How is the Coronavirus Crisis Affecting the Municipal Bond Market?

Brandeis University

The Issue:

Over the past month, the municipal bond market has shown signs of unprecedented stress and volatility. State and local governments depend upon this market to fund infrastructure like school buildings, roads and airports, as well as to bridge short-run mismatches between receipts and outlays. These bonds also offer a relatively safe investment class because rates of default by municipal issuers are generally quite low. But the coronavirus crisis has put stress on the municipal bond market, causing some concerns about the safety of those investments. Recent intervention by the Federal Reserve included some targeted measures designed to help stabilize these markets, but the ongoing crisis is likely to have some important implications for cities and states, for investors in the municipal bond market, and for others, including people who may expect to receive state and local pension benefits.

The crisis is likely to have important implications for cities and states, for investors in the municipal bond market, and for others, including people who may expect to receive state and local pension benefits.

The Facts:

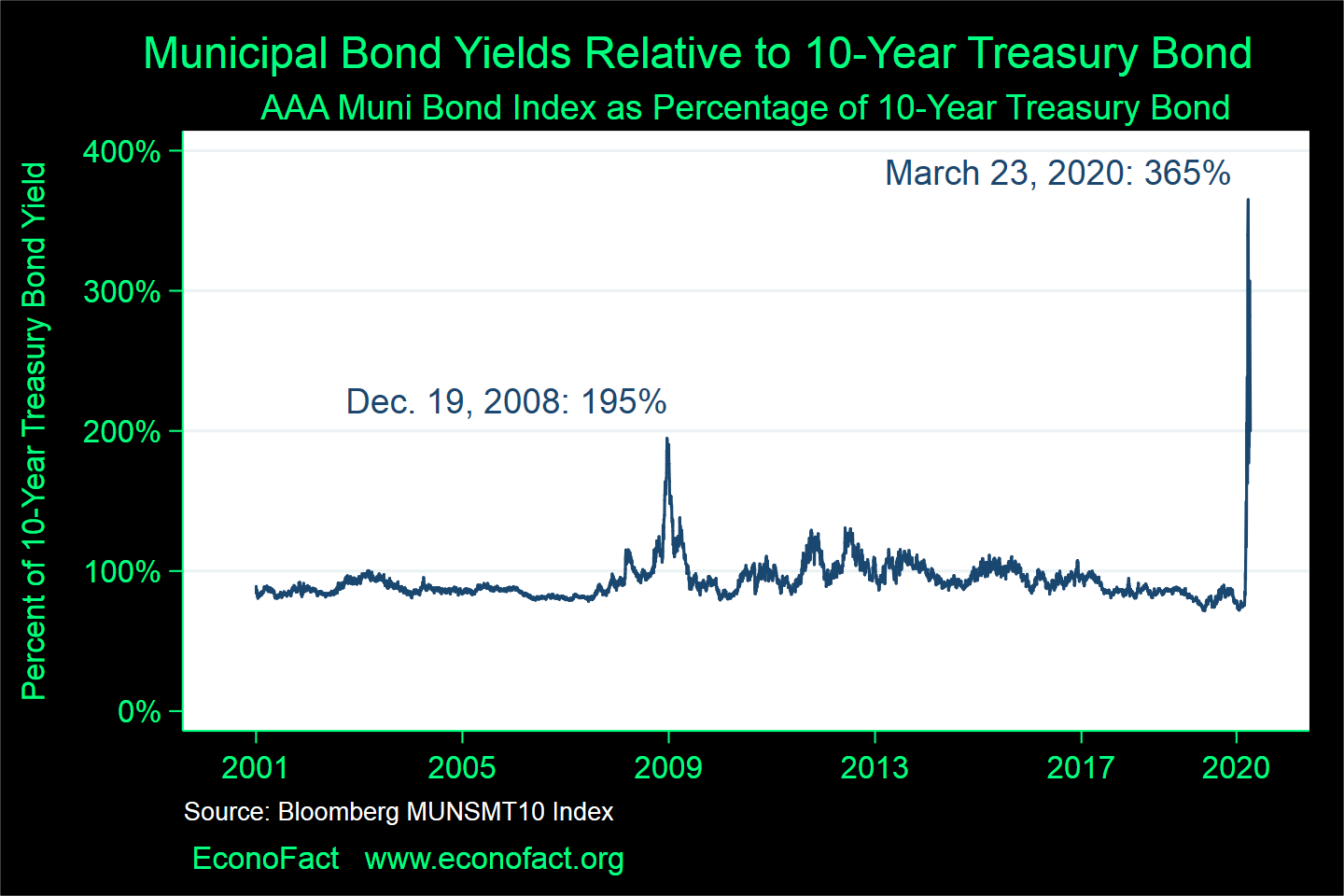

- Interest rates on municipal bonds have risen dramatically in the wake of the emerging coronavirus pandemic. The recent spike in interest rates in the municipal bond market and the volatility in that market are without precedent, and even dwarf what was seen in the 2007-2009 crisis. The graph shows the average interest rate on the lowest risk, AAA-rated municipal bonds that are 10 years from their maturity date, scaled as a percent of the 10-year Treasury bond yield. This ratio has typically been less than 100 percent because the interest on municipal bonds is tax-exempt so these bonds can offer a lower pre-tax interest rate than Treasury bonds. However, during the financial crisis at the end of 2008, this ratio rose to almost 200 percent. In recent weeks it has risen to more than 350 percent, a figure that well exceeds the ratios observed during the worst depths of the 2008 crisis. The standard deviation of this ratio between the beginning of February 2020 and April 7, an indicator of the volatility of the market, was more than 7 times bigger than the standard deviation in the period from the beginning of 2001 through January 2020, and more than triple the standard deviation in September through December 2008, the worst months of the 2008 financial crisis.

