The Burden of Public Pension Promises on State and Local Budgets

Brandeis University and Stanford University

The Issue:

Unfunded pension liabilities represent a significant challenge to the finances of many state and local governments. While no analysts dispute the general statement that pensions are underfunded in aggregate, there has been some discussion about how to estimate the magnitude of the gap. Moreover, however it is estimated, the extent of pension underfunding varies from place to place around the country. So too do the ways in which state and local governments are trying to deal with the issue. Unfortunately some of the proposed solutions to address these problems, such as the use of pension obligation bonds, have considerable downsides.Many cities and states - with Chicago and Kentucky being notable examples - are experiencing financial stress that stems from unfunded pension obligations.

The Facts:

- While there is debate about the best way to evaluate the cost of pension obligations, the size of pension underfunding in public pension systems is in the many trillions of dollars by almost any measure (see here). Pension obligations reflect promises to pay employees and retirees in the future. Estimating the size of pension obligations requires making assumptions about how much will be paid in future periods and the “discount rates” that should be applied to those estimated future payments in order to calculate their value in today’s dollars. The Federal Reserve and the Bureau of Economic Analysis, which produce our nation’s GDP figures, recently changed their approach to calculating the value of pension obligations. The new numbers reported with the new method were significantly larger and attracted attention to the issue: The estimated underfunding grew by $2.4 trillion in these newly reported statistics, growth that is mostly a consequence changed method of estimating the value of pension obligations. These recent estimates suggest that aggregate pension liabilities in the United States amount to $8.4 trillion in total and are underfunded by over $4 trillion, according to figures released by the Federal Reserve in September of 2018 (see here table L.120b). The main change in the valuation of these liabilities was an adjustment to the assumptions about the payments that will be made in the future. The previous projections had been based on a measure that reflected the payments that employees and retirees would receive if a pension plan were to be terminated today. The new measure assumes plan continuation and makes assumptions about the growth in pension payments based on anticipated future employment service.

- There is an ongoing debate as to how the value of pension liabilities should be estimated in today's dollars — and this debate has implications for state and local budgets. Economists who study state and local pension plans have argued that cities and states use discount rates for pension liabilities that are inappropriately high, which means that they can underestimate the amount of money they need to set aside in the present in order to be able to pay their future obligations. Although this assumption has minimal economic justification, public pensions can use the rate of return they expect to generate on their investments in order to discount their liabilities. For example, a 7.6 percent expected return (the average chosen by public pension systems in 2015) would mean that state and city governments are expecting the value of the money they invest today to double approximately every 9.5 years. When these rates are applied to discount liabilities, these high discount rates reduce the present value of the future commitments. A typical government might consider a promise to pay a worker $100,000 in ten years fully funded even if it had only set aside $50,000 (see here). The problem with these assumptions is that pensions must be paid regardless of the performance of the assets chosen by the pension system. Investments such as stocks, private equity stakes, real estate investments, and hedge funds almost always have some risk. Using a discount rate based on an estimated rate of return on risky assets to value commitments like pension liabilities is a questionable practice.

- In some sense, in choosing whether to use a more conservative lower discount rate versus a higher one that is based on expected market returns, a state or locality is making a tradeoff between today's taxpayers and the taxpayers of the future. If state and local governments discount their pension liabilities using lower discount rates consistent with the returns on lower-risk assets (for instance what would be obtained from investing the funds in U.S. Treasury bonds), this decision necessarily means that they would need to set aside a higher share of their current budgets to service future pension obligations. This option can strain budgets in the short run and lead to higher taxes or expenditures diverted away from current services. An example of these tensions is evident in the area of public education, where accumulated debt, in the form of promised pension obligations, is squeezing education budgets and triggering benefit cutbacks for newer generations of teachers and students. To the extent that school revenues are diverted to pay down pension debts, fewer funds are available to raise the salaries of current teachers and to fund education (see here). On the other hand, using a higher discount rate based on an expected market return in the order of 7.5 percent can be the equivalent of a transfer from future taxpayers to today's taxpayers if the targeted return is not realized and the taxpayers of the future are forced to foot the bill.

