Economic Fallout from the COVID-19 Crisis on Developing Economies

Harvard Kennedy School, and The Fletcher School, Tufts University

The Issue:

Thus far the coronavirus pandemic has hit some of the world's richest economies particularly hard. The United States, Italy, Spain, France and the United Kingdom were the five countries experiencing the highest known death tolls from COVID-19 as of mid-April 2020. But this does not mean that emerging markets and developing economies have been spared. The worldwide coronavirus pandemic is likely to hit these economies harder than economies in richer countries. Not only are their public health systems under-resourced to deal with the outbreak, making the containment and treatment of the disease more difficult, but their economies are already being battered by the way in which the pandemic is impacting global demand and financial markets. The economic and financial vulnerabilities of these countries at the beginning of this year, as well as the way the economic effects of this pandemic are unfolding, suggest that many less-developed countries are facing a very rough road ahead.

Developing economies are already being battered by the way in which the pandemic is impacting global demand and financial markets.

The Facts:

- Although there is a high degree of uncertainty regarding specific forecasts, as the full duration and pathway of the novel coronavirus outbreak remains unknown, there is widespread agreement that there will be a worldwide economic slump in 2020. The International Monetary Fund predicts the global economy will contract by 3 percent in 2020 in its April 2020 World Economic Outlook. This outlook is in agreement with forecasts by, among others, S&P Global and Moody’s Analytics. While there is still great uncertainty about the depth and duration of this crisis, “it is already clear, however, that global growth will turn sharply negative in 2020. In fact, we anticipate the worst economic fallout since the Great Depression,” said Kristalina Georgieva, the Managing Director of the International Monetary Fund (IMF). “This is already shaping up as the deepest dive on record for the global economy for over 100 years,” according to Harvard economist and co-author of a bestselling history of financial crises, Kenneth Rogoff.

- Emerging market and developing economies entered 2020 with vulnerabilities. The group of countries that the IMF classifies as emerging market and developing economies is diverse, including low-income nations in Africa, Asia and Latin America, but also countries that are highly dependent on one export product such as oil-producing Saudi Arabia, and countries such as India, China and Russia. Though not all characteristics apply to all of the countries in this category, many share features that place them in a vulnerable situation to face the pandemic. Advanced economies in Europe and the United States have struggled to find sufficient ventilators and medical equipment in regions where their medical systems have become overwhelmed by the pandemic. Developing nations are confronting the outbreak with health systems that have fewer resources: Sierra Leone, for instance, has 13 ventilators for the whole country. Developing and emerging market countries similarly have far fewer macroeconomic tools than advanced economies to cushion the blows from the outbreak and the social isolation measures taken to counter it. They have less money to spend on fiscal packages to support workers and companies through the pandemic, they have weaker social safety nets, much larger informal sectors — with workers lacking access to any government support and depending on tasks that often require personal interaction to make a living — and it is more difficult for their governments to borrow money as their borrowing costs soar. Central banks are unable to finance government spending by printing money, or engage in expansionary monetary policy, without stoking fears of a return to previous episodes of inflation and further weakening their currencies relative to the U.S. dollar.

- Income from international trade and remittances will be adversely affected by the coronavirus crisis. Developing countries are typically more dependent upon fewer sectors than advanced economies, and often these include reliance on commodities, tourism, agriculture and some manufacturing. These economies also tend to have a higher proportion of imports and exports than most advanced economies. The steep decline in economic activity in advanced economies will cut into the demand for exports from developing countries, depressing incomes in these countries. Countries that export commodities will also be hurt by falling prices due to the worldwide recession. The global prices of some agricultural commodities have fallen by more than 15 percent between the beginning of 2020 and early April: these include cotton (an important export of China, India, Pakistan and Vietnam), cocoa (Ghana and Ecuador), and palm oil (Indonesia and Malaysia), according to the IMF report (see page 17). Copper (an important export of Chile, Peru, Indonesia and Brazil) and oil (an important export of Mexico, Colombia, Nigeria, Russia and Saudi Arabia) have fallen by 15 percent and 66 percent, respectively during the same period (the oil price decline has also been driven by rising supply from Saudi Arabia and Russia). The shutdown of the global economy also truncates revenues from tourism and remittances. Tourism accounts for about one-seventh of GDP for Cambodia, one-tenth of GDP in both Thailand and Jamaica, about 3 percent for South Africa and about 2 percent for Mexico. A diaspora of workers in developed countries sending home part of their paychecks have now lost their jobs. Remittances account for about one-third of GDP for Haiti, one-fifth of GDP for El Salvador, and one-tenth of GDP in Egypt, Ukraine, and the Philippines.

