Taming Inflation: No Pain No Gain?

Williams College

The Issue:

Consumer prices rose 3.7% from August 2022 to August 2023. While inflation still exceeds pre-pandemic levels and the Federal Reserve’s two percent target, it has fallen dramatically from its June 2022 peak of 8.9 percent on a year-over-year basis, the steepest drop on record that has not been associated with a recession. The rapid deceleration contradicts the predictions of those who believed that a rise in unemployment would be necessary to reduce inflation. What accounts for inflation’s abrupt deceleration? Why has taming inflation not required a recession up until this point?

Inflation expectations have been less sensitive to rising prices than they were in the 70s and 80s, facilitating the fight against inflation.

The Facts:

- One source of inflation is an imbalance between the amount firms, households and governments wish to spend and what the economy can produce. In the aftermath of the Covid-19 pandemic, the federal government’s relief programs contributed to a sharp increase in personal disposable income, which increased households’ demand for goods and services. The Federal Reserve’s zero interest rates and quantitative easing policies also buoyed spending by increasing asset prices and reducing borrowing costs. At the same time, supply chain disruptions reduced the supply of goods available for households to purchase, and a three percentage point drop in labor force participation, reduced the economy’s ability to produce the goods and services households and firms wished to purchase.

- The dissipation of temporary inflation pressures has contributed to the drop in inflation. Following a stimulus-fueled post-pandemic period of rapid growth, consumer spending growth has returned to its pre-pandemic trend, and private-sector investment spending has plateaued. The Fed’s 5.25 percentage point increase in the target federal funds rate over the past 18 months has likely contributed to the slowdown in these interest-sensitive categories of spending. Labor force participation has rebounded and is approaching its pre-pandemic level. Commodity prices have fallen by eight percent since June 2022, reducing the cost of production of some goods and services. And in a sign of easing supply disruptions, the cost of containerized cargo shipping has fallen 85 percent since its post-pandemic peak in September 2021.

- Inflation expectations also matter. Temporary price increases may lead to persistent inflation if those increases get built into expectations. When prices are adjusted only infrequently, firms will set their prices based on likely future costs and expectations of what the market will bear in the coming months. Similarly, because wages are negotiated infrequently, workers will bargain for wages that factor in anticipated increases in the cost of living. Therefore, price rises can become self-fulfilling, and what might otherwise have been a transitory spike in inflation will persist for a longer period of time.