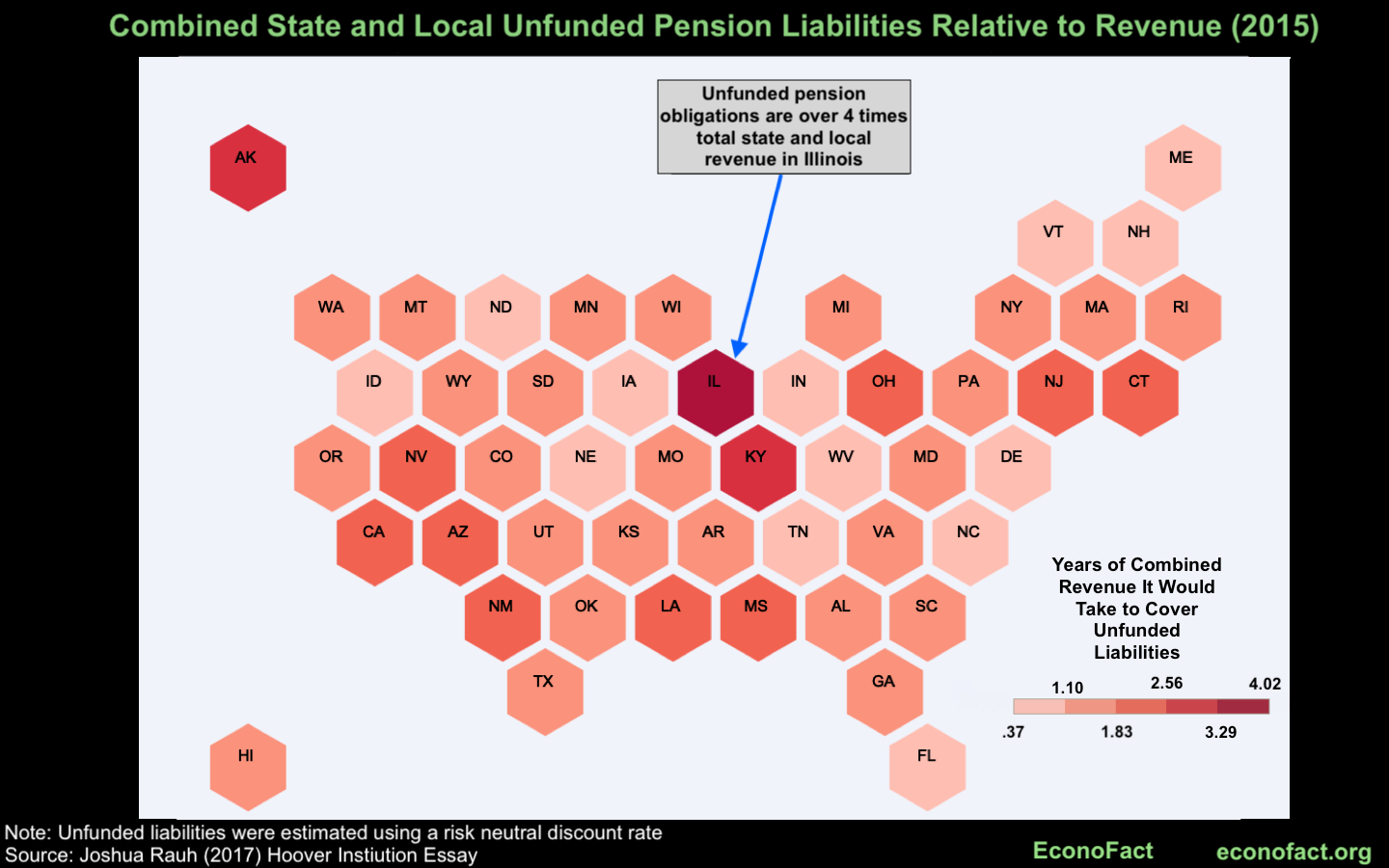

- The size of pension underfunding varies from place to place around the country. And because cities, counties, states, and other municipal entities can all sponsor pension plans, figuring out the pension liability associated with a given place can be complicated. But a number of places around the country stand out for the magnitude of the difficulties that they are facing. Combining state and local obligations, Illinois is a standout case. The value of the unfunded part of combined state and local pension obligations is $360 billion, or over four times the total state and local revenue of the entities in that state. Alaska and Kentucky also have combined unfunded liabilities amounting to more than two-and-a –half times revenue (see Figures 3 and 4 in this article). Among all of the states, Delaware is alone in having a combined state and local unfunded pension liability that amounts to less than half of a year’s value of revenue.

- How states and localities are dealing with pension obligations also varies. One approach to dealing with these unfunded pension liabilities – and an approach that has something of the nature of a shell game – is to use pension obligation bonds. This approach is being contemplated by Chicago and other cities. A pension obligation bond (POB) is a bond issued by a state or locality whose proceeds are directed to the pension funds. An issuer of a pension obligation bond transforms one type of net liability for another: the funding of the pension fund reduces the net liability of an underfunding plan, but the bond becomes an obligation of the issuer. The first POB was issued by Oakland, California in 1985, and took advantage of the tax law that prevailed at the time. The bond paid tax-exempt interest, so the required interest rate on the bond was lower than what would have been the case for an equivalent taxable instrument. At the same time, the proceeds could be issued by the (tax-exempt) pension plan in any assets, including assets that paid higher yields than the POB the city had issued. This bond was therefore very close to a pure arbitrage given the tax law of the time, with Oakland issuing a bond at a lower interest rate to finance investments at a higher yield. By making interest on POBs taxable for the purchaser, the Tax Reform Act of 1986, made this type of nearly pure arbitrage impossible. As a result, the issuance of POBs slowed after 1986. Despite the change in taxation