Leaning on the Fed (Updated)

The Fletcher School, Tufts University

The Issue:

The Federal Reserve walks a tight balance between maintaining low unemployment and preventing the economy from heating up and unleashing inflation. Its decisions carry consequences for different groups that might be tempted to exert pressure to favor the outcome that most benefits them. The independence of the Federal Reserve helps to ensure that it can make politically difficult decisions that are in the long-run best interest of the economy, just as the independence of the judiciary branch helps ensure adherence to the rule of law, even when those decisions are politically unpopular. Research shows the importance of central bank independence for good economic performance. Nonetheless, the independence of the Federal Reserve is not immune to threats from the Executive branch or Congress.

Central banks that are insulated from political pressure can make tough decisions about fighting inflation and, when the public recognizes this, average inflation tends to be lower.

The Facts:

- The Federal Reserve’s dual mandate requires it to “promote effectively the goals of maximum employment, stable prices, and moderate long term interest rates.” In practice, this has resulted in the Federal Reserve setting monetary policy to stabilize the economy, having it run neither too hot nor too cold. In order to do this, the Fed raises the federal funds rate when there are sufficient concerns about rising inflation and lowers it when there are sufficient concerns about rising unemployment and a slowing economy. This “Goldilocks” goal typically involves the Federal Open Market Committee (FOMC), the policy-setting body of the Federal Reserve, which holds eight annual regular meetings to assess economic conditions.

- By its very design, the Federal Reserve is structured to be insulated from political pressure. The Fed is not part of the executive, legislative, nor judicial branches of government. Its funding does not depend on congressional appropriations, its operations are financed primarily from the interest earned on securities it owns (see here). The chairman of the Federal Reserve and its two vice chairs are appointed midway through a presidential term. The terms of the other members of the Board of Governors are staggered and fourteen years-long. This is meant to prevent a president from taking advantage of the power to appoint governors by “stacking the deck” with members that favor the president’s policies and to provide continuity and stability to monetary policy.

- There can be short-term political advantages from implementing particular interest rate policies, but they come at the expense of longer-term costs to the economy. Raising interest rates can be painful for borrowers and businesses seeking to invest and lead to an economic slowdown. Central banks that are subject to political pressure from incumbents would tend to run monetary policies that are too expansionary, especially in advance of elections. Inflationary pressures would then need to be quelled by subsequently tighter monetary policies. This happened in the United States in 1972 when Richard Nixon pressured Federal Reserve Chair Arthur Burns to stimulate the economy in order to promote his re-election. Interest rate policy was, in fact, stimulative in that pre-election period, only to strongly reverse course afterwards in an effort to stamp out inflationary pressures exacerbated by the stimulus. This stop-and-go approach to monetary policy is economically destabilizing. It is also important that central banks are independent of a country’s treasury or fiscal authorities (which are typically part of the Executive Branch). Otherwise, there would be pressure for the bank to help finance government deficits by purchasing government debt. This would increase the money supply and lead to inflation. Extreme examples of this result in hyperinflation, as in Weimar Germany in the 1920s, and Venezuela and Zimbabwe in this century.

- One reason for the importance of central bank independence is that it allows the institution to earn a reputation for policy credibility that shapes people’s expectations of how it is going to respond to economic circumstances. Inflation partially reflects people’s expectations of how prices will change in the future. If people expect inflation to be high they will set prices and wages that reflect these expectations which then becomes a self-fulfilling prophecy. This has implications for the link between the central bank’s independence and inflation; central banks that are insulated from political pressure can make tough decisions about fighting inflation and, when the public recognizes this, average inflation tends to be lower. Notably, this lower inflation does not require higher average unemployment. An illustration of this is how inflation expectations in the United States stabilized in this century as compared to the last quarter of the 20th century. This meant that the spike in inflation in the wake of COVID was not thought to represent a permanently higher rate of inflation, given the experience of the past decades, so the subsequent disinflation was not accompanied by a significant rise in unemployment, unlike the disinflation of the early 1980s.