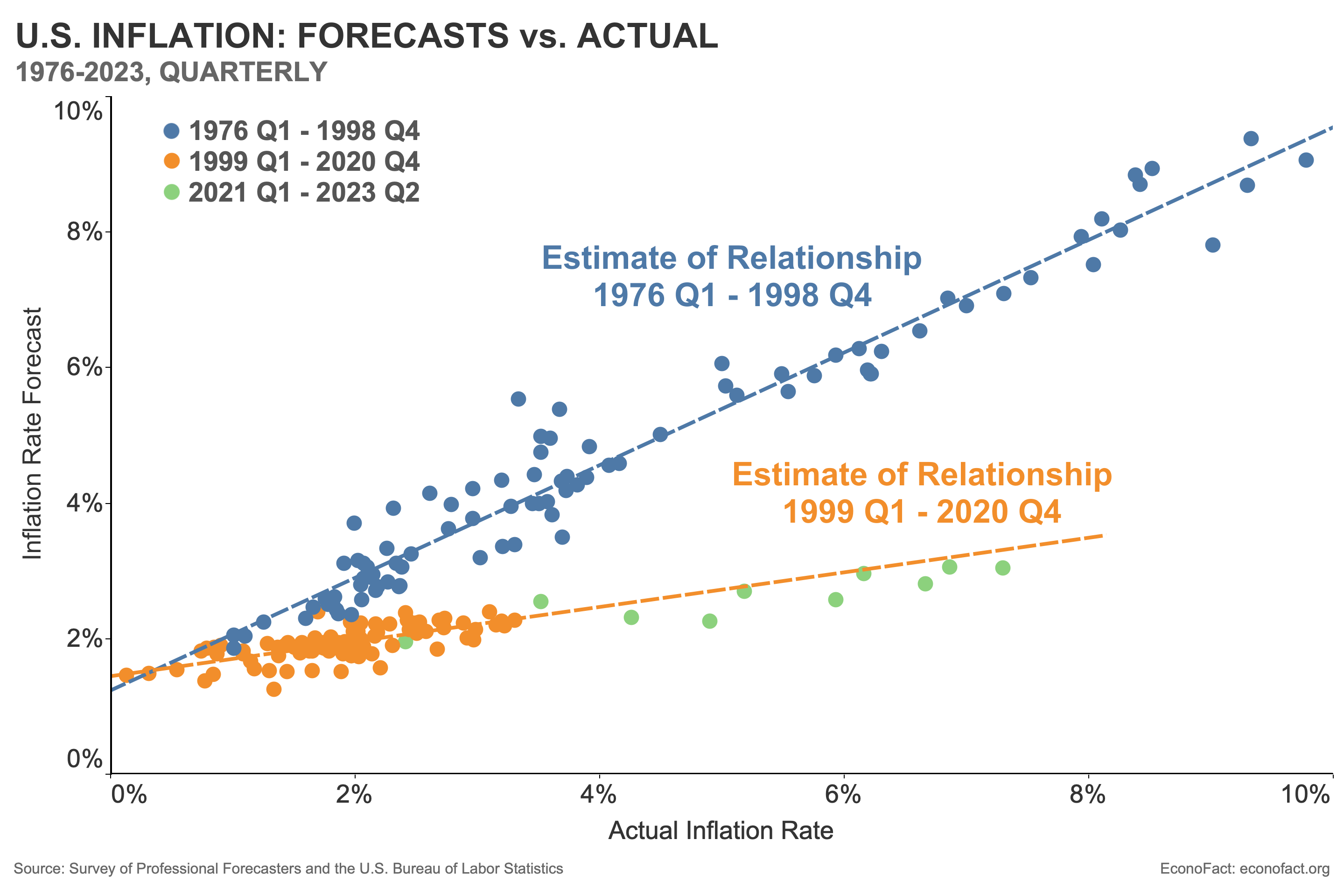

- Until the late 1990s, inflation expectations reacted strongly to inflation. Consequently, rising inflation in the 1970s led to immediate, nearly one-for-one upward revisions to medium-term inflation forecasts (see chart). The chart shows the four-quarter inflation rate, calculated using the chain-weighted GDP price index, on the horizontal axis; and the median one-year-ahead forecast from the Survey of Professional Forecasters, an indicator of medium-term inflation expectations, on the vertical axis. From the first quarter of 1976 through the fourth quarter of 1998, the slope of the best-fit line implies that a one percentage point increase in inflation over the previous four quarters led forecasters to revise upward their year-ahead forecasts by 0.8 percentage points, on average. The pattern also reflects declines in inflation expectations in the 1980s and 1990s caused by the drops in inflation that followed the 1981-82 and 1990-91 recessions.

- Inflation expectations became more stable after 1999. The best-fit line through the points from the first quarter of 1999 through the fourth quarter of 2020 is much shallower than in the pre-1999 period. In fact, the slope indicates that a one percentage point increase in the inflation rate between 1999 and 2020 led forecasters to revise upward their forecasts by only 0.2 percentage points, on average. This is evidence that expectations have become better “anchored,” in the sense that they have become less sensitive to inflation.

- Expectations have remained stable in the past three years, despite the post-pandemic inflation surge. Remarkably, the points in the plot that correspond to the period from the first quarter of 2021 through the second quarter of 2023 lie on (if not slightly below) the shallow line fit to the 1999-2020 data. This suggests that expectations have remained well-anchored since the pandemic, in spite of the most rapid inflation acceleration since the 1970s.

- The Federal Reserve’s commitment to price stability may explain why inflation expectations have remained anchored. The Federal Reserve’s mandate, as stated in the Federal Reserve Act, is to pursue “maximum employment and stable prices.” Until relatively recently, however, these objectives were not spelled out explicitly; nor was there clarity with regard to which would take precedence. But beginning in the late 1980s then-Fed chair Alan Greenspan made it increasingly clear that the Fed would prioritize price stability; and in 2012 the Federal Open Market Committee (FOMC) announced an explicit target inflation rate. These changes are credited with anchoring inflation expectations and reducing inflation persistence.

What this Means:

A combination of good luck and good policy explains the rapid ebbing of inflationary pressures. The good luck was that the Covid-19 pandemic did not permanently scar the supply side of the economy: input costs have fallen, labor force participation has bounced back and supply chains have been repaired. The good policy was the Fed’s emphatic reiteration of its commitment to price stability. Its commitment appears to have been sufficiently credible to keep inflation expectations anchored, despite an unusually long one-year delay between the first signs of accelerating inflation in the spring of 2021 and the commencement of policy tightening in March 2022. Consequently, the “no pain, no gain” theory of disinflation may be less relevant than in the past; if so, a recession may prove not to be necessary to bring inflation back down to the Fed’s two percent target.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.