How Economic Crises Spread Abroad

University of California, Santa Cruz and Fletcher School, Tufts University

The Issue:

The Issue:

The COVID-19 pandemic demonstrates in a particularly stark way how the world is interconnected with respect to the transmission of disease. But it is not just an issue for public health. There can also be implications of global interconnectedness with respect to acute economic maladies. How do economic “diseases” spread from one country to another? How has the United States suffered from economic disruptions originating abroad, contributed to downturns in other countries, and helped other countries at times of economic crises?

Countries benefit from increasing international trade and financial flows. But interconnectedness can make them vulnerable to economic shocks originating abroad

The Facts:

- Economic interconnectedness, through both international trade and cross-border financial flows, has generally increased in the post-World War II period. Global trade in goods and services increased to 25% of total global output in the last few decades. The experience of the United States reflects this pattern, with an upward tendency of its sum of exports and imports relative to GDP. The rise in trade reflects both technological advances and government policies. Containerization, for instance, enabled cheaper and easier shipping by sea and land, while the internet offered manifold expansions of trade in services as well as goods. Meanwhile, the creation of the General Agreement on Tariffs and Trade (GATT) in 1947, and successive rounds of trade negotiations by its successor, the World Trade Organization (WTO), have led to lower trade restrictions. Although measuring the extent of financial flows is more challenging than that of trade flows, evidence suggests greater international borrowing and lending as well over this period. Cross-border bank lending is estimated by the Bank of International Settlements to be about 40% of global GDP.

- There are benefits to greater trade and financial interconnectedness. Increased international trade of goods and services increases the efficiency of production by allowing for specialization in production and access to larger markets. It also increases the variety and choice of products available to consumers. The location and size of the United States makes it relatively “closed” with respect to the rest of the world as compared to other advanced economies. Still, about 20% of all consumer spending on goods in the U.S. goes to foreign producers and American manufacturing companies export about half of their output. American banks and financial institutions have a global presence, and borrowers in the United States, especially the government (through the sale of Treasury bills and bonds), benefit from a world capital market that lends to this country at rates that are more favorable than what would prevail if borrowers had to rely exclusively on domestic American savings. Similar benefits are even more pronounced for other countries that see a bigger foreign presence in trade and finance.

- However, increasing international trade and financial flows make countries vulnerable to economic shocks originating abroad. For example, the spike in the price of oil in 1973 meant that the United States and other oil-importing countries effectively paid a “tax” to the OPEC countries that led to a recession and contributed to the high inflation of the 1970s. A second example is the financial crisis that started in Thailand in July 1997 that spilled over to other countries. Problems in the country's domestic banking sector led to a pullback by foreign investors, setting off a spiral of depreciation, recession, and amplified banking sector weakness. Contagion happened when foreign creditors started pulling back from other countries in the region seen as having similar vulnerabilities. The crisis spread first to economies in East Asia and then to Russia, Brazil, and elsewhere. In the United States, the initial impact had both negative and positive ramifications. There were direct trade-related disruptions through lower exports — as impacted countries lowered their purchases of U.S. products. But the U.S. also benefited from reduced inflation pressures from cheaper imports and lower commodity prices as well as lower costs of borrowing because of an increased demand for safe U.S. government bonds. However, the adverse effects of the Asian financial crisis on Russia and Brazil eventually led to the 1998 collapse of Long Term Capital Management (LTCM), which was a large enough event to draw the attention of the U.S. Treasury and efforts by the New York Federal Reserve Bank to contain the potential financial contagion. A third example, the 2008 Great Recession, differs from these other two cases in that it originated in the United States with a meltdown in its financial markets. The crisis spread to other countries through both financial and trade channels. European and Asian banks found themselves with assets on their books that lost value overnight, imperiling their solvency and limiting their lending. The decreased demand for imports by American consumers and companies due to the collapse of U.S. income, as well as restricted access to trade finance, sparked a worldwide “Great Trade Collapse”. More recently, the recession associated with the COVID-19 pandemic, a global crisis, has hit developing countries particularly hard through reduced financial flows and a temporary reduction in the values of commodity exports, remittances, and tourism, in addition to the direct effects of the health crisis and associated lockdowns.

- Economic events in the United States have a disproportionate effect on the rest of the world due to the dominant position of the U.S. in global trade and financial markets, and because of the use of the U.S. dollar as a global currency. The disinflation policy of the United States at the end of the 1970s offers an example. The Federal Reserve raised interest rates in the United States to nearly 20% at the end of the decade, when the unemployment rate in the U.S. was over 7.5% and inflation was at nearly 15%. The policy was eventually effective in that it ushered in a new era of low inflation. But it also contributed to a recession in the United States and a global recession as the effects of contractionary monetary policy in the U.S. spilled over through trade and financial markets to other countries. On the trade side, companies that exported to the U.S. actually gained from the dollar appreciation, because their goods became relatively cheaper for the U.S. consumers to buy, but there was a countervailing reduction in demand for imports with the U.S. recession; the real value of U.S. imports were lower in 1980, 1981 and 1982 than they were in 1979. On the finance side, dollar appreciation created problems for anyone with debt denominated in U.S. dollars, including many emerging market governments. High interest rates in the U.S. also triggered capital outflows from highly indebted developing countries. These last two factors contributed to the debt crisis in Latin America in 1982.

