Will Social Security be There for You?

Harvard University

The Issue:

The good news in the 2018 report of the Trustees of the Social Security Trust Fund, released in early June, was that the program is expected to have enough money to pay for scheduled retirement benefits for the next decade and a half. There are concerns, however, about the longer-run financing of the program. Because of population aging, the program is projected to exhaust its ability to fund full retirement benefits in 2034; after that time, the Trust Fund will be depleted and incoming revenues will only be sufficient to pay 77 percent of scheduled retirement benefits.

Population aging is straining the program. The earlier this is addressed, the more time Americans will have to adjust and compensate for changes.

The Facts:

- The Social Security program provides vital income support to tens of millions of older Americans. Social Security provides retirement benefits to more than 40 million people each year, as well as to millions more spouses, dependents, and survivors of deceased workers (see this EconoFact piece). The benefits provided by Social Security represent 90 percent or more of income for close to one-quarter of elderly married couples and more than 40 percent of elderly unmarried people, according to the Social Security Administration. The Census Bureau estimates that Social Security benefits lifted 17 million people age 65 and older out of poverty in 2016 (close to 35 percent of that population).

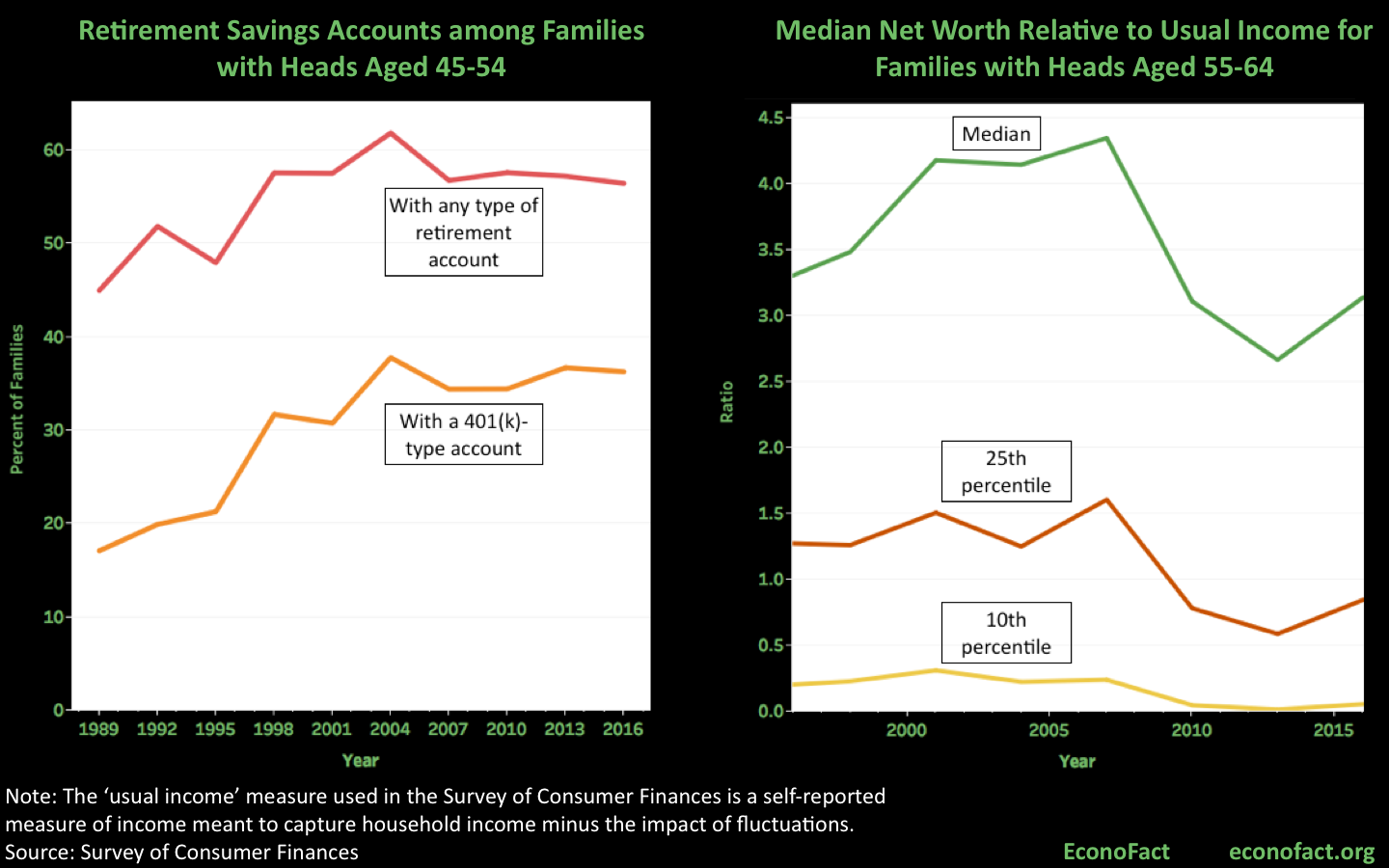

- Many of the Americans who are now approaching retirement age will be even more dependent on their Social Security benefits for financial security than today’s retirees. To start, Americans currently nearing retirement age are less likely to have income from private defined-benefit pension plans to supplement their Social Security income than earlier cohorts. Calculations based on Survey of Consumer Finances (SCF) indicate that 37 percent of families with heads between ages 55 and 64 are covered by such plans, down from 53 percent in 1989. Moreover, Americans nearing retirement age have done less of their own saving to finance their retirement compared with those of a similar age in the past. According to the SCF, the median ratio of net worth to “usual income” for families with heads between age 55 and age 64 was 28 percent lower in 2016 than it was just prior to the crisis — and even a little below where it was in 1995 (see chart). Families lower in the distribution have even less net worth than their counterparts in earlier cohorts. (The Survey of Consumer Finances asks respondents to state their "usual" income to capture a version of household income that is devoid from negative or positive income "shocks" that are unlikely to persist, say from a temporary unemployment spell or an unexpected salary bonus.)

- Only about one-third of American families nearing retirement are using workplace retirement plans such as 401(k)-type accounts. While research suggests that one way to encourage working-age people to do their own saving for retirement is to provide them with access to workplace retirement savings plans, many Americans are not using such plans. Calculations based on the SCF suggest that the share of families nearing retirement with a 401(k)-type account was 36 percent in 2016, having shown no net increase since 2004 (see chart). Some families may have rolled over their 401(k)s from earlier jobs into individual retirement accounts (IRAs); the share of families with any type of retirement account was considerably higher in 2016, at 56 percent, but has shown no net increase in more than 20 years.

