 percent. However, this still bears no comparison to the after-tax real income growth of the top 1 percent; incomes for this group nearly tripled between 1980 and 2014 (see Table 2).

- Our tax and transfer policies together reduce the poverty rate by 13 percentage points for all persons and 11 percentage points for children. Declining and stagnating wages lead to increases in poverty and near poverty; the social safety net helps to ameliorate the implications of the labor market for less skilled workers. The most important policies for reducing child poverty include the Earned Income Tax Credit (EITC) and the Supplemental Nutrition Assistance Program (SNAP), also known as food stamps (see here). However, the United States spends far less on reducing child poverty than other countries – the U.S. spends about 0.6 percent of GDP on “Family Benefits” compared to 2.1 percent of GDP for OECD countries as a whole, according to the OECD.

- Ameliorating the impact of poverty on children, particularly at younger ages, is likely to have an impact that extends well into the future. Recent research shows that providing more social assistance to families when children are young, through Medicaid the Earned Income Tax Credit and Food Stamps, leads to better adult outcomes including human capital, health and economic self sufficiency (see here for a review of studies). For example, research finds that when an expecting mother has access to food stamp benefits during her pregnancy, particularly her third trimester, it decreases the likelihood that her baby will be born with low birth weight — an outcome associated with poorer health and labor outcomes in adulthood. Indeed, research has found that having access to nutrition support before birth and in early childhood leads to a significant reduction in the incidence of obesity, high blood pressure, heart disease, and diabetes in adulthood (see here). To the extent that expenditures directed towards reducing poverty in children have long-term impacts, they have the potential to serve as investments that benefit future taxpayers: increasing tax revenue from a more productive workforce and reducing health-based expenditures.

- The social safety net for children has changed substantially in the past 20 years — reducing the share of assistance going to the poorest children. Fundamental changes have occurred in the social safety net for children. Health insurance for low-income children expanded dramatically through Medicaid. But, more programs and spending have become contingent on work: Welfare reform dramatically reduced the availability of cash assistance in the 1990s, while the Earned Income Tax Credit expanded substantially, creating subsidies to work. As a result of changes to the safety net, an increasing share of assistance is going to children near and above the poverty threshold, while a decreasing share is directed to the poorest children living below the poverty threshold — despite a relatively stable share of children living in poverty (see here).

- Despite the dramatic changes in income inequality over the prior decades, there have been few changes that improve the progressivity of our tax system in response. On the contrary, many of the tax changes of recent decades have made the tax system less progressive. Declines in top labor rates, top capital gains rates, top dividend rates, and cuts to the estate tax have reduced progressivity at the top, although there have been a few changes that worked in the other direction, including the investment income surtax that helped fund the Affordable Care Act. At the bottom of the distribution, expansions of the earned income tax credit have generally reduced the federal income tax burden of the lowest earners. Still, while the overall effect of the tax system is to reduce inequality, the tax system reduces inequality a bit less than it did in the past: The federal tax system did less to reduce a standard measure of income inequality (the Gini coefficient) in 2013 than it did in 1980, according to the Congressional Budget Office.

- More recently, the Tax Cuts and Jobs Act is a clear move toward a less progressive tax system. On net, the nonpartisan Tax Policy Center estimates that, in 2018, the bottom 80 percent of U.S. taxpayers will receive a tax cut of $795, about 1.3 percent of their after tax income, but by 2027 the legislation will result in an average tax increase of $15 for the same taxpayers. In contrast, taxpayers in the top 1 percent of the income distribution are estimated to receive a tax cut in excess of $50,000 (more than 3 percent of their after-tax income) in 2018. By 2027, the top 1 percent still receives a tax cut in excess of $20,000. Joint Committee on Taxation estimates also find tax cuts tilted toward the top (see here).

- The centerpiece of the Tax Cuts and Jobs Act (TCJA) is large business tax cuts; in fact, most individual side tax cuts are phased out over the ten years following enactment. While Administration officials have made rosy predictions about large benefits to workers from business tax cuts, most economic evidence indicates that the vast majority of the benefits from these tax cuts accrue to those at the top of the distribution. And so far, wage growth has been flat.

- So far, the main effects of the TCJA have been large increases in deficits. Deficits have increased relative to GDP due to a sharp decline in the size of tax revenues relative to the size of the economy. Deficits make it more difficult to fund the safety net. In addition, our high levels of debt will make it difficult for policy-makers to respond to the next recession by buttressing the safety net or cutting taxes. The absence of budget flexibility could make the next recession far more painful for American workers.

- Finally, even though the TCJA is tax legislation, it also weakens the safety net directly. The repeal of the individual mandate of the Affordable Care Act is expected to increase the number of uninsured Americans. The increased number of uninsured also increases health insurance premiums for others, putting further stress on middle class paychecks.

What this Means:

The recent era of increasing income inequality and wage stagnation for those in the bottom two thirds of the income distribution mean that both a robust safety net and a progressive tax system are more important than ever. Given these dramatic changes in our economy, policy needs to respond accordingly, strengthening the social safety net and increasing the progressivity of the tax system. Unfortunately, recent policy changes have moved in the opposite direction.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.