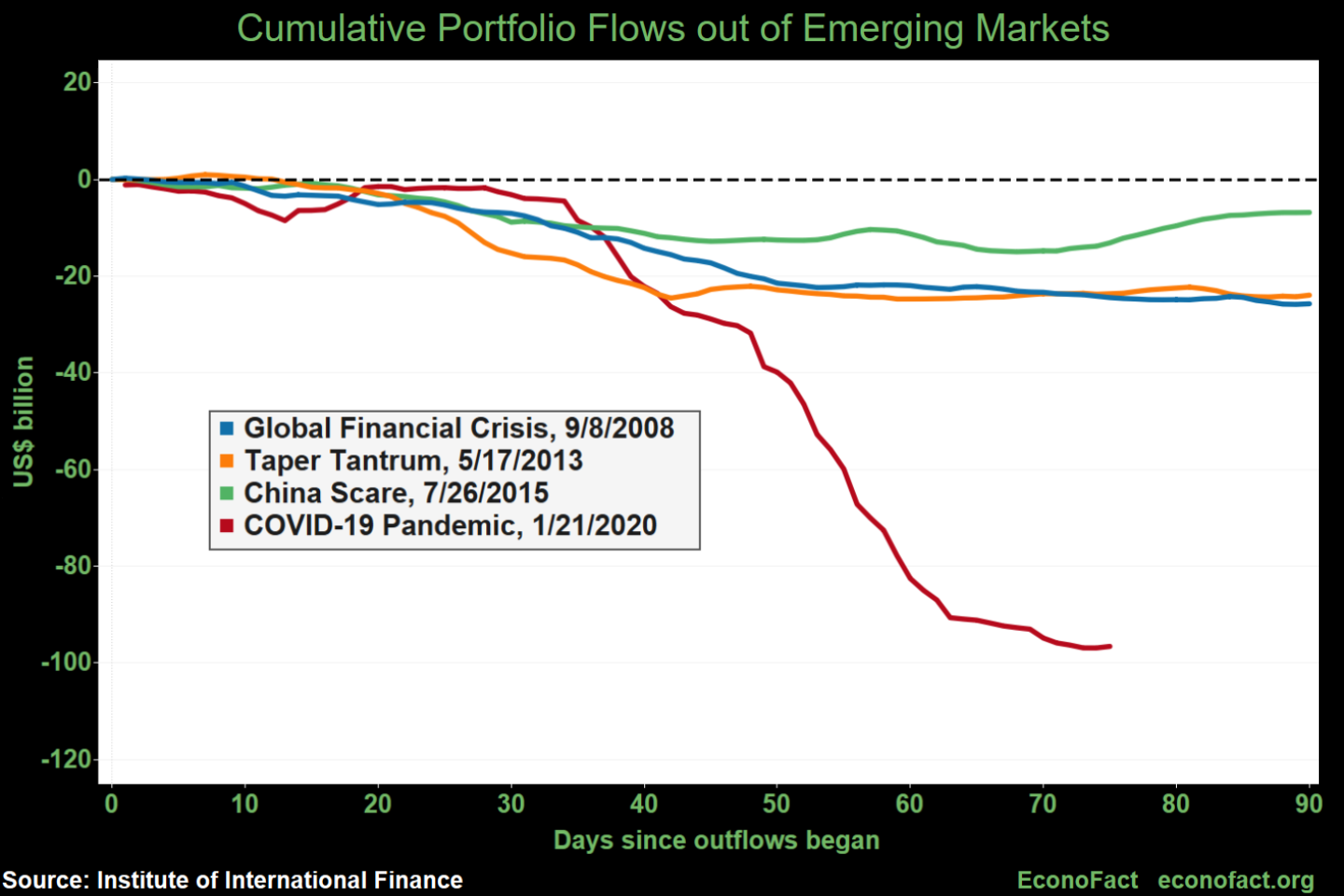

- The ability to borrow from advanced economies has been adversely affected as a result of the crisis. Emerging markets and developing economies borrow from other countries through capital inflows. This borrowing provides resources for governments and companies to enable them to build capacity and meet current needs. Emerging markets and developing economies are not entering this crisis from a position of strength: they already had an excessive build-up of public and private debt. Emerging Market debt reached 220 percent of those countries’ GDP in 2019; by comparison, this figure was 147 percent in 2007 before the Great Recession. International investors have responded to the coronavirus crisis by pulling capital out of these countries in order to buy safe-haven assets. March 2020 has seen the largest non-resident capital outflows on record for emerging market and developing economies, which have pushed up borrowing costs and made debt servicing even more difficult, according to the Institute of International Finance. The three months since the onset of the coronavirus crisis has seen a larger capital outflow from developing countries than what they experienced during the same length of time in the wake of the 2008 financial crisis, the 2013 taper tantrum and the 2015 China slowdown combined (see chart).

- Strengthening of the dollar makes it more difficult for governments and companies in developing countries to repay debts. As of April 3, the U.S. dollar has strengthened by 8.5 percent in real effective terms since the beginning of the year as investors liquidated assets and bought U.S. dollars, according to the IMF. Developing and emerging country debt is particularly exposed to a strengthening dollar because their governments and, increasingly, corporations have been issuing significant amounts of debt denominated in U.S. dollars; Emerging Market countries’ debt denominated in foreign exchange accounts for over 8% of their nonfinancial sector debt, with the biggest increases over the past decade in Argentina, Chile, Colombia and Turkey. As the dollar appreciates, these governments and firms have to spend more in their local currency to service ever dearer debt. The Federal Reserve has responded to the need for dollars by establishing new swap lines or easing the terms for using existing swap lines with fourteen foreign central banks. Most of these swap lines are with central banks of advanced economies, although Brazil and Mexico are also included. These swap lines have eased dollar funding pressures, but challenges remain for emerging market and developing economy countries not included in this initiative.

What this Means:

More than 90 countries have petitioned the IMF for assistance in the past few weeks, and the IMF estimates that emerging markets and developing economies will face a shortfall of at least $2.5 trillion this year - the IMF can lend up to $1 trillion. Even if advanced economies successfully transition back towards a more normal situation by the end of the summer, it is most likely that developing countries will still be facing the challenges outlined here. And beyond the economic and humanitarian crisis for people in those countries, the fact that emerging markets and developing economies account for around 60 percent of the global economy means that weakness there will contribute to weakness among advanced economies as well. This dire prediction calls for responses. A recent set of proposals from the Peterson Institute for International Economics sets out a range of ways the international community could help developing countries including direct support for COVID-19 responses, bans on medical equipment and food export restrictions, a stronger international financial safety net, and a voluntary standstill on foreign debt repayments.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.