- The longer-term financial problems of the Social Security program arise from the aging of the population. The program has “pay-as-you-go” financing, meaning that the Social Security benefits paid at any given time are funded by the Social Security taxes that are being collected from workers at that time. Until this decade, the ratio of the working population to the retired population was large enough such that tax revenues exceeded the benefits paid, with the surplus used to buy assets for the Social Security Trust Fund. But, that ratio has been falling as the baby boomers have moved into retirement — with retirement benefits paid beginning to exceed the relevant tax revenues in 2010. The shortfall between the income and expenses of the Social Security retirement program has been funded — and can continue to be funded for a number of years — through the return on the assets in the trust fund and (eventually) by redeeming those assets.

- Going forward, the aging of the population will strain the finances of the Social Security retirement program yet further. According to the Congressional Budget Office, the number of Americans who are 65 or older will increase by 34 percent over the next 10 years, while the number between ages 20 and 64 will increase by just 2 percent. As a result, the trust fund reserves available to finance Social Security retirement benefits are projected to be depleted by 2034. At that point, revenues taken in by the program will be only sufficient to pay 77 percent of scheduled retirement benefits. The law governing the Social Security program will thus need to be changed to make the program financially sound for future cohorts of retirees. The finances can be fixed by cutting benefits (including by raising the retirement age), raising taxes, or some combination of the two options. Policymakers may weigh a number of considerations when deciding exactly how to fix the system, including the different experiences in recent decades for higher- and lower-income people regarding wage growth and changes in life expectancy.

- Historically, major changes to the Social Security retirement program have been implemented gradually so as to give people time to adjust in various ways such as by raising their retirement saving or making plans to work longer. For example, to address an expected shortage of funds in the early 1980s, the Social Security law was changed to raise the age at which full retirement benefits can be claimed by two years, with the implementation of this change occurring over more than 40 years. To follow this strategy now, policymakers will need to act sooner rather than later given projections that the program will face a shortage of funds in roughly 15 years.

What this Means:

Although the Social Security program has ample funding to pay retirement benefits for a number of years to come, we have long known that the program will eventually run short of the money it needs to fully finance scheduled retirement benefits. With families that are nearing retirement age today tending to have less of their own savings and being less likely to have private defined-benefit pensions, it is more important than ever to address the longer-term financial challenges faced by the Social Security program. Changing the law now to phase in changes that shore up the finances of the program would have the advantage of allowing Americans to make gradual adjustments to their work and saving behavior to compensate for these changes.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.