The Productivity Slowdown is Even More Puzzling than You Think …

Wellesley College

The Issue:

Labor productivity — the amount of output produced from an hour of work — is a key economic metric that characterizes how efficiently an economy is operating. In addition, over long spans of time, increases in productivity have provided the means for pushing living standards today well above those of 50 or 100 years ago. Unfortunately, after a productivity boom fueled by the Internet and other information technology, the rate of productivity growth in the U.S. economy slowed down around 2004 and dropped even further around 2010. Economists often refer to this development as a “Productivity Paradox” because it has occurred in the midst of seemingly rapid advances in digital and other technologies that, in principle, should be boosting productivity.

Recent U.S. labor productivity growth has been exceptionally slow. If sustained, it would severely limit future increases in living standards.

The Facts:

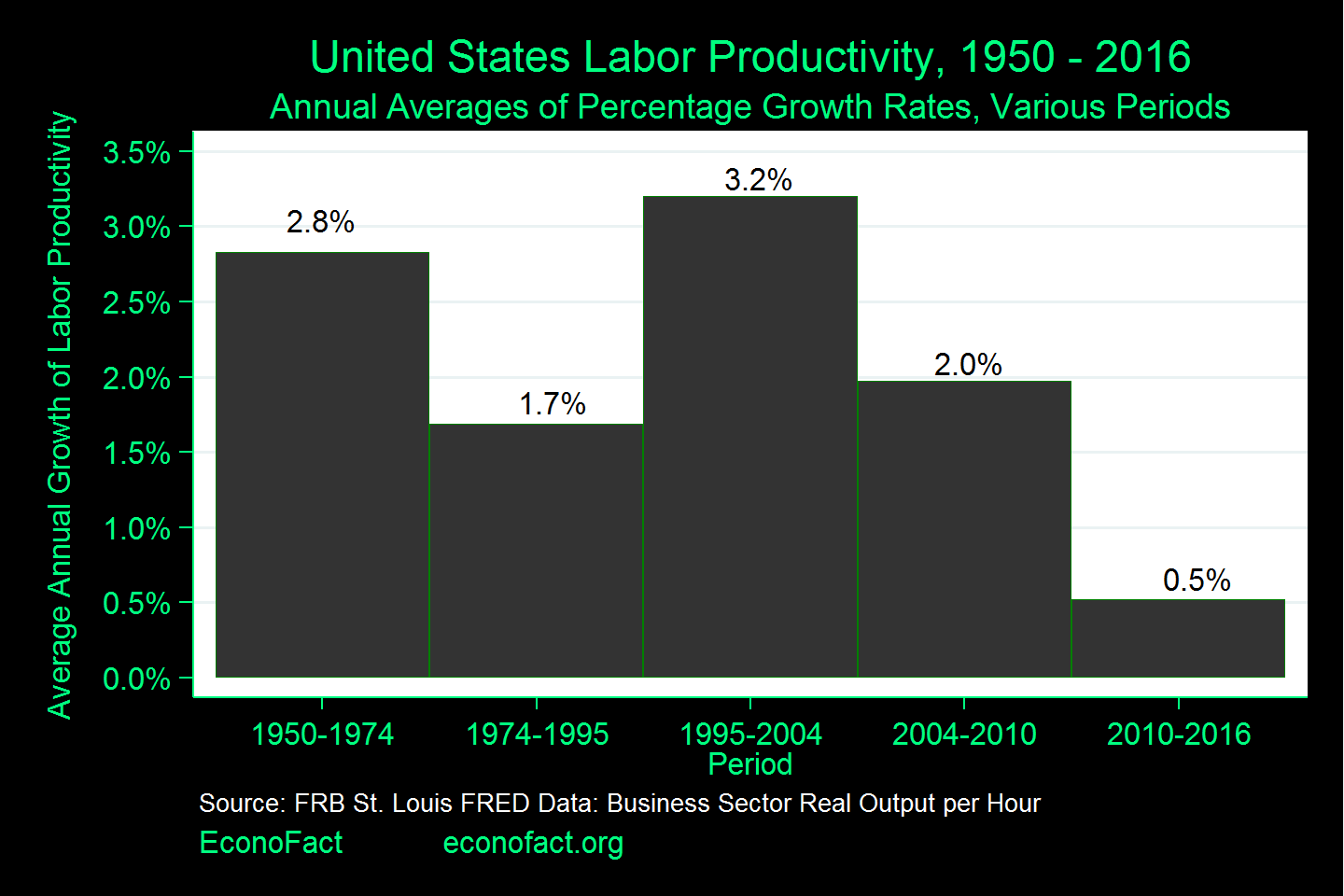

- U.S. Productivity growth has seen a dramatic slowdown in recent years. During the years of the Internet boom (1995-2004), labor productivity in the business sector rose at an average annual pace of roughly 3-1/4 percent according to data from the Bureau of Labor Statistics. Then, the growth rate of productivity slowed to about 2 percent a year during 2004-2010 before dropping to near ½ percent a year during 2010-2016 (see chart). By historical standards, an annual pace of ½ percent is exceptionally slow, and, if sustained, would severely limit future increases in living standards.

- Economists do not have a complete answer to the question of why productivity growth has been so slow. It is an issue that goes beyond the United States, with declining productivity growth being observed in other advanced economies, including Japan, Germany, the United Kingdom and Canada, among others. Possible explanations for the slowdown include economic historian Robert Gordon's thesis that the type of innovations that have the potential to transform economic life on a grand scale — such as electricity, public sanitation, and the internal combustion engine — are a thing of the past. Others argue that factors such as lower capital investment by firms, decreased competition, excessive regulation, and a slowing of gains in human capital (the education and skill level of the workforce) place limits on the pace of productivity growth. And, some argue that productivity is being mis-measured and is better than numbers would indicate. (See this working paper for different explanations of slowing productivity growth.)

- What makes this slow rate of growth in productivity even more puzzling, is that digital and other technologies appear to be advancing at remarkable rates. Examples abound with artificial intelligence, data analytics, autonomously controlled devices spreading through many industries; 3-D printing, tele-medicine and new diagnostic tools drawing on huge databases of medical outcomes; ubiquitous mobile access to vast digital resources in the cloud; and a host of other innovations in the digital sphere and elsewhere (for example in energy development and storage).

