How Immune Is the Federal Reserve From Political Pressure?

University of Maryland

The Issue:

The state of the economy affects the popularity of incumbent governments. For this reason, there is an incentive for politicians to attempt to influence monetary policy decisions, spurring growth with lower interest rates. This incentive can be especially strong in the run-up to elections. For this exact same reason, the Federal Reserve is structured to make interest rate decisions independently of electoral politics. While lower interest rates stimulate economic activity in the short run, they also risk fueling inflation and economic instability over a longer horizon. However, the independent structure of the Fed has not always insulated it from political pressure. An analysis of the personal interactions between US presidents and Federal Reserve officials between 1933 and 2016 shows that there were times when pressure from the president influenced the Fed’s activities at the expense of price stability.

Political pressure on the Fed during the 1970s and in the 1960s increased inflation over and above what macroeconomic factors would predict

The Facts:

- There is ample evidence of the importance of central bank independence. Countries with more independent central banks tend to enjoy lower inflation on average. This better inflation performance does not come at the expense of higher average unemployment (see here). In contrast, countries in which politicians have more power over central banks, for example by having more ability to fire the heads of the central bank or to have a more direct say in monetary policy, have a history of higher inflation and more economic instability. Beyond potential efforts to stimulate the economy before elections, this instability can also arise because subservient central banks can be made to help finance government budget deficits, by buying bonds or by allowing for more inflation, which reduces government liabilities in real terms. This monetization of the deficit helps initially to keep interest rates low but comes at the cost of eventual higher inflation.

- Many aspects of the Federal Reserve’s structure are designed to help insulate it from political pressure. It is an independent government agency, in the sense that it does not receive its funding through the congressional budget appropriations process. It is not part of the executive, legislative, nor judicial branches of the government. Its leadership does not change when a new US president and a new US Congress are elected. Members of the Board of Governors of the Federal Reserve System are appointed for 14-year terms, in order to disconnect them from the electoral cycle. The chair and vice chair are appointed for 4-year terms, which can be renewed multiple times. As an example, Fed chairs William McChesney Martin and Alan Greenspan were both in office as long as 19 years.

- Despite the institutional structure that attempts to insulate the Federal Reserve from political pressure, there are still ways in which presidents can try to influence monetary policy. This can be done directly or indirectly. For instance, a president could request a meeting with the Chairman of the Federal Reserve or other Fed officials in order to explicitly express desired policy goals. The president might also instruct cabinet members, or members of Congress, to talk to Fed officials and persuade them to change policy. The president might exert public pressure on the Fed, by criticizing the Fed’s action in speeches, in interviews with journalists, or more recently through social media. There is some evidence that this type of pressure can have an effect. One recent study looked at President Trump’s tweets regarding the Fed from the launch of his presidential campaign in 2015 to 2021. The study found that the tweets had a measurable impact on financial market expectations of future monetary policy — indicating that the markets believe that the president can influence the conduct of monetary policy in a sizable and persistent way.

