Fewer US Homes Are Insured Against Floods, Even as Risks Are Rising

Queens College, City University of New York

The Issue:

Flooding is among the costliest and most common natural disasters in the United States. Moreover, as the inland devastation that hurricane Helene painfully showed, the risk of flooding is increasing even in areas that have not been traditionally considered flood prone. Yet only a fraction of homeowners in flood-prone areas have flood insurance. The government program that is the main source of home flood insurance coverage in the United States has been the target of reforms for over a decade and recently changed the way it calculates insurance premiums. This is the biggest reform since the inception of the National Flood Insurance Program in 1968 and it is fundamentally changing the price of residential flood insurance for many households, impacting take up and coverage. Whether the reform will help shore up the program’s finances or reduce Americans’ financial exposure to flooding over the long term remains to be seen.

A reform of the US's main source of residential flood insurance is fundamentally changing the price of premiums, impacting take up and coverage.

The Facts:

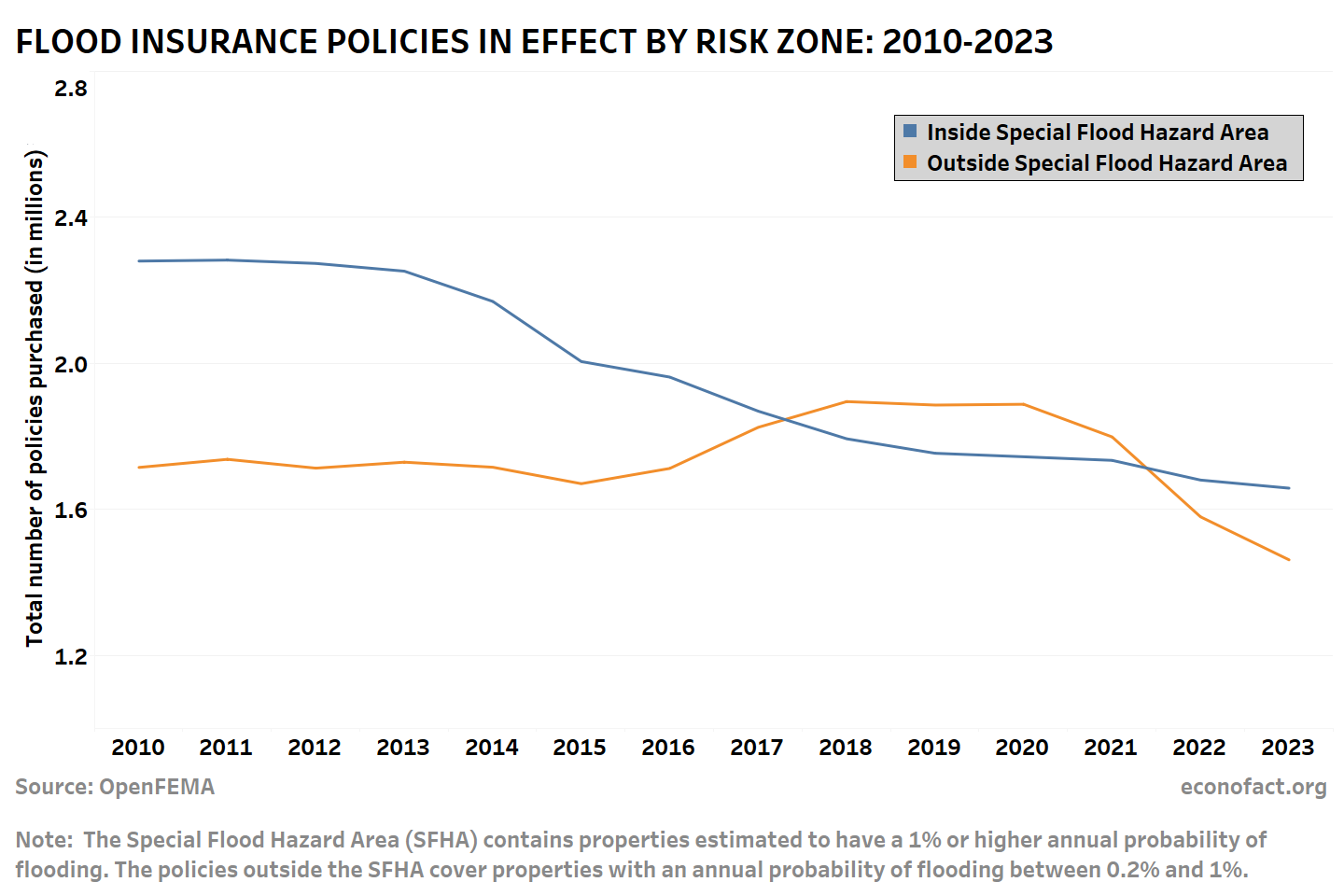

- In spite of rising flood risks, the number of flood insurance policies in the United States has been going down. Up to 90% of natural disasters in the United States involve flooding, according to estimates by the Department of Homeland Security. Moreover, exposure to this risk is increasing over time due to the combination of the increasing frequency of large-scale flooding events and increasing agglomeration of population and residential units in flood-prone areas. Yet the number of flood insurance policies has been steadily decreasing in recent years. The number of policies issued by the National Flood Insurance Program, the primary source of flood insurance for residential properties in the U.S., dropped from 5.11 million policies at the beginning of 2019 to 4.77 million policies as of December 2022 (see page 46). Since 2020, the number of policies has been decreasing both within the Special Flood Hazard Area (where the annual chance of flooding is 1% or higher) and outside of it (see chart). Insurance policies outside the flood zone saw a short-lived bump in numbers in the aftermath of Hurricane Harvey, which produced extensive flooding outside of flood zones in 2017, as properties that receive FEMA aid are required to purchase flood insurance for three years.