- Municipal bonds are an important source of financing for state and local governments’ investments in infrastructure. Higher interest rates make it difficult for these governments to borrow to meet future needs (and, in some cases, will raise the cost of their existing debt). State and local governments need to balance their budgets for current spending on items like education, fire and police services, and the elements of the social safety net they provide. Municipal bond markets enable states and local governments to borrow capital for infrastructure projects — when state and local governments sell bonds they are essentially selling promises to pay investors back a fixed amount of capital by a given date. The overall size of the municipal bond market at the end of 2019 was about $4 trillion, making it a large market but smaller in size than the market for U.S. Treasury bonds, which is about $17 trillion, and the $10 trillion market for U.S. corporate debt (see here). Most municipal debt is fixed-coupon, so a rise in interest rates does not affect the payments state and local authorities need to make on outstanding debt, although it does raise the interest expense of their future issuance. But a significant share of municipal debt has variable interest rates, so spikes in interest rates raise the immediate cost of this debt to the state and local authorities that have relied on variable-rate debt. (The total size of the municipal floating-rate note markets was approximately $230 billion at the end of 2018.)

- The spike in the interest rate of municipal bonds is equivalent to a fall in their price, which lowers the wealth of households that hold these bonds. An increase in the interest rate of a bond is equivalent to a decrease in the price of that bond since a higher return from a fixed coupon payment is obtained with a lower price for the bond. The municipal bond market is distinguished from other bond markets because almost half of the debt is held directly by households. By way of comparison, only 10 percent of the value of Treasury securities is held directly by households. This means that the pain of municipal bond price declines may be felt directly by households who hold the bonds, without the layers of intermediation that are more frequently seen in the holdings of other categories of bonds. In short, the stress that the coronavirus crisis is putting on the municipal bonds market is showing up rapidly in the wealth of households who own them.

- What explains the spike in municipal bond yields? Municipal bonds are priced (and the interest rate is set) based on the characteristics of the payment streams that back up these bonds. To understand the recent spike in municipal bond yields, it is important to appreciate first that in a well-functioning market these bonds will be valued in ways that reflect the underlying flows of revenues and taxes that are behind the promised payments they offer. The municipal bond market includes different types of bonds. For example, some bonds are backed by the issuers' ability to raise funds through taxes; others are backed by the revenues from specific infrastructure projects, including stadiums, university facilities, roads, airports, and sewer systems. A spike in bond yields can indicate changes in investors' expectations about the soundness of these payment streams.