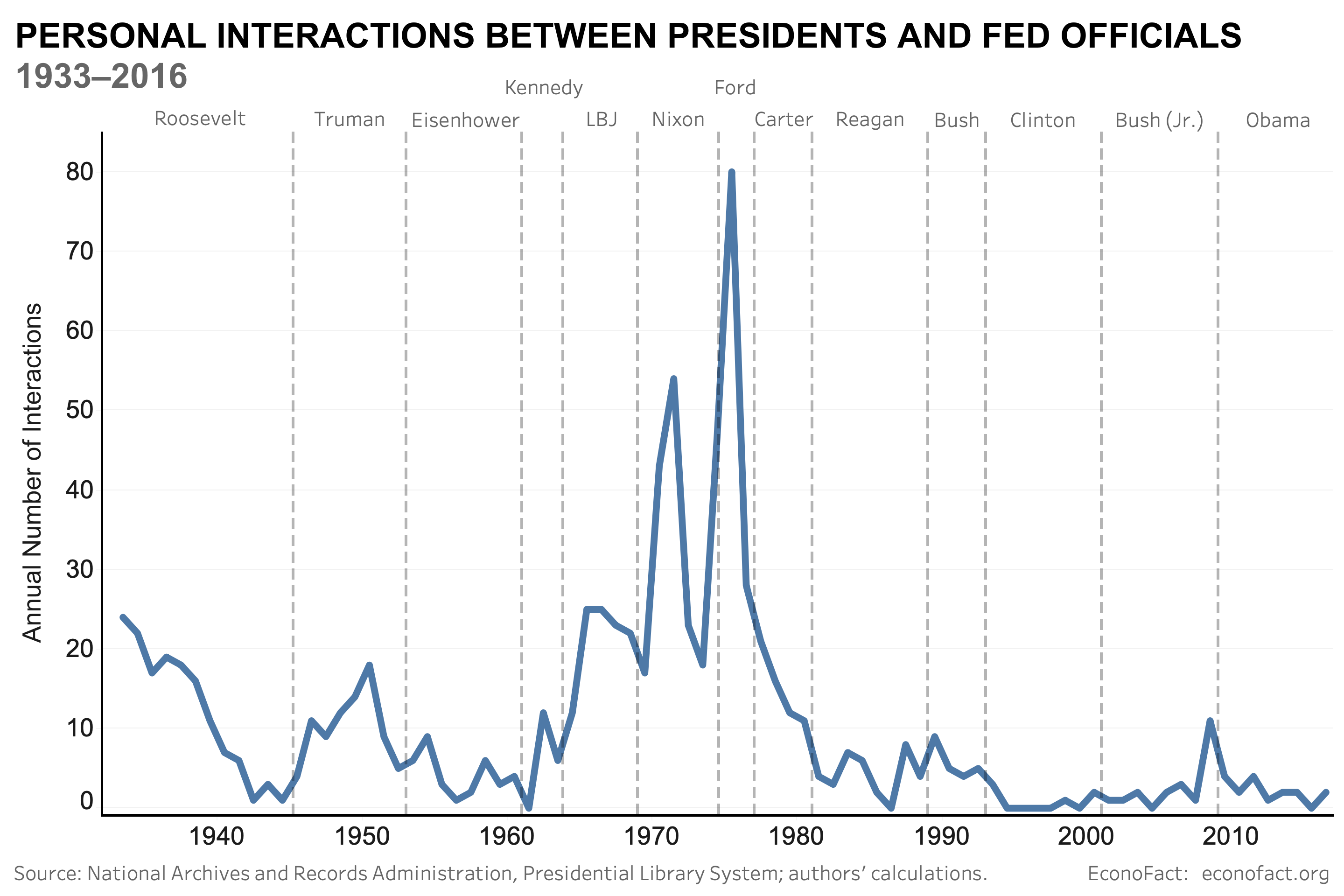

- The presidency of Richard Nixon offers a clear example of a moment in US history when a president tried to influence the Fed. Researchers have documented evidence from the Nixon tapes that President Richard Nixon pressured then chairman of the Federal Reserve, Arthur Burns, to engage in expansionary monetary policies in the run-up to the 1972 election. Writings in Burns’ diary describe how Burns felt a growing pressure to serve the needs of Nixon’s reelection over the economic welfare of the country. An analysis of the Fed’s Federal Open Market Committee (FOMC) transcripts from the period concluded that political considerations impacted the Fed’s decision-making and were an important contributor to the rise in US inflation in the 1970s.

- But political pressure is generally difficult to define and quantify. One way to approach this systematically is to look at the number of meetings between the president and Fed officials. There is wide variation across presidencies in the number of meetings between the president and Fed officials. For example, Bill Clinton met only 6 times with Fed officials during his 8-year presidency, while Richard Nixon had 160 meetings during his 6 years in office. Presidents Johnson, Carter and Reagan personally interacted 109, 60, and 34 times with Fed officials (see chart for the number of meetings in each year). Of course, meetings can occur for many reasons — including in response to economic conditions — and do not necessarily reflect political pressure. For instance, in a recession a president might be more likely to summon a Fed chair to ask for their view on the economy. To address this, I use information from the known episode of political pressure on the Fed during the run-up to the 1972 election to characterize meetings that constitute efforts to influence monetary policy. This enables me to measure the inflationary effect of political pressure through personal interactions over and above what would have been expected given other macroeconomic conditions. I find that an increase in political pressure by half as much as the pressure exerted by President Nixon, for six months, raises the US price level more than 8%. Political pressure shocks mainly occurred during the 1970s, as well as in the 1960s during the Johnson administration. My study finds that political pressure shocks strongly and persistently increase inflation.

What this Means:

The independence of the Fed has once again come into heightened focus. Starting his second term, President Trump has shown willingness to publicly criticize the handling of monetary policy, which he also exercised during his first term. In his Davos speech in January 2025, President Trump pledged to “demand that interest rates drop immediately–and likewise, they should be dropping all over the world”. In addition, the Trump administration has asserted its intent to exercise greater “Presidential supervision and control of the entire executive branch… including so-called independent agencies” in two executive orders issued on February 18 and February 19, 2025. The new presidential authority in the order, which will likely be subject to litigation, includes the Fed’s role in the regulation of the banking system but excludes the setting of monetary policy from this new presidential oversight. Of course, the president is not the only politician to seek to influence the Fed. On the other side of the political divide, Senator Elizabeth Warren urged Fed Chairman Jerome Powell to “move more rapidly to bring down interest rates” during testimony before the Senate Banking committee in February 2025. So far, Chair Powell has appeared committed to steer clear of interference, by repeatedly emphasizing the Fed’s political independence. Should the Fed change course and give in to political pressure from either side of the political spectrum, then history does not bode well for US inflation.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.