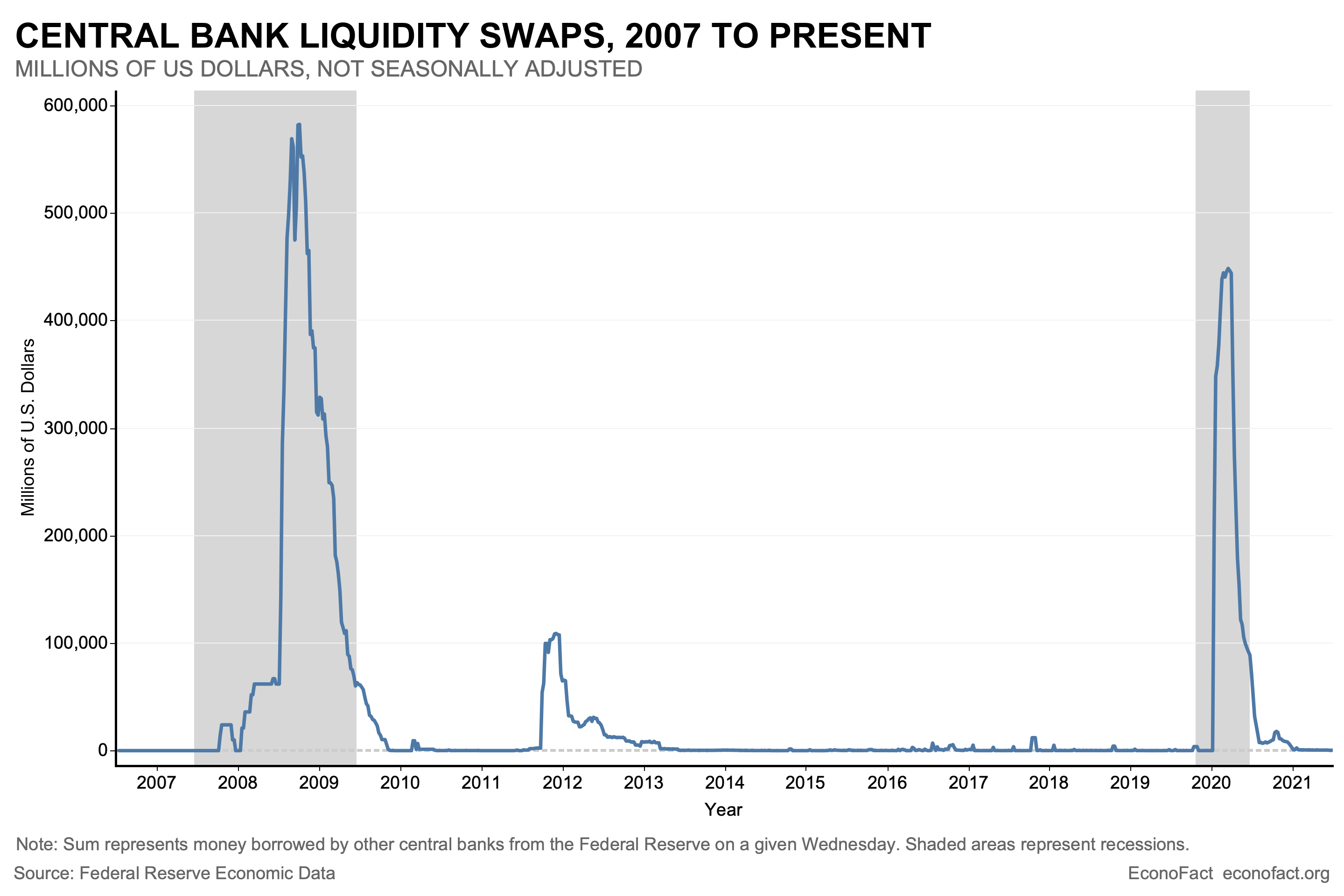

- But the U.S. is also in a unique position to help during crises. The 80s debt crisis in Latin America was eventually resolved through the implementation of the Brady Plan in which defaulted debt was converted to U.S.-guaranteed bonds. This restored countries’ ability to borrow abroad and created an active global trade in sovereign bonds. Similarly, efforts by Federal Reserve Chairman Alan Greenspan, Treasury Secretary Robert Rubin and Treasury Undersecretary for International Affairs Lawrence Summers to prevent a global economic collapse in the wake of the 1994 Mexican Crisis and the 1997 Asian Crisis prompted a 1999 Time Magazine cover that declared the three as "The Committee to Save the World." During the Global Financial Crisis of 2008-09, the Federal Reserve provided many foreign central banks with “swap lines,” which were U.S. dollar loans that those central banks could use to lend dollars to their country’s commercial banks in order to alleviate dollar shortages. This was important because widespread losses on dollar-denominated assets meant that foreign financial institutions needed to buy U.S. dollars at a time when the market experienced a shortage of U.S. currency and foreign central banks did not have sufficient dollar reserves to help their banks. As the chart shows, in early 2009, nearly 600 billion U.S. dollars were provided to foreign central banks. Similarly, in March 2020, when it became clear that COVID-19 was a pandemic that would require a global lock-down and financial markets panicked, the Federal Reserve provided over 400 billion U.S. dollars weekly through March, April, and May of 2020 to foreign central banks.

What this Means:

The term “contagion” is used by economists to describe how, in an economically interconnected world, countries’ economic fortunes are affected by adverse events originating in a single, large country or region. Economic events outside the United States affect conditions in this country while the size of the United States economy, as well as the central role of the dollar in international transactions, means that economic crises in this country have outsized effects globally. The United States can also help other countries at times of crisis, through both direct actions and by participating in coordinated responses. Ultimately the best way for an individual country, including the United States, to deal with economic disruptions originating beyond its border is from a position of strength – to have stable inflation, manageable government debt, robust economic growth, and reliable banks and financial institutions. Countries that start out in a better economic position tend to do a better job of weathering crises brought on from foreign sources, just as an initially healthy individual is better positioned to survive a disease than someone with underlying health conditions.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.