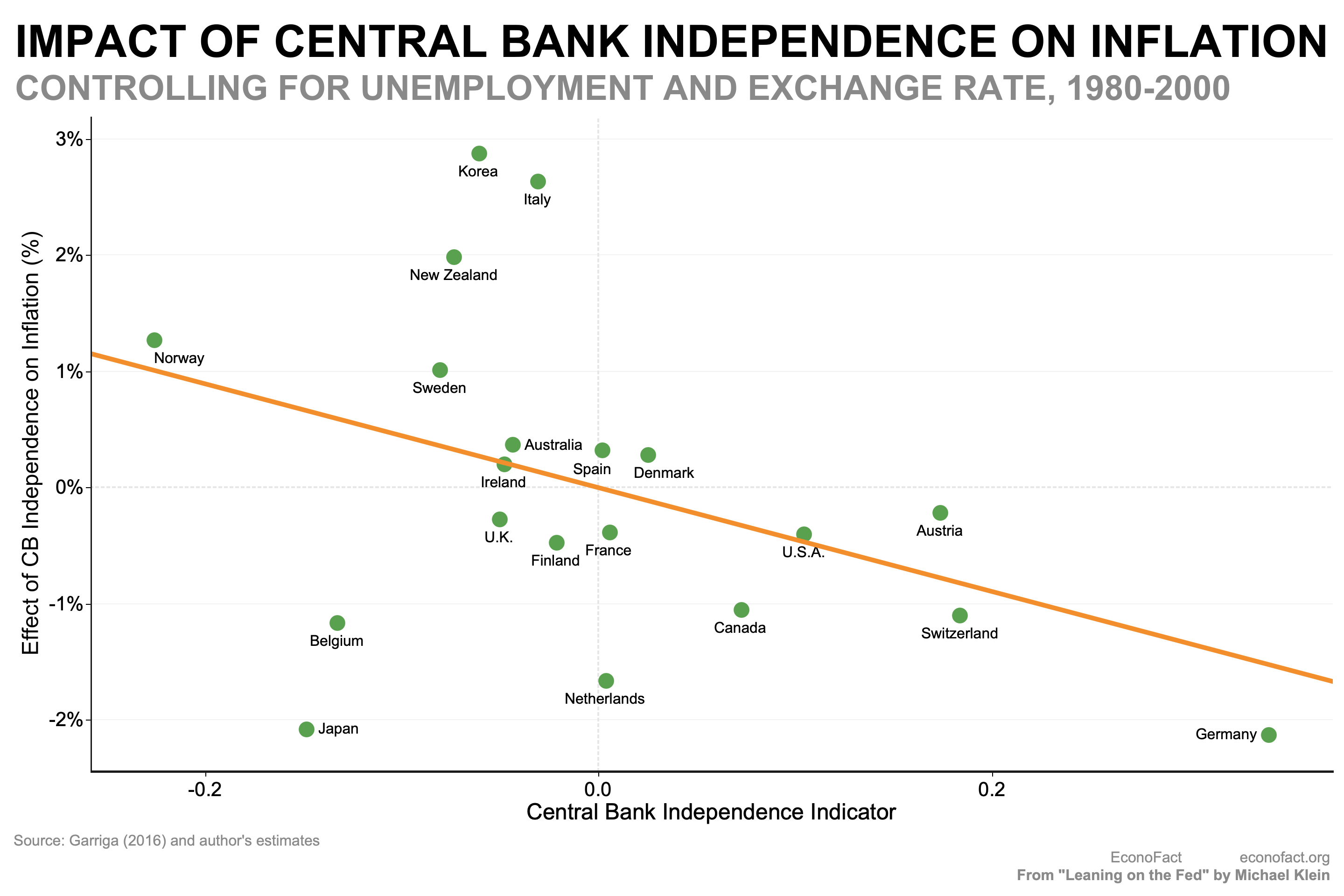

- Empirical analyses support this association between central bank independence and inflation. Countries with more independent central banks tended to have lower inflation than countries whose central banks were less independent over the 1980-2000 period. A scatterplot of average inflation rates for 20 advanced economies against an indicator of the independence of their central banks over the period shows that countries with a lower measure of bank independence, such as Norway, tended to have higher inflation than those with more independent central banks, such as Germany (see chart). (The relationship controls for unemployment and exchange-rate regime.) An analysis by the IMF using more recent data also shows how more independent central banks were more successful at tempering people’s expectations of inflation, and, through this channel, resulted in lower inflation. (The study included a wider set of advanced, emerging market, and low-income countries in the 2007 to 2021 period.) Notably, there has been a move towards making central banks more independent that reflects a greater appreciation of the importance of this institutional arrangement.

- The fact that the Federal Reserve has been designed to be independent does not fully protect it from political attacks. There have been times when politicians respond forcefully to the Fed’s policies. For example, President Trump complained about the Federal Reserves’ tight-money policies in his first term and more recently “lashed out” at the Fed when it kept interest rates unchanged in its January 2025 meeting. Representative Barney Frank (D-Massachusetts) voiced strong disagreement with the Fed’s decision to raise interest rates on the floor of the House in 1997. The House Committee on Oversight and Government Reform passed an “Audit the Fed” measure in 2017 that would have made monetary policy decisions subject to Congressional review and, potentially, congressional pressure. But there are also examples of Presidents honoring the independence of the Fed; for example, President Reagan reappointed Paul Volker, President Clinton reappointed Alan Greenspan, and President Obama reappointed Ben Bernanke, all of whom were initially appointed by the preceding Presidents.

What this Means:

William McChesney Martin, Jr., the Chairman of the Federal Reserve from 1951 – 1970, famously quipped that a common role of the Federal Reserve is to take away “the punch bowl …just when the party was really warming up.” Removing the punch bowl may not be a popular choice. But both theory and evidence show the advantages of having a central bank that has a reputation for not bowing to political pressure. Good reputations are hard to establish and easy to destroy. Politicians whose threats against central banks’ policies are successful may find some short-term benefit but at an ultimate cost to the economy.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.