- How fast is innovation in these technologies? One way in which economists gauge the pace of technical advance in an industry over time is by comparing the rate of change in prices of that industry’s products with prices of all other goods and services. To see the logic of this approach, consider an industry experiencing rapid technological progress. With those gains, that industry will be able, over time, to produce more output from a given set of inputs or will be able to produce higher-quality products. If the cost of inputs is relatively stable, then those products should see their prices fall over time. For example, consumer and business electronics and telecommunications have seen rapid price declines in recent decades. In 1952, a 10-minute phone daytime call from New York to Los Angeles cost about $48 in 2016 dollars, as computed from Federal Communications Commission data. Today, phone companies do not even bother to separately price that call, and the call can be made from almost anywhere on a mobile phone rather than from a landline phone.

- New research is finding evidence that the pace of innovation in the digital economy is faster than has been measured. To get reliable comparisons over time, price measures should gauge prices per unit of performance. For a long-distance telephone call, that is a reasonably straightforward exercise. But, for many high-tech products, the task is much more difficult. For example, an iPhone 7 costs about the same as a new iPhone 4 did, but the newer model delivers much higher performance. Accordingly, economists would say that the price of an iPhone — after accounting for improvements in performance — has fallen over time. And while federal statistical agencies work hard at getting these prices right, recent research has provided evidence that prices of high-tech products — including computers, communications equipment, software, and semiconductors — are falling more rapidly than is captured in official statistics. For example, official measures indicate that prices of computing equipment fell at an average annual rate of 11.2 percent between 2004 and 2015; the latest research indicates that these prices actually fell at an 18.9 percent pace during this period. In our recent paper, David Byrne, Stephen, Oliner and I show that these faster price declines then, in turn, imply that the pace of innovation in high-tech products is more rapid than it appears in official statistics. This work also shows that the rate of technical advance in the rest of the economy (outside of high-tech sectors is slower than indicated by the official measures.

What this Means:

If the pace of innovation in high-tech products is faster than implied by official statistics, then the productivity slowdown is even more puzzling than implied by official statistics. But, the very fact that the pace of innovation in the technologies underlying the digital economy is faster than we thought also gives hope for the future. In past historical epochs of innovation — think electrification or the spread of the Internet — it took a long time for new technologies to diffuse through the economy to a sufficient extent that they boosted economy-wide productivity growth. In these past episodes, businesses had to learn how to exploit the new capabilities and to make the necessary structural changes to implement them. The same type of delay could be happening now, and the faster pace of innovation that recent research points to could be the fuel needed ultimately to lead to a productivity revival.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.