The Perfect Storm in Home Insurance

Appalachian State University

The Issue:

The Los Angeles fires, perhaps the costliest weather-related event in U.S. history, started just a few months after Hurricane Helene which ranked among the top 10 costliest hurricanes to batter the United States. And while hurricanes and wildfires command the most attention, severe convective storms — those traditional hailstorms that generate tornadoes and severe winds — have become more frequent and more severe and are depleting the financial resources of insurers and reinsurers for the so-called normal events. Add to that high inflation and supply chain problems making it more expensive to rebuild and replace property — among other notable factors — and the result is an insurance system that is being stressed in ways it had not been before, essentially breaking down in a number of states.

If insurance companies are able to charge higher premiums to cover rising costs, then the question is whether consumers can actually afford them.

The Facts:

- Getting home insurance has become increasingly difficult and expensive in many parts of the United States. The average home insurance premium in the United States rose by 33% from $1,902 in 2020 to $2,530 in 2023 — a 13% increase over and above what is accounted for by inflation — according to a new working paper by economists Benjamin Keys and Philip Mulder. But it is not just affordability that is an issue. Accessibility to insurance has also decreased as large insurers have pulled out of markets including in Florida, California, and Louisiana. In addition, over 1.9 million policies across the country were not renewed between 2018 and 2023, with non-renewal rates doubling since 2020, particularly in areas at highest risk of climate-related disasters. Consumers facing considerable insurance affordability and availability difficulties have fueled the growth of state insurers of last resort in Florida and California. These plans are partially subsidized by insurance companies and often provide less coverage than standard insurance. Florida’s residual market, Citizens Property Insurance Corporation, has become the largest property insurer in the state with around 1 million policies. The residential coverage under the California FAIR plan has more than doubled over the past four years, from about $150 billion in property value and over 203,000 policies in 2020, to over $430 billion in property value and over 451,000 policies as of September 2024. When state-backed plans face a deficit, insurance companies are required to pay assessments based on their market share in the state. This exposure creates further incentives for private insurers to reduce the number of policies they offer in these states.

- Insurance works by pooling risk, but there are circumstances under which the system breaks down. Homeowners insurance works by grouping together a large number of properties and transferring the individual property risks to the group. Policyholders pay the average expected loss rather than the individual actual loss. In order for the system to work, insurers need to have a relatively accurate estimate of future losses and be able to charge a premium based on those predictions. But there are conditions under which this does not work. If the properties in the pool are highly correlated such that everybody is impacted at the same time, for instance during an earthquake or large-scale wildfires or flooding, then the system can break down. Problems also arise if the confidence of the predictions is eroded. Insurance providers tend to rely on historical data for loss and cost estimates such that expectations are based on previous weather patterns, previous inflation rates and previous interest rates. All those factors have seen increased uncertainty in the last few years.