- Standard homeowners insurance policies do not provide flood coverage. Flood insurance coverage in the United States has been mainly provided by the National Flood Insurance Program (NFIP) which is managed by the Federal Emergency Management Administration (FEMA). Congress created the program in 1968 to reduce the costs associated with providing federal flood assistance to repair damaged properties and businesses and to fill the void created by the absence of a robust private market for flood insurance — a gap that largely remains to this day. In addition to providing homeowners access to primary flood insurance, the NFIP seeks to mitigate the nation’s overall flood risk by encouraging sound floodplain management. These goals are accomplished by making NFIP flood insurance policies available only in areas and communities that voluntarily adopt and enforce the agency’s floodplain management standards. The National Flood Insurance Program engages in “noninsurance” activities such as producing flood maps that inform local flood risks and offering incentive programs for household and community investments in flood-risk reduction (see here).

- Over the last two decades, the NFIP has been operating heavily in the red, having to borrow from the federal government to cover catastrophic losses. As of September 2022, the NFIP’s debt was $20.5 billion despite Congress having canceled $16 billion in debt in October 2017. Particularly catastrophic flooding seasons in 2005 (hurricanes Katrina, Rita and Wilma), 2012 (hurricane Sandy) and 2017 (hurricanes Harvey, Irma and Maria) generated losses that dwarf those of the 1980s and 1990s (see here). The Government Accountability Office has listed the NFIP in its High Risk List since 2006 as a result of the growing imbalance.

- To ensure the fiscal soundness of the National Flood Insurance Program, reforms aiming to gradually eliminate subsidized rates began in 2012. Many premiums insured by the NFIP were artificially low relative to their actual flood risk. The program’s “original sin” was partly the result of offering subsidized rates to properties that were built in flood zones before flood insurance rate maps were available from FEMA. These properties represented a large financial burden: in 2015, they made up roughly 1/3 of the policies, but 2/3 of the claims (see here). Moreover, by not reflecting the true risk of flooding, flood insurance probably contributed to building in flood-prone areas. The 2012 Biggert-Waters Act introduced many reforms to make the NFIP more financially stable and make insurance rates better reflect actual flooding risks. The reforms focused particularly on the subset of highly subsidized properties and on reducing subsidies over time (although some of these reforms were moderated by subsequent legislation fueled by concerns over rapidly rising rates).

- In late 2021 FEMA began rolling out a major reform of the NFIP, Risk Rating 2.0, which modernizes the way the NFIP estimates flood risk and adopts individualized pricing that reflects each property’s flood risk. Prior to the reform only a limited number of factors were considered to determine flood insurance premiums, such as whether or not the property was within a flood zone, occupancy type, and elevation (if available). Under the new system, premiums are calculated on a broader set of factors to more closely reflect an individual property’s flood risk. Risk Rating 2.0 takes into account specific features of a property, including distance from water, type of flooding, flood frequency, structure foundation type, elevation of the lowest floor (for all properties), prior claims, and the building’s replacement cost, among others. Risk Rating 2.0 also seeks to factor the risk of other types of flooding beyond coastal and riverine flooding such as the risk of flooding from heavy rainfall (see here and here).

- Risk Rating 2.0 did not necessarily mean higher insurance premiums for everyone. In theory, the new premiums are based on actuarially fair rates — the point at which the premiums are equal to the annual expected payout (calculated by multiplying the probability of the risk by the estimated damage). The new insurance rates were expected to entail price increases for some homeowners and reductions for others, reflecting the flood risk of each individual property. Consequently, to the extent that homeowners’ insurance decisions are price-sensitive, the reform is likely to induce both entry and exit into the flood insurance market.

- In practice, the decline in the number of households purchasing flood insurance has accelerated since the reform was rolled out. In our research, we linked individual NFIP policy purchases over the period 2019-2023 to try to understand the impact of the reform on homeowners’ insurance decisions. We find that the reform increased the number of households that chose not to renew their flood insurance policies. Overall, the reform increased annual exit from the program (due to non-renewal) from 31,000 to 84,000 policies. Theoretically, the adoption of actuarially fair pricing could trigger the entry of new customers into the system. Indeed, we find that this happened in the Special Flood Hazard Areas, where there was an increase in new policies. However, the opposite effect happened outside of these areas. In sum, we estimate that enrollment in the NFIP would have fallen by 81,000 policies in 2023 even in the absence of the reform. The implementation of Risk Rating 2.0 exacerbated this decline by an additional 83,000 policies.

What this Means:

The National Flood Insurance Program has come a long way thanks to more accurate risk estimation and changes to insurance rates that better reflect current flood risk. These improvements provide better information to homeowners and potentially incentivize individual investments in mitigation. However, the reform has exacerbated the decline in enrollment in the program: take-up in 2023 is 22% lower (approx. 800,000 policies) than a decade earlier. Further reforms will be needed in order to balance premium affordability and the solvency of the program.

Topics:

climate changeLike what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.