- The ongoing Coronavirus crisis may have very different effects on different types of municipal bonds. Social distancing in the short run and consumer concerns about large gatherings and travel over a longer horizon may significantly disrupt revenues from stadiums and airports, respectively, while revenues for a sewer system in a high-income area are likely to be more robust to the economic, financial, and social disruptions that are ahead. If the credit quality of bonds backed by infrastructure reflects, in the end, the willingness of users to pay for the services provided by the infrastructure, then it is conceivable that America’s households will cut back on trips to Florida before they cut back on paying the sewer operator to take their household waste away.

- The stress on the municipal bond market from the coronavirus crisis, as shown by the spike in interest rates, may also reflect factors beyond purely the perceived stream of payments backing up these bonds. The recent fall in bond prices was widespread and occurred regardless of the credit quality of issuers. This suggests that the interest rate spike described above did not solely reflect long-term solvency concerns. Rather, the interest rate spike also appears to have reflected some short-run liquidity issues – that is, investor preference for cash even when the expected return on bonds and other non-cash financial assets appears high by normal standards. Municipal bonds can be subject to this type of liquidity problem because during more normal times they are generally perceived to be safe and relatively stable assets. Being held by investors who value this safety can result, perhaps perversely, in a “fire sale” for these assets in the event of a systemic liquidity shortage. The economic distress that became acute in the last month may have led to a temporary fire sale as holders of those bonds became anxious to exchange their bonds for cash. This rapid sale caused more market stress and disruption, which led to the spike in interest rates, reaching a peak on March 23 as shown in the figure (see here).

- The Federal Reserve intervened in late March to stabilize the municipal bond market, but interest rates remain elevated above normal levels. The Federal Reserve’s moves to ease some of the liquidity stress in the markets in March included the creation a new facility where holders of municipal bonds can use these bonds as collateral for borrowing cash from the Federal Reserve System. Being able to borrow using municipal bonds as collateral has appeared to ease some of the liquidity crisis for holders of this debt, since holders of municipal bonds that are eligible under this new program are freed from the need to sell the bonds to generate cash. This intervention has eased some of the short-term selling pressure in the market and brought down the interest rate, although it remained quite high at the end of the month.

- The disruption in the municipal bond market is part of the coronavirus pandemic’s larger disruption to state and local finances and operations. Depending on their mix of revenue sources and on the availability of rainy day funds and other stand-by resources, issuers in the municipal market may soon face the need to quickly reduce their expenditures. The city of Cincinnati has furloughed 20 percent of its workforce in anticipation of tax revenue declines, and the state treasurer of Rhode Island recently said that that state is within weeks running out of cash because of the pandemic and its effects. Cuts to state and local services stemming from the pandemic will reduce their ability to spend on the services they provide – health, education, public safety – at a time when the underlying needs for these services is likely to become even more acute.

What this Means:

The stress in the municipal bond market affects those who own these bonds and also everyone who depends on roads, public safety, education, and public health – the goods and services provided by states and localities. Furthermore, even though state pensions enjoy powerful legal protection, households that are counting on these benefits, as well as those who depend upon state and local retiree health benefits, may also suffer if state and local finances become sufficiently stressed. Federal Reserve intervention has eased liquidity concerns and brought down rates from their peaks, but concerns about longer-term solvency remain, especially for issuers whose finances were precarious even before the coronavirus crisis. As of early April, interest rates in the municipal bond market appear to be rising again. Senate Democrat Robert Menendez of New Jersey has introduced the Municipal Bonds Emergency Relief Act (MBERA) that would amend the Federal Reserve Act in order to enable the Federal Reserve to purchase municipal bonds directly. Unlike the liquidity-focused March interventions by the Federal Reserve System, direct purchases of municipal bonds would be a direct nationalization of the credit risk of those securities and issuers, and depending on which securities the Fed purchases, could be a dramatic rearrangement of how that risk is borne. The legislation has been introduced and referred to the Committee on Banking, Housing, and Urban Affairs, but has not been passed into law yet.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.