however, there are still some features that make the bond attractive and issuers began issuing taxable POBs in the early 1990s. But in substance, the issuance of a taxable pension obligation bond amounts to a gamble that the assets in the pension fund will outperform the cost of the bond issued. Allocations to equities and “alternative investments” such as hedge funds, in aggregate, amount to more than 70 percent of the value of pension assets. So a pension obligation bond transaction amounts to borrowing even more money to invest in the stock market. So if the stock market does well, then the outcome for the issuer will be positive, in the same way that a successful trip to a casino is a windfall to the gambler. But there is no guarantee that the stock market will do well: equities have historically had higher returns on average than some other asset classes, but these higher average returns are compensation for the higher risk of this asset class. Failing to achieve the targeted rate of return would mean that the issuer would have to pay both the debt service requirements of the taxable bonds and also the unfunded pension liabilities that would remain unmet. Hence, underperformance would leave issuers of pension obligation bonds – potentially including Chicago, if they proceed with a contemplated $10 billion bond issue – in deeper holes than where they started.

What this Means:

Many cities and states - with Chicago and Kentucky being notable examples - are experiencing financial stress that stems from unfunded pension obligations. The problem is widespread, and the high-profile examples are not alone in experiencing pension-related strain. Fixes that offer seemingly painless solutions, such as pension obligation bonds, carry a high degree of risk, and often amount to passing the problem to future taxpayers. Confronting the burden of pension obligations will necessarily involve taking painful steps. The set of people who will have to take the hit is some subset of taxpayers, people who depend on public services, retirees and bondholders — but exactly the way in which the pain is allocated across those people will be the outcome of a political process that is difficult to predict. If you add up the total amount of suffering it is going to be a lot — it is just not clear how it is going to be allocated.

Like what you’re reading? Subscribe to EconoFact Premium for exclusive additional content, and invitations to Q&A’s with leading economists.