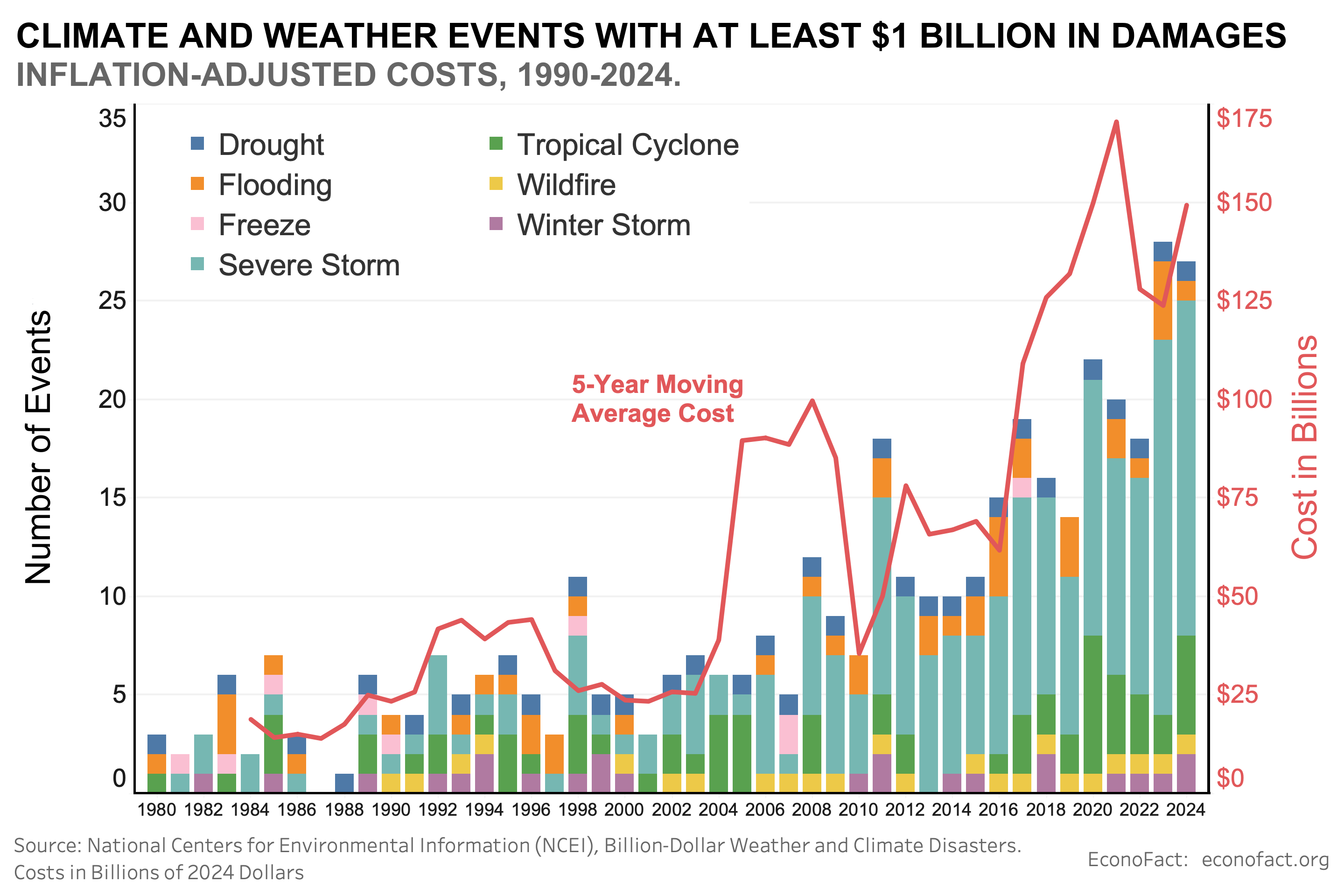

- More severe climate events, population migration, and the recent surge in inflation, mean that insurance companies in many regions of the country are paying more losses. Home insurers had to pay $15.2 billion for losses in 2023, the worst year for the industry since 2000. Climate change is clearly a large part of the story but not the only one. The number of climate-related disasters that cost over 1 billion dollars (adjusted for inflation) more than doubled in the United States during 2010-2020 relative to the previous decade and are on track to be higher this decade (see chart). The surge in economic damage from climate events is due in part to population migration to more at risk areas, which increases the value of property and assets at risk. Not only have more people moved to coastal locations exposed to hurricanes, but there has also been a disproportionate pace of development in areas at high risk of wildfires and other climate hazards. Since mid-2021 inflation also added to the toll, making it more expensive to rebuild and replace properties experiencing loss or damage. Between 2017 and 2023, the US property and casualty industry homeowners line experienced underwriting losses in 6 of the 7 years.

- Challenges to the reinsurance market have also impacted insurance providers, creating ripple effects for homeowners. Insurance companies — as well as governments, and agencies such as the Federal Emergency Management Administration (FEMA) — turn to the reinsurance market to reduce their exposure to large concentrated risks that result in substantial losses, such as hurricanes and wildfires. Simply put, reinsurance is insurance for insurance companies. It is a private market and their rates are not regulated, which means that they can swing wildly. Reinsurance rates for American property insurance providers unexpectedly increased dramatically in 2022 and 2023. While losses to climate-related events played a role in driving these higher rates, economic conditions played a very big factor as well. Higher interest rates in the fight against inflation caused the value of bonds to drop, eroding the value of the large bond portfolios that a lot of reinsurers hold. A strong US dollar also hurt the finances of reinsurance companies, since most of them are based in Europe, the United Kingdom, and Bermuda: if they are paying claims in dollars, a strong dollar makes it more expensive for them to pay their claims.

- Insurance companies are not always able to raise premiums high enough or fast enough to cover their growing costs. Premiums have to be approved in nearly every state by the state regulator. It is a slow process that is also impacted by political forces. Many insurance commissioners are either elected or appointed and their jobs are at risk if they let insurance rates go too high. Insurance companies were in a tough spot when reinsurance rates unexpectedly increased dramatically in 2022 and 2023. Even if state regulators allow a commensurate rate increase, it might take them two to three years to approve it. Facing higher reinsurance rates, paying more in losses, and unable to get the rate increases that they expect, insurance companies either pull out of riskier markets or transfer more of the risk to the consumer through higher deductibles or reduced coverage terms. If insurance companies are allowed to charge higher premiums, then the question is whether consumers can actually afford them. If homeowners are not required to have insurance (40% of homeowners own their house outright), they might choose to go without. One study found that the share of Americans that no longer had home insurance had risen from 5% in 2019 to 12% by 2024 (see here).

- A lack of affordable home insurance can have widespread consequences for the economy. In order to have a resilient community, one that can recover from a catastrophic event, you have to have some sort of program that's going to help pay for losses. Insurance tends to be the one used historically in the United States, combined with different governmental programs. A lack of insurance tends to make recovery from a catastrophe more difficult for individuals and communities. In a situation of widespread damage, lenders can be at risk as defaults rise. More broadly, friction in the home insurance sector impacts people’s ability to buy and sell homes. Lenders cannot provide loans unless their collateral is insured. Ultimately, lack of well-functioning insurance markets would limit economic growth.

What this Means:

In the short term, the outlook for insurance is difficult. Although inflation has decreased from its post-pandemic highs, prospects point to likely increasing homebuilding costs. The construction sector already faces labor challenges and these are likely to get worse with deportation of undocumented immigrants. If tariffs raise prices in the housing sector, this will also contribute to higher insurance costs and rising premiums. Over a longer horizon, through mitigation and wiser development — changing the way we build houses and where we build them — there is a path for improvement. If we can find ways to build homes that are more resistant to damages and able to recover and not be unusable after an event, then eventually we will have a stronger housing stock. But it will require more active government involvement in mandating certain building codes and better informed consumers demanding certain types of construction when they buy a house.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.